Double Base Propellant Market: Strategic Outlook 2026 — Tactical Intelligence for Decisions that Matter

Executive snapshot

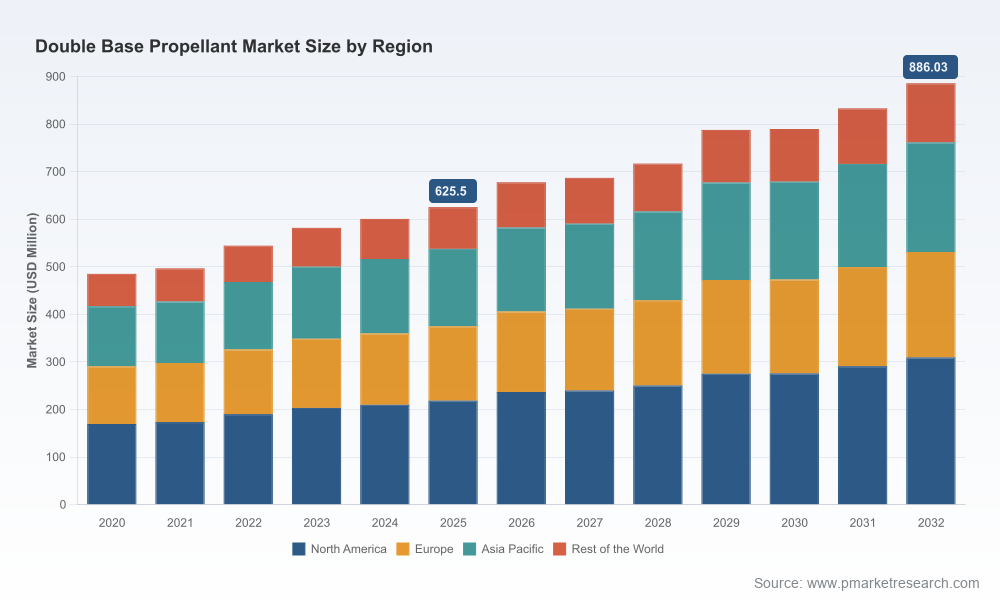

PW Consulting’s latest market study on Double Base Propellant delivers an action-oriented intelligence package for defense, industrial and investment leaders preparing decisions in 2026. Our analysis uses a 2025 base year, traces historical performance from 2020–2025, and presents a 2026–2032 forecast period built on scenario-tested demand drivers, supply-side stress tests and policy-shock simulations. The global market — measured in USD million — expanded from approximately 485.2 in 2020 to 625.5 in 2025 and is forecast to reach 677.8 in 2026, continuing to grow at a compound annual growth rate (CAGR) of 5.1% through 2032, where our baseline projects an overall market in the vicinity of 886.0 (USD million). These macro trajectories frame an industry still recovering from prior bottlenecks while entering a phase of measured expansion and strategic re-shaping.

Double Base Propellant Market

Why 2026 is a turning point

Leaders who recognize the 2026 inflection will convert near-term momentum into durable advantage. The next 12–24 months are decisive because: (1) capacity investments initiated in 2022–2025 start to come online; (2) strategic alliances and joint ventures are accelerating localization of production in priority markets; and (3) regulatory and export-control dynamics are tightening, raising the premium on compliant, on-shore or allied supply lines. Our report identifies the tactical windows where procurement commitments, technology investments and M&A activity can lock in differentiated access to propellant supply and technical know-how.

Double Base Propellant Market

Market dynamics shaping strategy

- Demand drivers — Sustained defense modernization, prepared surge production for munitions stocks and continued replacement/upgrade cycles for rockets and missiles underpin the forecasted ~5.1% CAGR for 2026–2032. While growth is steady, it is not uniform; pockets of accelerated demand coincide with national procurement programs and regional rearmament dynamics.

- Raw-material constraints — Double base propellants are chemically anchored in nitrocellulose (NC) and nitroglycerin (NG). Producers with secured NC feedstock and diversified sourcing strategies — including integrated nitration capabilities or long-term supply agreements — demonstrate measurable resilience in stress scenarios modeled in our study.

- Technology inflection — Adoption of solventless production techniques for certain high-caloric formulations is a differentiator for applications requiring ballistic stability and thermal performance. Manufacturers scaling solventless lines are likely to capture premium contracts for heavy-caliber and tank ammunition use cases.

- Regulatory overlay — Export controls and classification under strategic goods frameworks place an operational premium on compliance systems, audited quality management (ISO 9001:2015, AQAP 2110) and traceable supply chains. Non-compliant suppliers face access restrictions in major markets, altering supplier selection calculus.

- Concentration and competition — The industry exhibits moderate concentration: CR3 ~42.8% and CR5 ~58.4%. This concentration indicates both a degree of incumbency advantage and continued opportunity for targeted entrants or strategic scale-ups, particularly around capacity investments and niche formulation expertise.

Competitive landscape: capabilities that win in 2026

Our competitive assessment profiles incumbent manufacturers, turnkey plant integrators and diversified defense producers. Key patterns for decision-makers:

Double Base Propellant Market

- Integrated specialty producers (e.g., firms with vertically integrated nitration and propellant lines) retain pricing and delivery leverage when feedstock supply tightens. These players combine product range with certification credentials that most defense procurement processes require.

- Technology-led producers that have deployed solventless and high-caloric formulations are positioned to win tank and heavy-munition contracts where ballistic consistency matters. Investments in process automation and safety systems are increasingly table stakes.

- Turnkey and plant vendors that can deliver packaged production lines accelerate capability buildouts in regions pursuing on-shore capacity. Their role in enabling rapid scale-up is central to several recent national programs.

Representative companies covered in the study include established ordnance manufacturers, specialized propellant producers and turnkey plant suppliers. Each is assessed on a consistent set of criteria: technological breadth, feedstock security, certification & compliance, capacity trajectory, and partnership potential. Notable recent moves informing our 2026 view include major capacity expansions, transatlantic collaborations to bolster on-shore energetics, and new joint ventures targeting regional production hubs. These initiatives underline two themes: supply-chain localization and technology transfer partnerships are accelerating.

What the full report contains — practical assets for the C-suite and commercial teams

This research is designed as a decision-support toolkit rather than a descriptive study. Key deliverables include:

- Proprietary market model (2020–2032) with scenario levers for demand shocks, policy changes and raw-material disruptions.

- Supply-chain mapping and single-point-of-failure identification across upstream NC/NG supply and downstream conversion capacity.

- Technology readiness assessment and process-cost curves for solvent-based vs solventless production routes.

- Commercial playbooks: procurement contracting templates, long-term off-take structuring, and inventory surge strategies aligned to defense contracting cycles.

- M&A and JV screening matrix with prioritized targets and value-capture case studies for capacity buys, tech acquisitions and regional partnerships.

- Compliance and certification tracker — audit-ready gap analysis against ISO 9001:2015, AQAP 2110 and common export-control regimes.

- Risk register and mitigation roadmap covering raw-material price volatility, production safety incidents, and regulatory restriction scenarios.

To respect the “preview” role of this release, detailed regional, type and application splits that drive supplier- and program-level recommendations are available exclusively in the full report.

Five tactical moves for 2026

- Secure feedstock commitments — Lock multi-year NC supply and establish contingency contracts for NG. Our cost-impact scenarios show material vulnerability for producers without these safeguards.

- Pursue localized, modular capacity — Where procurement policy favors on-shore sourcing, modular plants and turnkey solutions offer the fastest path to compliance and reduced logistic risk.

- Invest selectively in solventless lines — For firms targeting high-caloric, high-stability formulations, solventless technology yields a differentiated product position and contract access for heavy-caliber applications.

- Build compliance and certification as capabilities — Treat ISO and AQAP compliance as strategic assets; they materially affect tender eligibility and time-to-contract in regulated markets.

- Use partnership-first market entry — Joint ventures, licensing or technical partnerships accelerate entry into restricted markets while spreading capital risk — a model already visible in recent cross-border alliances.

Risk picture and mitigations

- Raw-material shocks — Mitigate through diversified sourcing, inventory buffers and contractual price collars.

- Regulatory constraints — Embed export-control specialists in deal teams; assess program eligibility early in the RFP cycle.

- Operational safety — Invest in modern process controls and emergency-response systems; a single incident can halt operations and trigger multi-jurisdictional scrutiny.

- Market concentration risks — For buyers, concentration creates supplier risk; for investors, it highlights consolidation opportunities where strategic roll-ups can unlock synergies.

Implications for investors, OEMs and national planners

Investors should treat the sector as steady-growth with episodic upside tied to geopolitical-driven procurement. OEMs and defense integrators must prioritize supply-chain assurance and qualification roadmaps. National planners aiming for strategic autonomy will find the economics of modular and on-shore production increasingly compelling, especially where export-control rules create friction for cross-border supply.

How to use this preview

This release is a strategic preview: it surfaces the macro trajectory, competitive dynamics and practical levers that will define winners in 2026. It intentionally omits granular regional and application-level split data to preserve the value of the full analysis. Executives preparing procurement plans, capital budgets or M&A activity should consult the complete report for the proprietary models, supplier scorecards, and deal-ready playbooks that inform contract-level decisions.

Next steps

For immediate decision support, PW Consulting offers tailored briefings that overlay your program-level requirements on the market model and supply-risk heatmaps in this study. Contact our sector specialists to schedule a confidential strategy session and to obtain the full report containing detailed segmentation, supplier economics, and actionable procurement templates.

For detailed analysis of this topic, please visit the official page:Double Base Propellant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com