Technology and Digital Transformation in North America Events Industry

Other |

2026-03-20 09:43:41

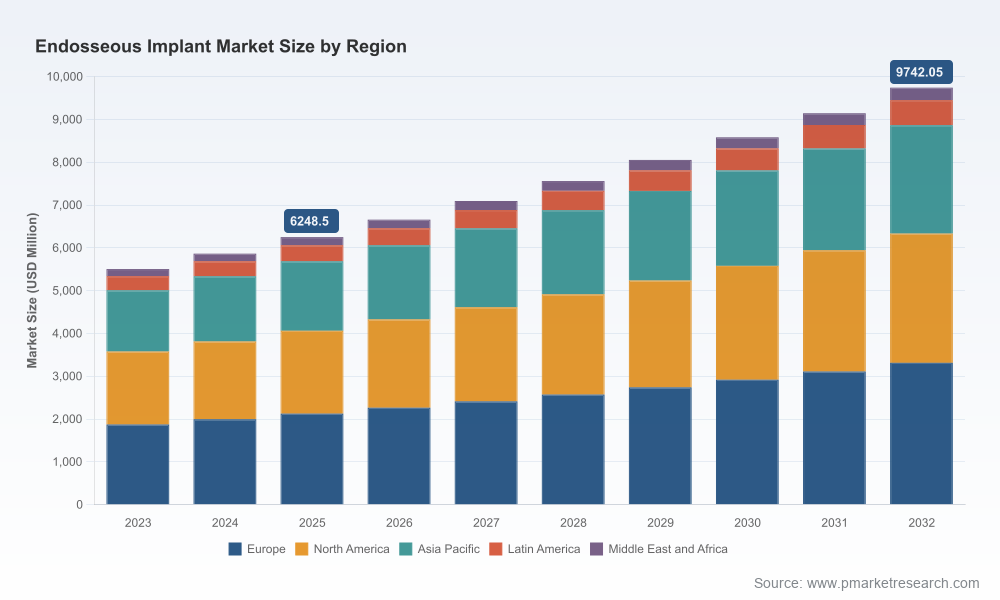

As the global dental implant sector continues its steady evolution, PW Consulting’s forthcoming Endosseous Implant Market report frames a pragmatic strategy playbook for executives preparing decisions in 2026. Built on a 2025 base year and a 2026–2032 forecast horizon, our analysis projects a compound annual growth rate (CAGR) of 6.55% across the forecast window and models the market in USD (Million). The headline: demand remains resilient, clinical evidence is widening the addressable patient pool, and innovation in materials, surfaces and system-level workflows is re-shaping competitive advantage — but execution risk is rising with regulatory and reimbursement complexity.

Endosseous Implant Market

Actionable timing: 2026 is the inflection year for several strategic vectors — product life-cycle renewals, regulatory filings aligned to Class II device controls, and distribution footprint rationalization. Our report translates market-scale trajectories into discrete decision windows so leaders can time launches, trials and M&A to maximize ROI.

Endosseous Implant Market

Operational prioritization: Manufacturers face trade-offs between investing in premium-surface R&D, scaling low-cost platforms for volume markets, or accelerating digital prosthetic workflows. We quantify the relative value of these paths (and the sensitivity to pricing and reimbursement shifts) to make capital allocation less speculative.

Endosseous Implant Market

M&A and partnership scouting: Consolidation continues. Our competitive and concentration analysis identifies where bolt-on acquisitions or exclusive distribution partnerships will deliver the fastest route to expanded addressable markets with limited integration friction.

Using 2025 as our analytical baseline, PW Consulting models steady expansion throughout the forecast period to 2032. The projected CAGR of 6.55% reflects combined tailwinds from increasing implant adoption in aging populations, broader acceptance of immediate-loading protocols, and the steady diffusion of innovations that improve osseointegration and soft-tissue outcomes. For commercial leaders, the macro trend is clear: the total market is large enough to sustain multiple growth strategies, but the winners will be those who convert product differentiation into reproducible clinical and commercial outcomes while navigating tightening regulatory regimes.

Our full report is deliberately operational. It moves beyond descriptive taxonomy to provide pragmatic tools and templates used by corporate strategy teams:

Market sizing and scenario modeling (base, upside and downside) calibrated to 2026 commercialization timelines and 2032 horizon value.

Regulatory playbook: stepwise requirements for FDA 510(k) pathways, EU MDR readiness for Class IIb implants, and checklist for country-level variations in Asia and Latin America.

Clinical evidence matrix linking surface/material technologies to likely adoption curves and reimbursement impacts.

Go-to-market blueprints for five archetypal commercialization strategies (premium innovation, value-volume, regional champion, direct-to-consumer practice enablement, and full-arch system specialist).

Supplier and sterility-risk map that integrates material standards (e.g., relevant ISO specifications for implant alloys) and sterilization requirements to protect supply continuity.

Pricing and reimbursement models calibrated to CPT coding dynamics and payer sensitivity scenarios.

M&A screening matrix highlighting targets by capability (surface tech, digital prosthetics, distribution reach) and likely integration complexity.

Primary research appendix: anonymized interview excerpts with key opinion leaders, distributors and OEMs, plus a consolidated dataset used for our revenue and CAGR calculations.

The endosseous implant market is concentrated, with top-tier firms holding meaningful shares of installed practitioner preference and channel relationships. PW Consulting’s analysis of leading players surfaces three strategic archetypes that will influence 2026 outcomes:

Technology incumbents focused on premium differentiation. Companies with proprietary materials and surface chemistries continue to command pricing power and clinical prestige. Examples include firms that have invested heavily in specialized alloy formulations and bioactive surface treatments that support faster osseointegration and immediate loading protocols.

System integrators and full-arch specialists. Players promoting system-level solutions (implant designs plus prosthetic workflows and surgical guides) are gaining share in advanced prosthetic cases, particularly where predictable full-arch protocols like four-implant concepts are preferred by clinicians.

Volume-oriented regional champions and value players. Cost-competitive manufacturers with broad distribution networks are expanding penetration in price-sensitive markets by simplifying sterile kits and partnering with localized training programs.

Key company profiles in the report provide comparative strategic intelligence (headquarters, core platform strengths, and recent go-to-market moves). We analyze recent developments that materially affect competitive dynamics, including product launches that expand immediate-loading capability, regulatory clearances enabling new lengths or indications, long-term clinical data that influence purchasing decisions, and strategic distribution partnerships that accelerate market access in target geographies.

Regulatory landscape: Endosseous implants are governed by well-defined device controls in principal markets. The FDA’s 510(k) pathway and EU MDRs are decisive factors in time-to-market and post-market obligations. Our report maps likely approval timelines and post-market surveillance burdens and quantifies their impact on development budgets and launch sequencing.

Material and manufacturing standards: ISO standards for implant materials and industry sterilization norms (including required sterility assurance levels) create minimum-capability thresholds for manufacturers. Meeting these standards is non-negotiable, and upgrades to quality systems are often a gating item for entering premium channels.

Reimbursement and coding: Dental procedure coding and payer rules materially affect adoption economics in key markets. Surgical placement codes and associated reimbursement influence clinician willingness to adopt higher-cost systems — we model elasticity of demand under alternative reimbursement scenarios.

Clinical evidence: Robust long-term survival and soft-tissue stability data remain the primary drivers of practitioner preference. Recent five-year survival publications and surface-technology studies are shifting the benchmark for “must-have” claims.

Lock in regulatory sequencing. Prioritize submissions and clinical trials so that new product families achieve major market clearances within or immediately after 2026; delayed filings materially compress your commercial runway.

Match product architecture to channel economics. Differentiate where you can win premium pricing (e.g., advanced surfaces, immediate-loading systems or prosthetic compatibilities) and bundle simplified, cost-efficient offerings for high-volume, price-sensitive channels.

Accelerate clinical evidence generation for pivotal use-cases. Invest selectively in high-quality clinical programs (randomized where feasible, multi-center where credible) that can be published within 24–36 months to support premium positioning.

Reassess distribution models. Hybrid models that combine selective direct representation in premium clinics with national distributors in volume markets deliver both margin protection and scale — but require disciplined channel conflict management.

Pursue targeted M&A to close capability gaps. Look for assets that provide either immediate clinical differentiation (surface or digital-prosthetic IP) or rapid access to underpenetrated geographies through established distribution relationships.

In keeping with PW Consulting’s “preview” approach, this release surfaces the strategic implications and high-level market sizing necessary to inform 2026 decision-making, while withholding detailed segmented dollar-value tables and granular regional or application percent shares from this public summary. These segmented datasets and interactive models are available exclusively in the full report and online data portal — designed for executive teams who need runnable numbers to stress-test strategy scenarios.

For strategy teams preparing budgets, R&D roadmaps, or M&A pipelines for 2026, PW Consulting’s Endosseous Implant Market report provides the empirical backbone and pragmatic playbooks to convert insight into executable plans. Visit our report page to access the complete dataset, downloadable scenario models, and a tailored briefing with our senior analyst team.

For detailed analysis of this topic, please visit the official page:Endosseous Implant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com