How Are Automation and Smart Manufacturing Driving the Automatic Labeling Machine Market?

Other |

2026-03-13 09:35:46

PW Consulting’s newest market research release on the Mango Kernel Fat market synthesizes primary interviews, plant-level capacity mapping, and a multi-scenario financial model to deliver an actionable strategic outlook for 2026 and beyond. The market has evolved from a niche by‑product play into a recognizable specialty fats category: total industry revenue expanded materially between 2020 and 2025, reaching USD 230.65 Million in our base year (2025). Our forecast model — calibrated to macro trends, capex announcements and elasticities in end-markets — projects the market to grow at a compound annual growth rate (CAGR) of 7.89% over the 2026–2032 horizon. By the end of the forecast window the sector is expected to be approaching mid‑hundreds of millions in annual sales under the base scenario.

Mango Kernel Fat Market

Mango kernel fat’s transition into commercial relevance is driven by three converging dynamics. First, formulators in personal care and specialty confectionery continue to seek plant‑derived emollients and cocoa butter replacers that meet consumer demand for natural and traceable ingredients. Second, food manufacturers are experimenting with more cost‑efficient or functionally equivalent fats to broaden formulation flexibility. Third, regulatory and procurement emphasis on traceability and certification (organic, sustainable sourcing) has elevated the premium attached to verifiable supply chains.

Mango Kernel Fat Market

These demand drivers, combined with documented raw-material economics (mango kernels typically contain between 9%–18% oil by weight), underpin the structural growth assumptions in our model. Seasonality and the fact that kernels are a byproduct of mango processing create episodic supply dynamics; processing economics (cold‑press vs solvent fractionation) further determine which grades enter cosmetics vs food pipelines.

Mango Kernel Fat Market

Understanding feedstock logistics is essential. Mango kernels originate as a downstream output of fruit processing; sourcing is concentrated in major tropical producing regions and often involves complex rural supplier networks, including smallholder and community groups. These sourcing models create both resilience and vulnerability: they enable social impact narratives and cost advantages, but introduce traceability and quality control challenges.

On the processing front, technology choices materially affect grade, yield and margin. Cold‑pressed production preserves native characteristics and supports organic/clean‑label positioning; solvent fractionation enables higher throughput and tailored melting profiles suitable for confectionery and industrial formulations. Notably, recent industry filings and corporate announcements indicate a step‑change in large‑scale fractionation capacity coming online — moves that create the potential for downward pressure on commodity‑grade margins while enabling expanded specialty-grade outputs for premium applications.

The market comprises a mix of upstream processors, specialist ingredient houses and global distributors. Leading firms span origin producers with deep rural procurement networks, European processors with global B2B distribution platforms, and North American formulators that brand and blend specialty grades.

Recent corporate developments are illustrative of strategic intent. A prominent origin processor announced a multi‑year expansion that includes a new processing subsidiary in West Africa and a large solvent fractionation unit commissioned to scale specialty fats production. These moves materially increase available refined and fractionated capacity and alter the competitive dynamics for both commodity and specialty grades.

Market concentration measures show leading groups capturing a significant share of the market without absolute dominance, indicating room for consolidation activity while preserving opportunities for nimble niche players. For executives this implies a two‑track competitive approach: defend and fortify core supply agreements while pursuing targeted partnerships or bolt‑on acquisitions to capture specialized capabilities (cold‑press, organic certification, downstream blending).

Mango kernel fat is traded within established HS classifications for fixed vegetable fats and oils. Regulatory emphasis on sustainable sourcing, traceability, and organic credentials is increasing, especially in cosmetics and food channels that feed Western markets. Compliance with local food safety standards and international labeling requirements should be factored into supplier onboarding and product launch timelines. Certifications are often decisive in commercial contracts and can justify price differentials where traceability is a procurement imperative.

Price formation reflects raw‑material seasonality, processing mix, and the degree of value‑adding (refinement, fractionation, certifying). The influx of new fractionation capacity can widen availability of tailored melting profiles, but also introduces short‑term supply gluts for certain commodity grades. Buyers and sellers should adopt contract designs that balance volume guarantees with flexibility: indexed pricing, tiered quality premiums, and capacity reservation agreements coupled with penalty/bonus mechanisms will be central to stabilizing margin outcomes through 2026–2028.

Our market report is designed as a strategic toolkit for commercial, procurement and strategic teams. Key practical deliverables include:

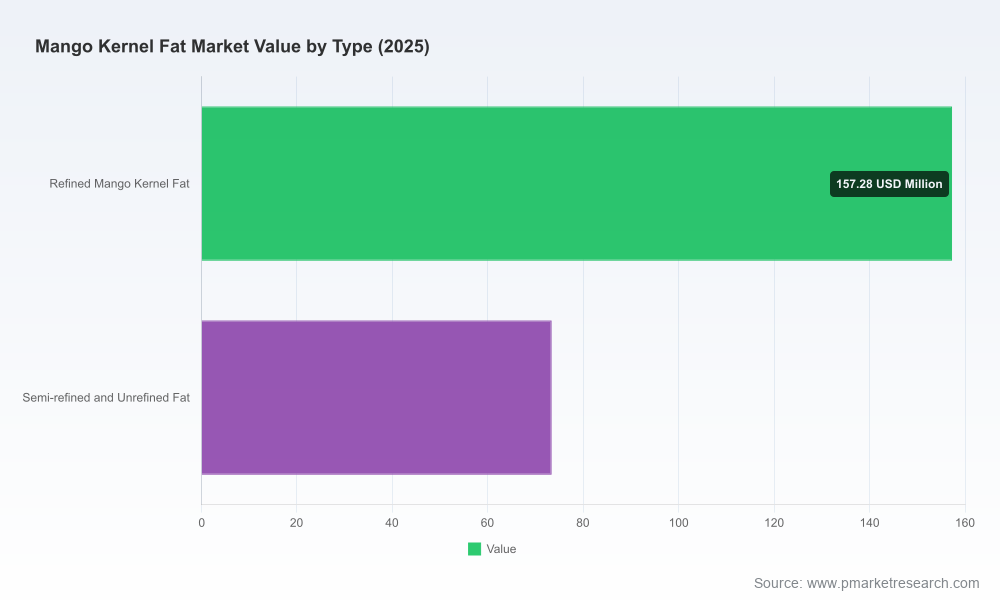

To preserve commercial sensitivity we have intentionally withheld detailed sub‑segment allocations and region/application-level splits from this public summary. These datasets — including granular regional demand curves, application mixes and supplier capacity tables — are available in the full report and accompanying Excel models.

PWC Consulting’s Mango Kernel Fat market study reframes a by‑product into a strategic raw material class with implications across procurement, product development and corporate strategy. 2026 is a pivotal year: capacity additions are reshaping supply economics while end‑market demand for natural, traceable and functional plant fats continues to strengthen. Firms that combine disciplined sourcing, tactical investments in processing capability and robust supplier governance will capture disproportionate value.

For immediate access to the complete dataset, sub‑segment forecasts, supplier scorecards and the buildable model that underpins our scenarios, contact PW Consulting or visit our report landing page. The full intelligence package is intended to support the 2026 planning cycle and equip teams to move from insight to implementation within 90 days.

For detailed analysis of this topic, please visit the official page:Mango Kernel Fat Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com