Residue Hydrodesulfurization Catalyst Market — Strategic Outlook for 2026

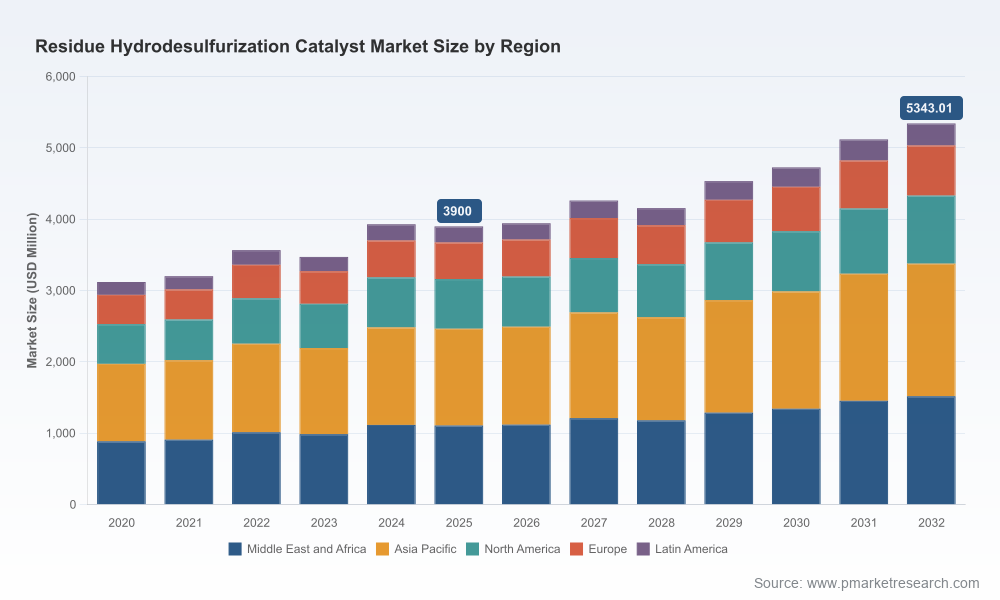

PW Consulting’s latest Residue Hydrodesulfurization (RDS) Catalyst Market report provides a focused, executable intelligence package for executives preparing capital, procurement, and technology decisions in 2026. The market for RDS catalysts has demonstrated resilience through recent cycles, standing at approximately USD 3.9 billion in 2025 and, under our central scenario, is projected to reach roughly USD 5.34 billion by 2032 — representing a 4.61% compound annual growth rate across the 2026–2032 forecast window. This release summarizes the strategic value of the full report for decision-makers and outlines the critical levers that will determine competitive advantage in the coming 12–36 months.

Residue Hydrodesulfurization Catalyst Market

Why this report matters for 2026 decisions

- Timing matters: Refinery operators, catalyst vendors, and investors face a near-term decision window where modest market growth masks structural change — regulatory tightening, feedstock shifts toward heavier residues, and supplier consolidation. Our report shows how these forces converge on 2026 investment and procurement cycles.

- Cost and margin pressure: Manufacturing margins for catalysts are exposed to metal price volatility and concentrated raw material supply chains. Tactical choices on hedging, supplier contracts, and specification trade-offs will materially affect unit economics.

- Supplier selection and partnership design: With a moderately concentrated market structure (top three suppliers capturing a clear majority share and the top five commanding an even larger portion), the report provides selection criteria and negotiation playbooks tailored to different refinery profiles and strategic goals.

- Operational risk management: Decisions about catalyst change-out frequency, pilot testing of new formulations, and retrofit schedules are capital-intensive. The report prioritizes actions that protect run-length and throughput while controlling total cost of ownership.

What the PW Consulting report delivers (practical, actionable contents)

- Proprietary demand models and scenario-based forecasts across the 2026–2032 horizon with sensitivity analysis to feedstock composition, fuel regulation scenarios, and metal-price stress tests.

- Technical profiles and decision matrices for core catalyst technologies (NiMo, CoMo, and specialty resid formulations), including recommended testing protocols and KPIs for performance validation in fixed, ebullating and slurry systems.

- A supplier evaluation and negotiation playbook that combines performance metrics, supply-risk indicators, and contract structures to minimize downtime and financial exposure.

- Cost-to-serve and TCO (total cost of ownership) templates that capture purchase price, activity life, regeneration schedules, disposal costs, and the downstream value effects on desulfurization units and product slates.

- M&A and partnership diagnostics highlighting targets, capability gaps, and integration risks — including playbooks for value capture post-acquisition.

- Operational checklists for rapid pilot design, scale-up, and decision gates aligned with regulatory timetables and refinery maintenance windows.

Competitive landscape — who matters and why

The competitive structure of the RDS catalyst market is characterized by a group of well-established global players with deep technical portfolios and regional manufacturing footprints. Leading catalyst suppliers combine proprietary formulation know-how, application engineering, and long-term refinery partnerships. The strategic implications are straightforward: access to advanced catalyst technology is increasingly a function of both technical capability and supply-chain resilience.

Residue Hydrodesulfurization Catalyst Market

- Axens SA (France) — strong in fixed-bed atmospheric and vacuum applications with a suite of transition-zone and HDM/HDS products. Axens’ integrated approach to catalyst and process licensing remains a key differentiator for complex retrofits.

- Advanced Refining Technologies (ART) (U.S.) — specialized resid hydroprocessing capability across fixed and ebullated beds. Note: ART’s ownership structure changed in late 2025 following an acquisition that reshaped capability maps for resid hydroprocessing suppliers.

- Albemarle, Haldor Topsoe, Honeywell UOP, Johnson Matthey, Shell (Criterion), BASF — incumbents offering high-activity formulations for heavy and sour feedstocks; each combines global delivery scale with targeted R&D efforts in NiMo/CoMo systems.

- Sinopec and CNPC — domestic champions with growing cross-border ambitions, supplying both standard and localized resid formulations for heavy-feed markets.

Recent industry moves, including consolidation and strategic acquisitions, underscore a trend toward vertical integration and capability aggregation. For example, the November 2025 acquisition that consolidated ART into a larger portfolio is already shifting the competitive calculus for ebullated-bed resid solutions — an important signal for buyers considering multi-unit supply agreements or long-term development partnerships.

Residue Hydrodesulfurization Catalyst Market

Key market dynamics and headwinds to watch

- Regulatory velocity: Continued global pressure for ultra-low sulfur fuels keeps demand for high-activity NiMo and CoMo residue catalysts elevated. Refiners processing heavier, sour feeds will prioritize catalysts capable of deep desulfurization while maintaining conversion and liquid yields.

- Raw material exposure: Molybdenum and other base metals remain a principal cost driver. In 2025, we observed molybdenum spot-price volatility in the order of roughly 18–22% over twelve months, directly impacting catalyst manufacturers’ margins. Standard base metal catalyst inputs were trading within a band of roughly USD 28–45 per kilogram in 2025, with specialty resid formulations commanding premiums in the 40–60% range. These dynamics necessitate active procurement strategies and cost-pass mechanisms embedded in long-term contracts.

- Concentration and supply risk: Market concentration metrics show a few suppliers commanding a majority share, which creates both negotiating power for those suppliers and supply rigidity for buyers during cyclical upticks in demand.

- Technology divergence: Incremental improvements in dispersion, resistance to poisoning, and tailored support structures are extending run-lengths, but they also raise the bar on validation and pilot testing. Refiners must balance the promise of extended life against testing timelines and up-front investment.

Strategic playbook for executives — immediate and 12–24 month actions

To convert market intelligence into advantage in 2026, PW Consulting recommends a three-tiered approach: stabilize, optimize, and transform.

- Stabilize (0–6 months)

- Hedge or layer procurement contracts for key metal inputs with strike clauses tied to molybdenum indices; establish swap-based or forward contracts where available.

- Audit current supplier contracts for force majeure and supply continuity clauses; negotiate short-term capacity guarantees for maintenance seasons.

- Run prioritized performance audits on feedstock variability and catalyst aging profiles to identify imminent change-out needs.

- Optimize (6–18 months)

- Deploy controlled pilot programs for advanced formulations with clear decision gates and economic thresholds tied to product value uplift.

- Re-evaluate total cost of ownership for alternate suppliers and formulations using PW Consulting’s TCO templates, including downstream yield impacts and regeneration schedules.

- Rebalance sourcing to include regional producers where advantageous, but only after risk-adjusted evaluation of quality, logistics, and intellectual-property constraints.

- Transform (18–36 months)

- Consider strategic partnerships, joint ventures, or tuck-in acquisitions to capture proprietary access to advanced catalyst technology or to secure dedicated capacity.

- Invest in process upgrades (reactor internals, hydrogen capacity, feed pretreatment) that unlock the value of higher-activity resid catalysts and improve overall refinery margins.

- Institutionalize an R&D-to-pilot pipeline with suppliers, including co-funded test campaigns to accelerate qualification and reduce time-to-value.

Methodology and confidence in our outputs

Our analysis uses a mixed-methods approach: bottom-up demand modeling informed by refinery-level feedstock mixes and maintenance schedules; supplier capacity and shipment data; primary interviews with technical and commercial stakeholders across the value chain; and scenario analysis calibrated to metal-price shocks and regulatory pathways. Base-year calibration is 2025, with historical review from 2020–2025 and a forecast through 2032. We supply interactive models and sensitivity dashboards in the full report so teams can run bespoke scenarios tied to their specific asset mixes.

How to use this intelligence without exposing proprietary data

PW Consulting’s report is designed around a “needs-to-decide” construct: it provides the evidence and decision frameworks necessary to commit CapEx, choose long-term suppliers, and structure hedges — while keeping proprietary operating and contractual details within client engagement channels. The summary here intentionally omits granular regional and application splits and supplier-specific commercial terms to preserve the trailer principle: we demonstrate analytical depth and strategic perspective to build confidence while guiding executives to the full dataset and executable tools behind the paywall.

Next steps — where this report creates the most value

- Procurement heads: use our TCO and hedging templates to reprice 2026 supply negotiations and to test alternative sourcing mixes under molybdenum stress scenarios.

- Refinery operations and engineering leads: leverage the pilot design checklists to shorten qualification timelines for next-generation formulations.

- Corporate development teams: apply our M&A diagnostics to screen targets for technology fit and supply-chain strategic value.

- Investors and financiers: use the scenario outputs to stress-test portfolios exposed to heavy-oil processing and to identify financing structures that reflect catalyst-related operational risk.

For a detailed breakdown of the datasets, regional and application segmentation, supplier-level benchmarking, and the full suite of decision tools referenced above, please access the full PW Consulting Residue Hydrodesulfurization Catalyst Market report — it is the definitive operational playbook for 2026.

For detailed analysis of this topic, please visit the official page:Residue Hydrodesulfurization Catalyst Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com