Exhaled Nitric Oxide Detectors Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

Executive snapshot

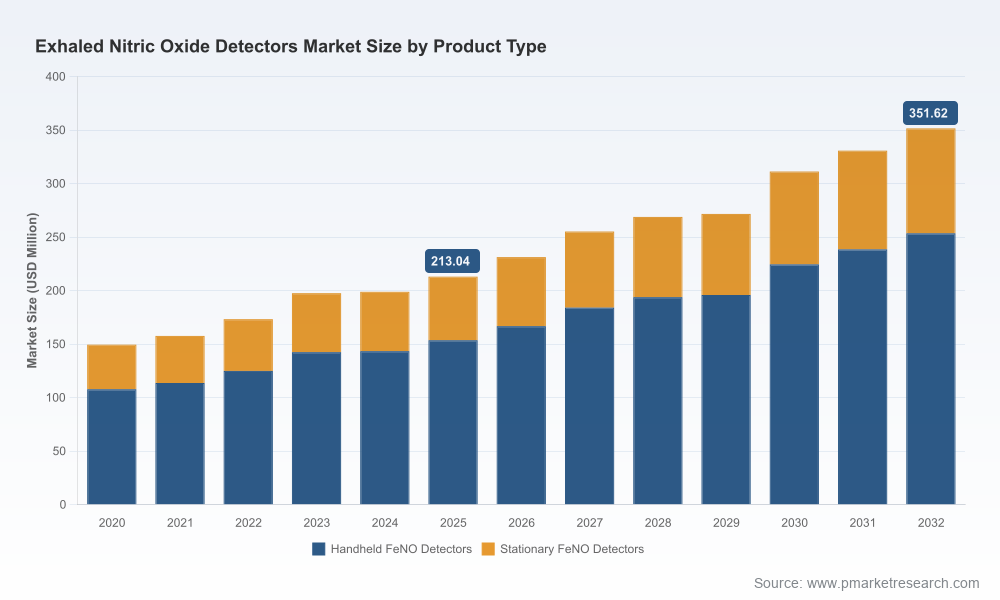

The Exhaled Nitric Oxide (FeNO) detectors market is transitioning from a niche clinical tool into a mainstream respiratory-care instrument with meaningful commercial scale. According to our latest market model, the market reached approximately USD 213.04 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 7.42% through the 2026–2032 forecast window, reaching roughly USD 352 Million by 2032. These headline figures understate a more nuanced reality: 2026 represents a tactical inflection point for device manufacturers, payers, and healthcare providers as guideline recognition, regulatory activity, and new product clearances converge to reshape adoption dynamics.

Exhaled Nitric Oxide Detectors Market

Why this matters to decision-makers in 2026

For commercial leaders, clinical strategy teams, and corporate development groups, the question for 2026 is not whether the FeNO market will grow, but how fast, where, and on what terms that growth will be won. The combination of updated guideline positioning, multiple recent regulatory clearances of portable systems, and emerging integration pathways into routine asthma care creates both opportunity and execution risk. The PW Consulting report offers the analytical scaffolding executives need to convert high-level growth into executable plans — from go-to-market and reimbursement strategies to product portfolio prioritization and M&A screening.

Exhaled Nitric Oxide Detectors Market

Market dynamics driving 2026 decision windows

- Guideline momentum: The expanded recognition of FeNO in the 2025 GINA guidance elevates the test from an adjunct research tool to a clinically endorsed biomarker for identifying Type 2 airway inflammation. That endorsement shortens the adoption runway for primary care and specialist clinics comfortable aligning practice to international guidance.

- Regulatory inflection: Multiple executive-level regulatory events in late 2025 and early 2026 — including new 510(k) clearances for portable analyzers — lowered barriers for market entry and broadened the set of devices able to be used in point-of-care environments. These approvals are not merely paperwork: they materially change purchasing committees’ risk calculus around device procurement and workflow redesign.

- Clinical workflow & technology design: Innovations that reduce breath-hold time, simplify calibration, and enable both online and offline measurement fundamentally change clinical throughput economics. Devices that shorten test time and fit within primary-care visit time budgets will accelerate adoption faster than superior-but-cumbersome reference systems.

- Reimbursement and pricing dynamics: Established fee structures, reimbursement packaging in outpatient settings, and modest per-test payments mean that sustainable adoption requires a value narrative that links FeNO measurement to demonstrable improvements in medication stewardship, reduced exacerbations, or downstream cost avoidance.

- Consolidation of commercial power: The competitive set is concentrated: a small group of established medical-device firms and specialist manufacturers dominate clinical mindshare. New entrants must therefore plan either for targeted niche disruption or for partnership strategies that offset go-to-market limitations.

Competitive landscape — what to watch

Leading global and regional players are actively shaping the market through product refinement, regulatory filings, and evidence generation. Among the firms commanding attention:

Exhaled Nitric Oxide Detectors Market

- NIOX Group plc (Circassia) — The NIOX VERO platform has been positioned strongly against ATS/ERS standards and benefits from longstanding clinical acceptance, particularly where guideline alignment is a procurement criterion.

- Bedfont Scientific — Known for cost-effective portable solutions and incremental clinical evidence supporting integration into asthma care pathways; recent publications highlight improved asthma control when FeNO testing is incorporated.

- Bosch Healthcare Solutions — Recent regulatory clearance for a portable FeNO system accelerates a larger industrial player’s push into point-of-care respiratory diagnostics.

- MGC Diagnostics (affiliated with CAIRE) — Commercial positioning around unique workflow features (e.g., rapid breath maneuver approvals) addresses clinic throughput constraints and expands device use cases.

- ECO MEDICS — Maintains strength on the reference analyzer side with chemiluminescence systems, anchoring precision use cases in research and tertiary centers.

- Regional manufacturers (select China-based firms) — Offering competitive handheld analyzers suitable for both online and offline use, these players are important for pricing dynamics and for non-traditional distribution channels in emerging markets.

Recent developments to track closely include regulatory clearances in late 2025 and product updates through early 2026, which together lower friction for purchasers but also intensify competitive pressure on pricing and clinical differentiation.

What the PW Consulting report delivers — practical, transaction-ready intelligence

Our research is structured to support immediate 2026 decision cycles. The full report contains:

- Proprietary market-sizing and scenario modelling with bottom-up and top-down reconciliations to quantify addressable channel opportunity under three clinical adoption scenarios.

- Regulatory and reimbursement playbooks that map pathway timelines, evidence thresholds, and payer engagement levers across major markets.

- Clinical evidence prioritization matrices that rank use cases (diagnosis, treatment monitoring, population screening) by expected incremental clinical and economic value.

- Go-to-market playbooks for incumbent vendors and new entrants: channel selection, distributor negotiation tactics, pricing architectures, and service/consumable strategies.

- M&A and partnership screens: a short list of capability gaps, target archetypes, and valuation sensitivities for bolt-on acquisitions or licensing deals.

- Technology and operations assessment: lifecycle forecasts, manufacturing scale considerations, supply-chain risk heatmaps, and quality/regulatory compliance checklists for rapid commercialization.

Actionable strategic recommendations for 2026

- Prioritize rapid regulatory and evidence wins: If you are a device supplier, secure 510(k)-equivalent clearances early and invest in targeted clinical studies that demonstrate real-world impact on treatment decisions and outcomes — not just analytical performance.

- Design for point-of-care economics: Usability, test duration, and integration with electronic health records are decisive features for primary-care adoption. Device specifications that reduce visit time and administrative burden win procurement tenders.

- Build payer narratives tied to outcomes: Given existing payment structures, commercial success requires showing that FeNO-guided care reduces exacerbations, medication overuse, or downstream utilization. Prioritize health-economic models that translate test use into dollars saved at the episode-of-care level.

- Decide your competitive posture: New entrants should choose between two viable routes — differentiated clinical performance (reference/precision use cases) or price/performance leadership in primary care. Hybrid strategies are costly and slow.

- Leverage partnerships to accelerate scale: Distribution alliances, bundled offerings with spirometry or chronic-care platforms, and co-development with EHR vendors can compress time-to-adoption.

- Prepare for consolidation and M&A activity: Expect acquisitive moves around niche technology plays and consumable-driven business models; have a readiness plan with valuation thresholds and integration playbooks.

Risks and watchpoints for corporate boards

While growth is robust, executives must manage several risks: evolving regulatory interpretations of flow-dependent accuracy requirements; payer scrutiny of unit economics; potential commoditization triggered by low-cost regional players; and the clinical adoption gap between specialist centers and primary-care settings. These are manageable risks if addressed early with regulatory, clinical, and commercial investments aligned to the 2026 decision calendar.

How PW Consulting can accelerate your 2026 plan

We designed the report as a decision-support toolkit for 2026: a concise executive briefing, an analyst-ready dataset for integration into corporate financial models, and a playbook for rapid execution. Our advisory work combines device-clinical-regulatory expertise with payer negotiation experience and M&A execution capability — the combination most frequently requested by device CEOs and corporate development teams preparing for accelerated rollouts or sale processes.

Next steps — obtain the full intelligence

This preview highlights the strategic contours and why 2026 offers a compressed window of opportunity. To access the full market model, segmented demand scenarios, granular country- and channel-level analyses, and our proprietary vendor scoring (intended to support procurement and M&A diligence), please consult the full PW Consulting Exhaled Nitric Oxide Detectors Market report on our website. The detailed datasets and appendices contain the actionable segmentation and unit economics that underpin the strategic recommendations summarized here.

For immediate advisory support, bespoke scenario modelling, or to schedule a briefing with our respiratory diagnostics practice, contact PW Consulting’s healthcare strategy team. The choices you make in 2026 will determine whether you are a market leader in 2030 — and we are prepared to help you make those choices with conviction.

For detailed analysis of this topic, please visit the official page:Exhaled Nitric Oxide Detectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com