Skin Whitening in Dubai: Modern Approach to Skin Clarity

Other |

2026-04-27 10:44:09

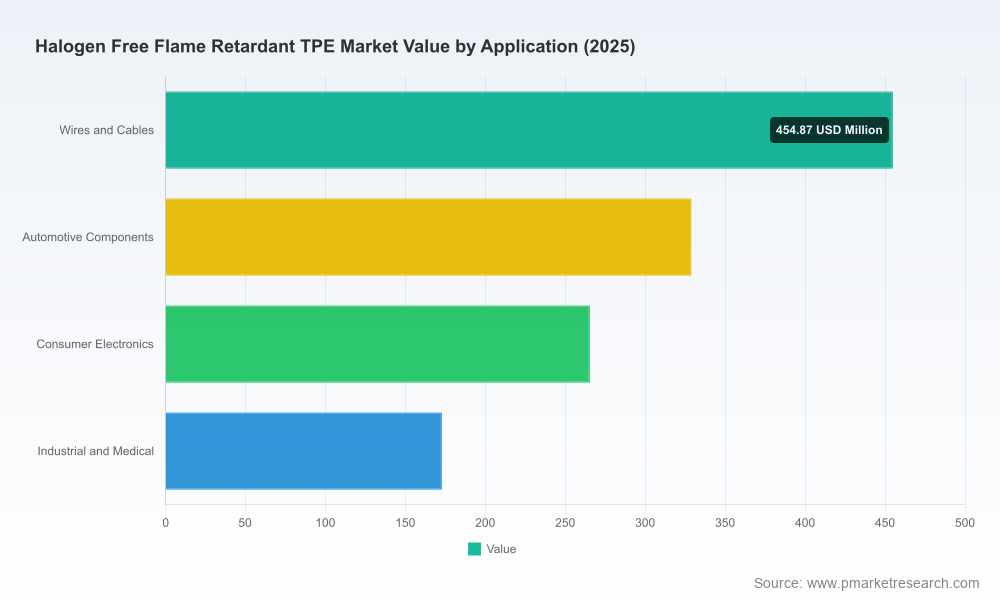

PW Consulting today releases a strategic briefing drawn from our forthcoming Halogen‑Free Flame Retardant (HFFR) Thermoplastic Elastomer (TPE) Market report. Built on a five‑year historical baseline and a seven‑year forecast window, the dossier synthesizes primary interviews, proprietary supply‑chain modeling and scenario analysis to inform executive choices in 2026. The total market reached approximately USD 1.22 billion in our 2025 base year and, riding a compound annual growth rate of roughly 7.5% for the forecast horizon, is projected to exceed USD 2.0 billion by 2032. Our concentration analysis also indicates a moderately consolidated supply base (CR3 ~38.5%; CR5 ~54.2%), a structural detail with direct implications for sourcing strategy and M&A.

Halogen-Free Flame Retardant TPE Market

Timing pressure: 2026 is a decision year where product roadmaps, supplier contracts and certification timelines converge. The market’s sustained growth trajectory means firms delaying strategic commitments face higher entry costs, longer qualification cycles and potential supply bottlenecks.

Halogen-Free Flame Retardant TPE Market

Regulatory inflection: Safety‑critical standards (including IEC and RoHS frameworks, and regional rail standards driving DIN EN 45545‑2 compliance) are tightening acceptance criteria for low‑smoke, low‑toxicity HFFR formulations. Early alignment reduces rework and accelerates time‑to‑market in rail, automotive and infrastructure segments.

Halogen-Free Flame Retardant TPE Market

Margin and performance tradeoffs: Technology choices—phosphorus‑based chemistries versus mineral fillers—have distinct implications for mechanical properties, processing and price volatility. Companies need forward models that quantify those tradeoffs into product and procurement strategies.

Consolidation windows: With more than half the market served by the top five players, 2026 is an opportune year for acquisitive expansion or bolt‑on partnerships to secure compounding capabilities, certification know‑how and regional manufacturing footprints.

Robust market architecture: Transparent methodology, reconciled historicals (2020–2025) and a detailed 2026–2032 forecast model that captures demand drivers, substitution dynamics and pricing elasticities.

Scenario toolset: Three market trajectories (Baseline, Accelerated Adoption, Policy‑Driven Acceleration) with sensitivity levers for raw material price shocks, regulatory tightening and end‑market adoption rates—designed for boardroom strategy sessions.

Practical commercial playbooks: Go‑to‑market options for incumbent polymer compounders and new entrants—covering positioning, channel strategy, sample-to-production qualification timelines and margin build‑up.

Supply‑chain and raw material deep dive: Cost‑to‑serve models, key upstream vulnerabilities (including phosphorus feedstock dynamics and mineral‑filler loading effects), and recommended contracting strategies to mitigate price pass‑throughs.

Regulatory and certification roadmap: A compliance matrix linking product specs to the most relevant global and regional standards, plus a step‑by‑step certification playbook for safety‑critical segments such as rail and medical.

Competitive benchmarks and technology scouting: Proprietary scorecards evaluating supplier capabilities across formulation breadth, certifications, manufacturing scale, sustainability credentials and route‑to‑market strength.

M&A and partnering target shortlist: Screening criteria and prioritised profiles for targets that can close capability gaps quickly, including integration risk assessments.

Avient Corporation (Avon Lake, Ohio): Positioning around sustainable credentials and market‑ready, bio‑based/recycled HFFR TPE grades for consumer electronics and cable jacketing. Their emphasis on UL94 V‑0 performance combined with circular content is a template for premium differentiated offerings.

RTP Company (Winona, Minnesota): Broad portfolio depth and RoHS‑aligned formulations make RTP a resilient supplier for diversified industrial applications—particularly where multi‑material compliance and custom compounding are table stakes.

Teknor Apex (Pawtucket, Rhode Island): Focused on low‑smoke HFFR TPEs that deliver PVC‑comparable processing and performance. Their narrative underscores the commercial opportunity to displace legacy materials through easier processing and lower total cost of ownership.

KRAIBURG TPE (Waldkraiburg, Germany): A clear play in safety‑critical verticals. Recent launches and updated technical fact sheets emphasize third‑generation HFFR series engineered for rail applications and DIN EN 45545‑2 compliance—sharpening the bar for tear resistance, PP adhesion and smoke toxicity metrics.

HEXPOL TPE (Malmö): Product ranges targeted at ignition resistance and low‑smoke performance reveal demand at higher technical tiers, particularly where UL94 V‑0 ratings at variable thicknesses matter.

Angreen Advanced Material Technology (China): A competitive force in wire and cable formulations with a stated focus on EV and 5G ecosystems—areas with accelerating HFFR demand and regional sourcing advantages.

Elastron USA (part of Elastron Group): Niche leadership with copper‑stabilized halogen‑free TPV grades addressing UV/ozone resistance and polyolefin bonding—illustrating the value of specialty additives and fit‑for‑purpose properties.

Notable recent market activity we tracked includes KRAIBURG’s March 2025 launch of a next‑generation HFFR TPE series designed for high fire protection in rail (DIN EN 45545‑2 R22/R23 HL3 compliance), a subsequent fact‑sheet update confirming UL94 V‑0 ratings in late 2025, and a series of trade‑show presentations in 2025 spotlighting future development and collaboration opportunities across Chinese and international compounders. These moves reflect both product innovation and an intensifying race to secure certification leadership in safety‑critical markets.

Raw material choices are decisive. Phosphorus‑based flame retardants enable lower filler loadings and preserve TPE mechanical performance, while mineral systems (ATH/MDH) often require higher loadings that can compromise elasticity and processability.

Upstream feedstock volatility—particularly in phosphorus intermediates—has a near‑immediate pass‑through effect on compounded formulations. Procurement strategies must therefore balance spot exposure with long‑dated contracts and inventory buffers.

Regulatory tightening on smoke toxicity and halogen content is redirecting specifiers away from legacy halogenated systems and toward validated HFFR solutions. Certification lead times are non‑trivial and should be accounted for in product roadmaps.

End‑market accelerants—electrification, 5G rollout and rail modernization—are increasing demand for low‑smoke, halogen‑free solutions across cables, connectors and safety seals, creating pockets of premium growth.

Prioritise supplier qualification now: Lock in Tier‑1 compounding partners with certified production lines and documented UL/DIN test heritage to shorten qualification timelines.

Invest selectively in phosphorus‑chemistry R&D: Where product performance is a differentiator, lower loading phosphorus systems deliver superior mechanical profiles and faster route‑to‑certification—offsetting near‑term material cost differentials.

Diversify feedstock contracts: Hedge phosphorus and key additive exposure through a mix of spot, forward and strategic partner agreements to reduce margin volatility.

Design certification roadmaps to pre‑empt regulation: Map product families to applicable standards early and embed testing milestones into development sprints to avoid late‑stage redesigns.

Evaluate bolt‑on acquisitions or JV structures: Target capabilities that close formulation, certification or regional manufacturing gaps; even modest consolidatory steps can materially improve CR‑adjusted market access.

Adopt modular specifications for OEM customers: Create graded product families (e.g., UL‑qualified, rail‑qualified, bio/recycled content variants) to rationalise SKUs while addressing premium and volume needs.

This briefing is a strategic preview. The full PW Consulting Halogen‑Free Flame Retardant TPE Market report contains the comprehensive regional and application segmentation tables, supplier scorecards, unit price curves, sensitivity models, interview transcripts and downloadable financial models that underpin the recommendations above. For procurement leaders, product heads and corporate development teams preparing decisions in 2026, the extended dataset and scenario tools are designed to convert uncertainty into executable plans.

Contact PW Consulting or visit our report page to review the full table of contents, order the report package, or schedule a bespoke workshop to translate the findings into a tailored 24‑month action plan.

For detailed analysis of this topic, please visit the official page:Halogen-Free Flame Retardant TPE Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com