Global Organopolysilazane Market Set to Reach USD 988.65 Million by 2032 Amid Rising Demand for High-Performance Coatings

Other |

2026-06-09 09:07:57

PW Consulting’s new Steel Idler Rollers Market report (base year: 2025; historical coverage: 2020–2025; forecast: 2026–2032) is designed for executive teams making capital, procurement, and product strategy decisions in 2026. The analysis combines macro demand projections with operational playbooks and competitive benchmarking to translate market trends into immediate, actionable choices.

Steel Idler Rollers Market

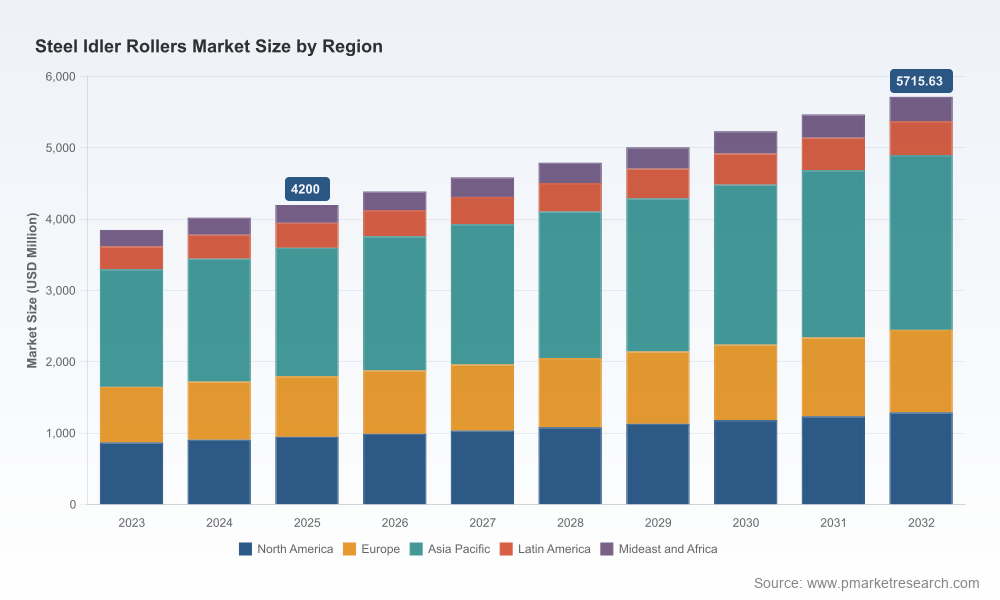

After steady expansion through the early 2020s, the global market for steel idler rollers reached approximately USD 4,200 Million in 2025. Our model projects the market to grow at a compound annual growth rate (CAGR) of 4.5% for the 2026–2032 forecast window, reaching an estimated USD 5,715.63 Million by 2032. The report lays out the drivers behind this trajectory and the sensitivity of those forecasts to raw-material volatility, infrastructure investment cycles and technology adoption.

Steel Idler Rollers Market

Bridge strategy to execution: We translate market momentum into practical initiatives—capital allocation scenarios, procurement hedging plans, and OEM aftermarket monetization pathways—that procurement and operations leaders can act on within 6–18 months.

Steel Idler Rollers Market

Unpack risk and margin levers: The analysis quantifies how steel-price swings and producer pricing trends materially affect unit economics for OEM and aftermarket players and presents mitigation levers, from contract design to component substitution strategies.

Reveal competitive asymmetries: With a highly fragmented supplier landscape, the report identifies pockets of consolidation, capability gaps and white-space opportunities for differentiated product and service offerings.

The report is structured to support tactical decisions as well as strategic planning. Key deliverables include:

Executive dashboard: Scenario-based revenue and margin forecasts (2026–2032) with sensitivity to steel-price bands and PPI movements.

Go-to-market playbooks: Sales and channel strategies for OEMs, distributors and aftermarket service providers, with recommended KPIs and contract structures.

Procurement & sourcing toolkit: Shortlist of hedging instruments, supplier-selection frameworks and supplier risk scorecards tailored to idler roller supply chains.

Product and technology roadmaps: Evaluation of coatings, bearing technologies and sensorized (“smart”) idlers with ROI models for retrofit vs. new-build scenarios.

CapEx & operations modeling: Factory footprint optimization, local content scenarios and labour-capex trade-off matrices to inform 2026 capital plans.

M&A and partnership scanner: Prioritized list of inorganic targets and JV archetypes, with integration checklists and value-creation timelines.

Compliance and safety playbook: Checklist to align product design and documentation with evolving safety and environmental requirements in bulk handling industries.

While demand is broad-based across mining, ports, logistics and manufacturing, industry concentration remains modest. Our concentration metrics indicate that the top three suppliers account for roughly one-quarter of the market (CR3 ~ 24.5%), and the top five roughly one-third (CR5 ~ 34.8%). This fragmentation creates opportunities for scale-driven cost optimization, niche technical leadership and aftermarket service differentiation.

The market is served by a mix of global players, regional specialists and vertically integrated suppliers. Below is a synthesis of comparative positioning among leading firms; the full report contains deeper company scorecards, financial proxies and capability maps.

Rulmeca (Italy): Recognized for heavy-duty steel rollers and a broad conveyor component portfolio. Strengths include international standards compliance and deep port/mining experience—positioned where ruggedness and cross-border supply reliability matter most.

Metso Outotec (Finland): Focused on mining and aggregates, with emphasis on durable, low-maintenance designs for abrasive environments. Strong aftermarket services and engineering credibility in high-wear contexts.

Continental (Germany): Integrates steel idlers into comprehensive conveyor systems, leveraging scale and systems-engineering capabilities for large bulk-handling installations.

ASGCO, Douglas Manufacturing, Precision Pulley & Idler (PPI), Martin Engineering, Superior Industries (USA): These players are notable for CEMA-compliant offerings, service networks and close customer relationships in the Americas.

HIC Universal (India), GCS Conveyor (China), Melco (South Africa), Fenner Dunlop (Australia/Netherlands): Regional manufacturers that combine cost competitiveness with localized support; attractive partners for expansion and retrofit playbooks in emerging markets.

Smart idlers and real-time monitoring: Product integrations such as the 2025 Smart Idler implementation demonstrate a clear path to predictive-maintenance monetization. Sensor-enabled rollers are moving from pilot to commercial service, changing aftermarket economics and opening subscription-style service revenues.

Material and surface innovation: Industry research in early 2026 highlights gains from self-lubricating bearings and advanced corrosion-resistant coatings that materially extend service intervals in aggressive mining environments.

Raw-material volatility is the single most consequential near-term risk. High-grade alloy steel pricing has exhibited material year-over-year swings (industry observations indicate variance as high as ~18% in peak periods). Producer Price Indexes for conveyor and conveying equipment manufacturing are also trending higher, underlining cost pressures across OEMs.

For 2026, procurement-led interventions are table stakes: multi-sourcing, price collars, and indexed long-term contracts linked to clear PPI or steel benchmarks. The report provides executable hedging templates and a supplier risk heat map to prioritize actions in the coming 12 months.

Demand in 2025–2026 is underpinned by continued infrastructure builds, port expansions and cement/aggregate investments—particularly in Southeast Asia and parts of the Middle East. These macro projects favor steel idler rollers over lighter alternatives due to superior load-bearing and durability characteristics that support compliance with mining and bulk-handling safety and efficiency regulations.

However, demand is uneven by application and region; the full dataset in our report provides granular, actionable segmentation (by region, type and application) to support market-entry sizing and sales-force prioritization. Note: this teaser intentionally omits specific segment values to preserve the commercial value of the full report.

Based on our scenario analysis, firms should prioritize the following initiatives this year:

Operational resilience: Reassess supplier concentration and near-source critical spares. Move from single- to dual-source strategies for high-risk alloy inputs and bearings.

Service-led growth: Convert maintenance customers to contracted-service or sensor-driven subscription models. Pilot retrofit programs in high-wear sites to prove unit economics before scaling.

Product differentiation: Invest selectively in coatings and self-lubricating bearings to extend service life by measurable margins; use TCO-based sales arguments with customers in mining and ports.

Price management: Adopt dynamic pricing tied to PPI or steel indices and upgrade sales contract terms to include pass-through provisions for raw-material swings.

M&A and partnerships: Pursue bolt-on acquisitions to secure aftermarket footprints or proprietary sensor integrations, and pursue JVs where local content and service proximity are key competitive advantages.

Executives who adopt the report’s playbooks will be able to: compress procurement lead times through supplier segmentation, improve installed-base uptime via targeted smart-idler pilots, and protect margin via indexed pricing and selective vertical integration. We provide the implementation templates—project timelines, budget envelopes and KPI trackers—so teams can move from decision to deployment in 90–180 days.

PW Consulting’s full Steel Idler Rollers Market report contains the detailed segmentation, regional and application-level forecasts, company scorecards, financial models and execution toolkits referenced in this preview. This executive preview intentionally omits the drill-down tables and segment-level values to protect the actionable intelligence reserved for subscribers and clients.

For procurement teams, OEM strategy groups and private-equity investors evaluating plays in bulk-material handling, obtaining the full report will provide the quantitative and operational templates needed to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Steel Idler Rollers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com