Low Fat Soya Flour Market: Strategic Outlook for 2026 — PW Consulting Report Preview

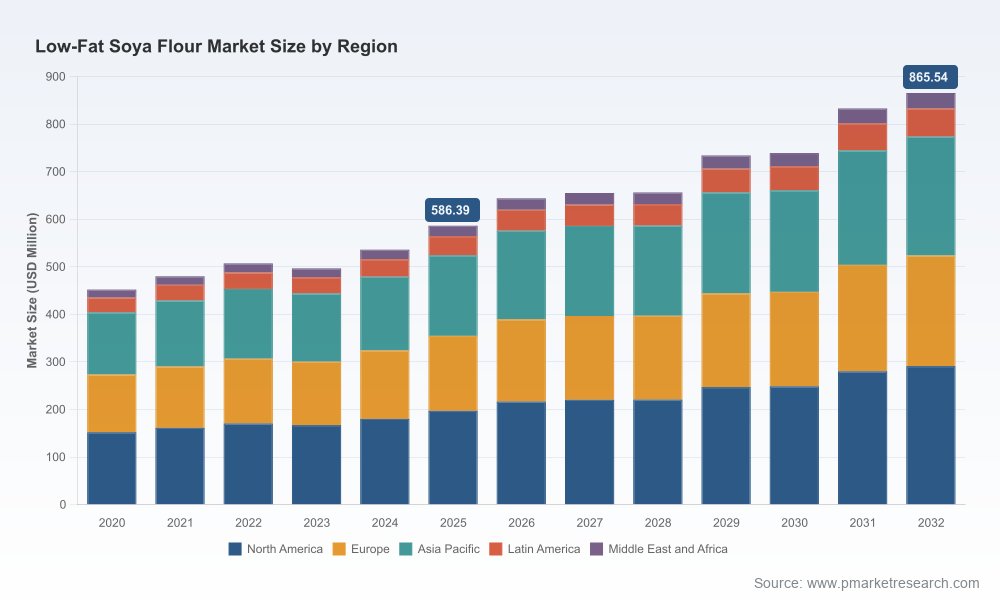

PW Consulting’s latest market intelligence on the Low Fat Soya Flour market synthesizes proprietary modeling, primary interviews and trade data to give senior leaders the actionable clarity they need for 2026 planning. Anchored on a 2025 base year and a 2026–2032 forecast horizon, the study quantifies a clear upward trajectory: after a temporary market softening in 2023, total industry revenues recovered to approximately USD 586.4 Million in 2025 and are projected to expand at a compound annual growth rate (CAGR) of 5.72% through the forecast period, approaching an estimated USD 865.5 Million by 2032. This preview explains why the report is strategically valuable for 2026 decision-making, what decision-makers will find inside, and the practical takeaways that should influence sourcing, product and M&A strategies in the coming 12 months.

Low Fat Soya Flour Market

Why this report matters for 2026 decision-makers

- Timing: 2026 is a pivotal year for translating product innovation into scalable commercial opportunities in plant-based proteins and fortified foods. Our forecast period captures both near-term volatility and medium-term structural demand shifts.

- Risk-adjusted planning: The report layers price and supply scenarios (including crush and meal dynamics) onto product demand to produce stress-tested revenue and margin outcomes — a necessary input for procurement, commercial and capital-allocation decisions.

- Go-to-market clarity: Manufacturers and ingredient buyers must choose between competing supply models (integrated processors, tolling/contract manufacture, or specialty regional suppliers). The report evaluates the tradeoffs that matter in 2026: traceability, certification, margin capture and lead-times.

- M&A and partnership prioritization: With consolidation momentum in nearby value chains, the report identifies strategic targets and partnership archetypes that accelerate access to capacity, non‑GMO sourcing and value-added formulations.

What the report delivers (practical, transaction‑ready content)

- Market sizing and model: transparent methodology with historical base (2020–2025), 2026–2032 forecasts and scenario variants tuned to raw material and demand shocks.

- End‑use demand mapping: demand drivers by formulation type and application categories, with practical implications for product specification, labeling and pricing.

- Supply chain anatomy: major crushing and flour-processing routes, cost build-up, logistics chokepoints and certification workflows (non‑GMO, organic, gluten-free).

- Price-sensitivity and margin analysis: buyer/seller bargaining dynamics, pass-through assumptions, and hedging approaches for ingredient procurement.

- Competitive playbooks: rigorous company profiles and inferred strategy maps for the leading processors and specialty manufacturers, including capability gaps and M&A levers.

- Regulatory and tariff brief: trade classifications, labeling requirements and near-term regulatory risks for cross-border ingredient movement.

- Investment and commercial roadmaps: prioritised actions for product development, capacity deployment, and channel partnerships with estimated timing and risk.

Note: This press release purposely omits granular segment-level figures and regional/application splits to preserve the integrity of our premium dataset. The full report provides the detailed breakdowns and underlying assumptions that corporates and investors require for transaction diligence.

Low Fat Soya Flour Market

Market dynamics shaping 2026 strategy

- Raw material and processing dynamics: Crystallizing supply-side signals matter. USDA’s April 2026 revision raising the 2025/26 U.S. soybean crush forecast to a record level is a structural indicator: higher crush throughput tends to increase availability of defatted flour grades but can also create short-run volatility in meal and flour pricing as processors rebalance product mix. Regional meal price observations in early 2026 underscore this dynamic and are embedded in our scenario workstreams.

- Product and formulation demand: Low-fat and defatted soya flours are increasingly selected for high-protein bakery formulations, plant-based meat and dairy alternatives, and fortified nutrition products. Their technical profile — notably high protein density and low residual fat — makes them attractive as protein fortificants and functional extenders.

- Regulatory framing: International trade and classification rules (the market’s HS classifications remain an operational hinge) influence tariff exposure and logistics planning for cross-border supply chains; the report maps these implications for common sourcing strategies.

- Innovation and premiumization: Product innovation is bifurcating the market: on one side, commodity-oriented processors compete on price and scale; on the other, specialty manufacturers and ingredient innovators are delivering ultra-high protein fractions and certified non‑GMO variants targeted at premium food brands.

Competitive landscape — who’s shaping the market and how

Our competitive analysis evaluates capability, route-to-market and strategic intent across the core incumbents and specialist suppliers that matter to corporate buyers and investors.

Low Fat Soya Flour Market

- Cargill, Incorporated — A global integrator with branded low-fat offerings designed for bakery and meat applications. Strengths: scale, application development capabilities and multi-channel customer access. Strategic consideration: Cargill’s productization of functional flour variants makes it a natural choice for manufacturers seeking technical partnership rather than a pure commodity supplier.

- Archer Daniels Midland (ADM) — A major processor with capacity breadth and product-grade diversity. Strengths: integrated crushing footprint and non‑GMO options. Strategic consideration: ADM’s scale supports long-term supply contracts and vertical collaboration on branded ingredient programs.

- Tiger Soy, LLC — A regional specialist emphasizing reduced-fat and non‑GMO credentials. Strengths: farmer-linked sourcing and flexibility for bespoke batches. Strategic consideration: attractive to buyers prioritizing traceability and niche certifications.

- Soy Austria Produktions GmbH — A European specialty producer focused on non‑GMO and semi-defatted variants. Strengths: product differentiation for premium European customers and export capability.

- Agricultural Cooperative BACEX, Bic Services, Seasons International, CHS Inc., Bunge Limited — These players span cooperatives, ingredient specialists and global agribusinesses. Collectively they demonstrate the dual structure of the market: local, high-trust suppliers that enable specialty playbooks versus large-scale processors that dominate bulk supply chains.

Recent industry moves—such as new processing capacity coming online and ultra‑high protein product launches—are accelerating the race to higher-value formulations. The full report catalogues recent facility additions and product innovations, quantifies their near-term impact on capacity and identifies where a first-mover premium is attainable.

How executives should use this intelligence in 2026

- Sourcing strategy: Reassess long-term offtake and tolling arrangements in light of capacity movements and crush forecasts; evaluate staggered contracting to balance price volatility and certification needs.

- Portfolio prioritization: Use the report’s application-level insights to prioritize SKUs that yield the highest unit economics in plant-based and fortified portfolios.

- M&A and JV screening: Apply our target archetypes to accelerate capability acquisition — focus on suppliers with validated non‑GMO pipelines, traceable feedstock and proven technical application support.

- R&D and co‑development: Leverage ingredient partner roadmaps to fast-track reformulations that reduce dependency on higher‑fat variants and capture formulation premiums.

- Risk mitigation: Incorporate the report’s scenario matrix into treasury and procurement plans to stress-test margins against raw material and logistic shocks.

Methodology and credibility

PW Consulting’s forecast integrates a blended bottom-up and top-down approach. Historical series span 2020–2025 with 2025 as the base year. Forecasts cover 2026–2032, denominated in USD (revenues expressed in Million USD). Modeling inputs include: trade flows, measured plant capacities, public company disclosures, private supplier interviews, and price data for soybean meal and crush margins. Sensitivity testing and peer benchmarking underpin the stated CAGR of 5.72% for the forecast period.

Conclusion — the strategic choice for 2026

The Low Fat Soya Flour market presents a clear growth runway for firms that can align ingredient strategy with application innovation, supply resilience and differentiated certification. PW Consulting’s full report is designed to move leaders from insight to decision: it reveals where and how to invest, where to partner, and where to protect margins as the market scales through 2026 and beyond.

For the complete dataset, regional and application breakdowns, company-by-company scenario impact and our downloadable model, access the full PW Consulting Low Fat Soya Flour Market report. This preview demonstrates the analytical depth; the full study supplies the granular inputs you will need for 2026 strategic and transactional decisions.

For detailed analysis of this topic, please visit the official page:Low Fat Soya Flour Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com