خدمات التجميل بالبوتوكس في الرياض

Health |

2026-05-18 12:23:35

As organizations plan budgets, R&D programs, and M&A activity for 2026, rigorous, decision-ready intelligence on the skin measurement instruments market is non‑negotiable. PW Consulting’s latest market research synthesizes seven years of market evolution (2020–2026 baseline) and a multi‑scenario forecast through 2032, offering the contextualized insight that senior leaders require: market trajectory, competitive positioning, regulatory inflection points, and practical go‑to‑market playbooks. This release is a strategic trailer — it surfaces the insights that matter while guiding readers to the full report for granular segmentation and financial models.

Skin Measurement Instruments Market

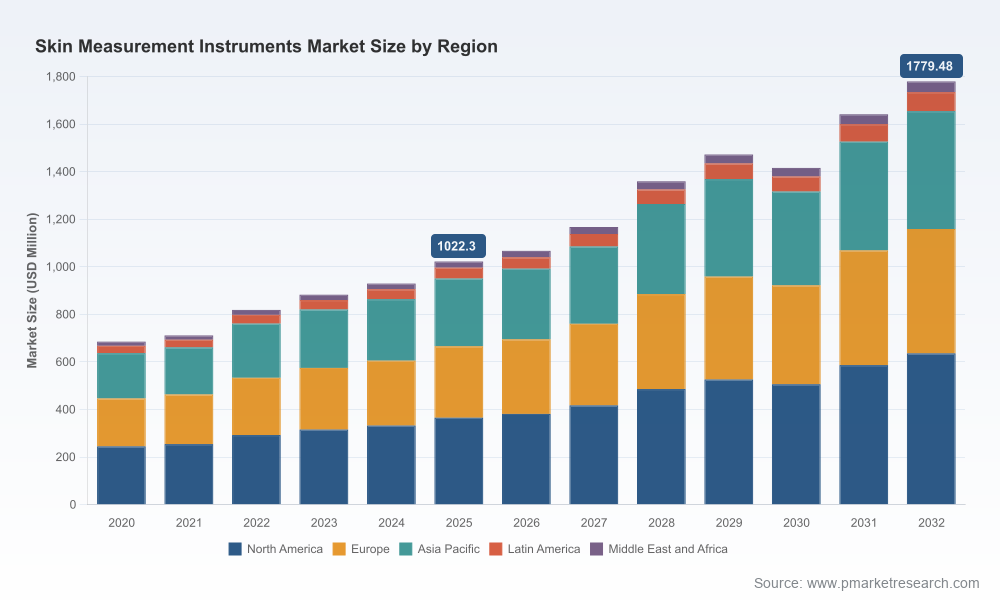

The skin measurement instruments market has moved from niche technical tools to a strategic platform underpinning cosmetic claims, clinical decision‑making, and personalized beauty services. Our benchmark shows the global market expanding materially across the 2020–2025 historical window and continuing on an upward path into the forecast horizon. From the early 2020s through the 2025 base year, the market size demonstrated robust recovery and accelerated demand, and our forecast models project continued expansion through 2032 at a compound annual growth rate of approximately 8.24%.

Skin Measurement Instruments Market

This growth is not uniform by use case or region — it is being shaped by three concurrent forces: (1) increased investment in AI‑enabled imaging and multi‑parameter platforms, (2) broader clinical adoption as regulatory clarity reduces approval friction, and (3) the migration of diagnostics‑grade capabilities into retail and point‑of‑care channels. The result is a market that is getting larger and more strategic, with capital equipment and software platforms emerging as higher value vectors for vendors and buyers alike.

Skin Measurement Instruments Market

Regulatory inflection: A notable regulatory development in 2026 reduces a major obstacle for certain optical diagnostic devices and electrical impedance spectrometers. The reclassification to Class II with special controls has opened the 510(k) pathway for a subset of devices, shortening time‑to‑market for feature‑rich optical and spectroscopic instruments. Organizations that align product design, clinical evidence generation, and regulatory strategy to the new pathways will secure first‑mover advantages in clinical and aesthetic channels.

Reimbursement and reimbursement‑adjacent policy: Payer and outpatient payment changes implemented for CY 2026 — including refinement of APCs and unbundling decisions related to select skin substitute and procedural codes — change the economics for device deployment in hospital outpatient settings. While skin measurement capital equipment is primarily deployed in clinics and research labs, these payment shifts affect procurement cycles, hospital service bundling, and cross‑departmental ROI calculations, and must be factored into contracting strategies.

Technology convergence: Our analysis identifies two simultaneous technical waves: precision metrology for biophysical parameters (hydration, TEWL, elasticity, pigmentation) and AI/3D imaging platforms that convert photos and scans into actionable diagnostic and commercial insights. Leading vendors are integrating imaging, multi‑probe measurement and analytics into unified suites — shifting buyer preference toward systems that deliver both measurement accuracy and interpretive intelligence.

The market’s vendor structure reflects moderate concentration: the leading three firms command a meaningful share, and the top five nearly half of the market by revenue — a profile that creates pockets of competitive advantage for established instrument specialists and opportunity for innovators on the periphery. Several archetypes emerge from our competitive mapping:

Gold‑standard metrology houses: Firms with long heritage in skin biophysics continue to set measurement benchmarks. Their instruments are commonly used in regulatory‑grade clinical trials and efficacy testing, and they leverage modular hardware platforms that scale across research and point‑of‑sale use cases.

Imaging and AI platform providers: Companies that combine high‑resolution imaging, 3D capture, and machine learning analytics are redefining consultation workflows in dermatology and aesthetic medicine. These platforms deliver quantifiable visual narratives that appeal to clinicians, marketers, and consumers.

Portable and point‑of‑care specialists: Lightweight, scientifically validated handheld devices are expanding clinical reach, enabling bedside or in‑clinic diagnostics, and supporting decentralized research protocols.

Representative players include global metrology leaders who provide gold‑standard probes and modular systems; imaging specialists delivering next‑generation 3D and AI analysis suites; and a cadre of regional and niche vendors supplying portable measurement devices and dermatoscopes. Recent company developments illustrate these dynamics: a major imaging firm launched a next‑generation system combining 3D capture with AI skin analysis in early 2026; a portable device provider published an application note expanding its tissue dielectric measurement use‑cases in late 2025; and regulatory reclassification in 2026 has materially altered the pathway calculus for optical diagnostic instruments.

Leaders planning 2026 investments should treat the skin measurement instruments market as both an operational procurement decision and a strategic battleground for customer engagement. The following actions have high strategic leverage:

Prioritize system‑level value over point features. Buyers increasingly prefer integrated solutions that couple reliable metrology with actionable analytics and patient/user workflows. Product roadmaps and procurement specs must reflect total solution economics (hardware, software, upgrades, and service) rather than unit price alone.

Align clinical evidence with regulatory strategy. The changed regulatory landscape accelerates pathways for certain optical and impedance devices, but sponsors must still invest in robust evidence packages that address the new special controls. Early planning of pivotal and supportive studies reduces approval risk and shortens commercialization timelines.

Build partnerships across the health‑beauty continuum. The most effective commercial plays link dermatology clinics, cosmetic R&D groups, and retail personalization channels. Pilot programs that demonstrate cross‑revenue synergies (e.g., device‑enabled consultations that drive service upsell or product conversion) create defensible, recurring revenue models.

Invest in field service and quality assurance. As instruments become more sophisticated, uptime, calibration, and validated SOPs are competitive differentiators. Vendors and buyers should quantify service economics during procurement and prioritize vendors with proven service networks and regulatory documentation.

Plan M&A and partnership plays around software and AI capabilities. Given the premium buyers place on interpretive analytics, strategic acquisitions or partnerships that accelerate AI capabilities can rapidly enhance platform value and market access.

For executives who require more than directional intel, the full PW Consulting report provides operational, transaction‑grade deliverables, including:

Forecast models with scenario sensitivity (base, upside, downside) through 2032, enabling NPV and IRR calculations for product investments and market entry plans.

Vendor heatmaps and a comparative technology matrix that evaluate measurement accuracy, regulatory readiness, integration capabilities, and service footprint.

Go‑to‑market playbooks for clinic, research, and retail channels — including pricing strategies, pilot design templates, and key performance indicators to monitor adoption.

Regulatory pathway guides keyed to device archetypes, with recommended clinical evidence plans aligned to the new US and European frameworks.

Commercial diligence materials for M&A and JV evaluation, including comparable transaction analysis and vendor due diligence checklists.

Because this release follows the “trailer” approach, we are intentionally reserving full segmented breakdowns, regional allocations, and modelled revenue curves for the comprehensive report. Those datasets are essential for execution — pricing, channel selection, and capex planning — and they are provided in the complete deliverable along with editable financial models.

Product teams: Re‑baseline roadmaps to emphasize interoperability and clinical evidence generation aligned with the new regulatory paths. Consider re‑scoping feature sets to expedite 510(k) filings where applicable.

Corporate development: Target bolt‑on acquisitions that expedite AI analytics or add point‑of‑care deployment expertise. Use our vendor heatmap to shortlist targets that close capability gaps quickly.

Commercial leaders: Pilot bundled offerings that pair measurement instruments with subscription analytics and service contracts; use pilot KPIs to build case studies for reimbursement and hospital adoption.

Clinical and research directors: Leverage validated portable devices to decentralize studies and accelerate recruitment; work with vendors whose documentation supports regulatory endpoints.

The skin measurement instruments market is maturing from a collection of technical tools into a strategic platform intersecting clinical diagnostics, cosmetic science, and consumer personalization. Market scale and forecast momentum underscore opportunity, while regulatory and reimbursement developments in 2025–2026 materially change commercialization pathways. Firms that take an integrated approach — combining rigorous metrology, software‑driven interpretation, regulatorily aligned evidence packages, and disciplined service economics — will convert technical capability into sustainable commercial advantage.

PW Consulting’s full report operationalizes these themes into the datasets and execution frameworks that senior leaders need to make 2026 investment, product, and partnership decisions with confidence. For access to the complete segmented models, vendor scorecards, and step‑by‑step regulatory guides, please visit our report landing page or contact our advisory team for a briefing.

For detailed analysis of this topic, please visit the official page:Skin Measurement Instruments Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com