Process Analyzer Market Size, Share, Current Trends, and Forecast by 2033

Other |

2026-06-10 09:18:48

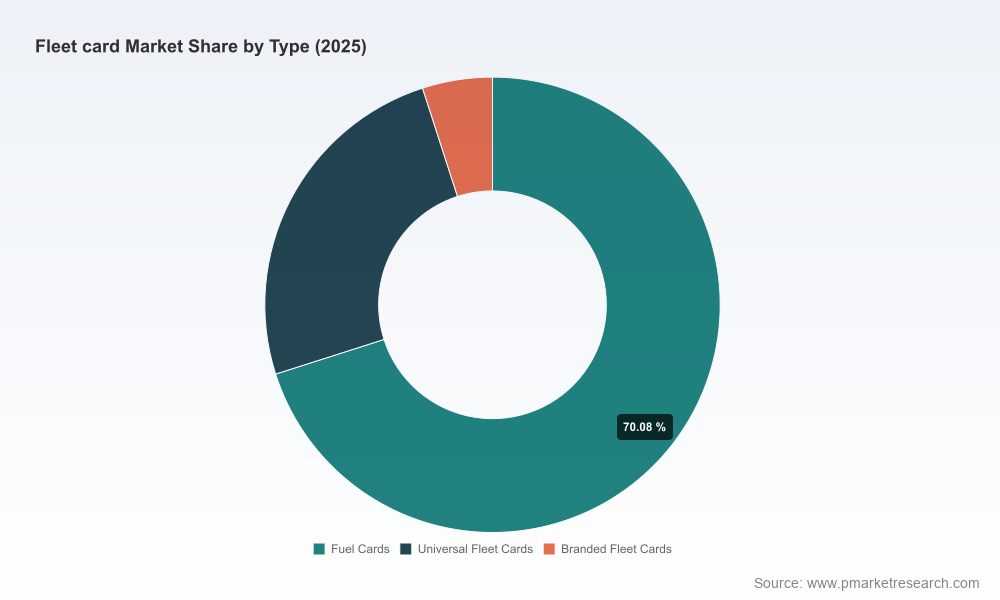

PW Consulting’s latest Fleet Card Market research—anchored on a 2025 base year and projecting through 2032—translates emerging market dynamics into actionable choices for executives preparing 2026 budgets and strategic roadmaps. Our top-line analysis finds the global fleet card market at approximately USD 28.5 billion in 2025, on a trajectory to reach the low‑to‑mid forty‑billion range by 2032 under a compound annual growth rate (CAGR) of roughly 6.5% for the 2026–2032 forecast window. These macro trends create distinct inflection points for product, commercial and capital-allocation decisions in the year ahead.

Fleet Card Market

Timing: 2026 is the year when fleet programs must reconcile legacy fuel-card economics with accelerating digital payment and mobility stacks. The market’s steady mid-single‑digit CAGR masks compositional shifts—where network reach, data integrations, and EV charging support are differentiators.

Fleet Card Market

Capital allocation: With consolidation still concentrated (a three‑firm concentration near half the market and a five‑firm concentration north of sixty percent), incumbents and challengers must weigh organic investment against acquisitive growth to secure distribution and data assets.

Fleet Card Market

Commercial contracts: Procurement teams will demand more than price-per-gallon concessions—expect negotiation leverage to tilt toward vendors that provide real‑time spend controls, telematics data harmonization and integrated EV charging bilaterals.

High‑level sizing shows a resilient market expanding from the mid‑twenty billions in the early 2020s to an estimated USD ~44.3 billion by 2032 under our baseline scenario. That expansion reflects a combination of increased commercial mileage, tighter expense governance by fleet operators, and the incremental revenue opportunity from adjacent services (maintenance, tolling settlements, and EV energy services). While headline growth is predictable, the strategic value lies in customer‑level economics: margins concentrate around who controls authorization, reconciliation and cross‑channel rebates, not merely fuel discounts.

We intentionally withhold granular regional and application splits in this release to preserve the integrity of our proprietary models—access to the full dataset and the accompanying scenario tool is available through the report landing page.

Demand and supply forecasts with scenario modules (baseline, accelerated electrification, recessionary demand shock) calibrated to fleet telematics and freight activity indicators.

Competitive scorecards—quantifying network coverage, product breadth (closed‑loop vs. universal), telematics and EV integrations, and go‑to‑market capabilities—designed for vendor selection and partner prioritization.

Playbooks for commercial teams: negotiation scripts, incentive structures, and co‑marketing frameworks to accelerate adoption among small-to-medium fleets and enterprise accounts.

M&A heatmap and valuation sensitivities: target archetypes, expected multiples by capability (network access, data platforms, payment flows) and integration red flags.

Operational readiness checklists for product and IT teams: API standards, fraud and authorization policies, reconciliation workflows, and EV charge point settlement templates.

Regulatory and compliance tracker with remediation scenarios for fuel transparency mandates and data‑privacy regimes relevant to telematics-linked billing.

Executive dashboards and an interactive model that lets you test margin, penetration and pricing levers against the forecast horizon.

The market remains a blend of energy majors, card specialists and financial services firms. Each class pursues a distinct strategic play:

Card specialists (e.g., WEX Inc.): Their core advantage is neutral acceptance networks and deep integration capabilities with telematics and back‑office systems. WEX’s broad acceptance footprint and investments in EV charging and real‑time controls position it as a prime partner for fleets wanting vendor‑agnostic routing and reconciliation. Their risk: margin pressure if rebates and interchange compression accelerate.

Payments incumbents (e.g., Corpay/brands historically under FleetCor): These players scale through product breadth and enterprise sales. Recent product launches focused on mixed fleets and real‑time expense monitoring illustrate their move from pure payment instruments toward integrated spend platforms. Expect continued investment in analytics to defend enterprise accounts.

Energy majors and branded programs (Shell, BP, ExxonMobil, Chevron, TotalEnergies): Branded cards leverage station networks and loyalty programs; partnerships with card specialists expand acceptance and EV charging options. Their edge is physical network control and fuel procurement bargaining power, but their challenge is competing on neutral, cross‑brand data services that many fleets now demand.

Regional specialists and mobility service providers (DKV Mobility, UTA Edenred, Radius, World Kinect): These providers dominate in corridor and cross‑border trucking markets by bundling tolling, VAT reclaim and service payments. Growth depends on extending digital integrations and monetizing cross‑border financial services.

Financial institutions (e.g., U.S. Bancorp’s Voyager): Banks win on procurement financing, wide PSP linkages and government fleet relationships. Their challenge is to couple financial depth with product‑level features that fleets find sticky—detailed reporting, granular spend controls and industry‑specific reconciliation workflows.

Recent competitive moves validate our strategic thesis. In 2025, Corpay introduced a mixed‑fleet product emphasizing high rebates and real‑time expense visibility—reinforcing the shift toward hybrid solutions that blend discounting and data. Shell’s updated card offering, launched in partnership with a major card specialist, expanded EV charging support and U.S. network acceptance, signaling acceleration of cross‑industry partnerships. Earlier market outlooks published by major players underlined a marketplace in transformation: incumbents are publicly acknowledging the need to integrate mobility, payments and energy services into a single customer proposition.

Electrification: EV charging is no longer a fringe capability; fleets and vendors must integrate charger billing, roaming agreements and energy settlement into card platforms. That creates an upsell path but also requires new clearing and settlement logic.

Data convergence: Telematics and card authorization data form the basis of policy enforcement (geo‑fencing, route‑based authorizations) and predictive maintenance billing. Vendors with robust APIs and data normalization frameworks will capture higher lifetime value.

Regulatory shifts: Heightened demands for fuel transparency and near‑real‑time reporting—coupled with an open‑internet baseline established by recent regulatory changes—favor providers that can demonstrate auditability, privacy compliance and interoperability.

Freight and activity trends: A meaningful uptick in freight activity supports service expansion beyond fuel—fleet maintenance, tolling and value‑added settlement services are areas of incremental monetization.

For CFOs: Reallocate a portion of vendor rebate and card‑program budgets toward analytics and integration—these are now differentiators in pricing negotiations and customer retention.

For Product Leaders: Prioritize EV charging settlement, telematics integration and a developer‑friendly API layer. Run a 60‑day vendor sprint to validate integration proofs of concept with top 3‑5 customers.

For Business Development: Seek strategic partnerships early with network owners and roaming aggregators to secure acceptance breadth for mixed fleets; structure pilot commercial terms that can scale into exclusive offers for targeted segments.

For M&A Teams: Target data‑rich tuck‑ins (fleet telematics, route optimization providers, fuel‑site aggregators) rather than capex‑heavy station portfolios—data buys accelerate differentiation faster.

For Compliance and Operations: Establish near‑term roadmap items for real‑time reporting and fuel‑use audit trails to preempt regulatory requirements and to support sales conversations with enterprise fleet customers.

As the fleet card market enters a phase where payments, fleet operations and energy services converge, 2026 will reward organizations that treat cards as hubs of operational control and data monetization rather than only instruments of purchase. PW Consulting’s Fleet Card Market report provides the forecasting, competitive benchmarking and operational playbooks that boards, CFOs and product leaders need to make defensible, time‑sensitive investments.

This release is a strategic preview: it surfaces the report’s most actionable conclusions while reserving our full segmentation tables, scenario models and proprietary company scorecards for report subscribers. For the complete dataset, interactive forecast model and vendor scorecards that inform executable go‑to‑market plans, please visit the PW Consulting report landing page.

For detailed analysis of this topic, please visit the official page:Fleet Card Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com