Experts Predict Germany's Smart Grid Meters Market Will Thrive

Other |

2026-05-11 06:40:08

PW Consulting’s latest Smart Transmitter Market report (base year 2025) delivers a concise, decision-ready roadmap for executives preparing capital allocation, procurement, and digital transformation strategies in 2026. Built on a quantitative foundation and forward-looking scenario analysis, the study explains why smart transmitters will remain a core enabler of process automation and IIoT-driven efficiency through the remainder of the decade.

Smart Transmitter Market

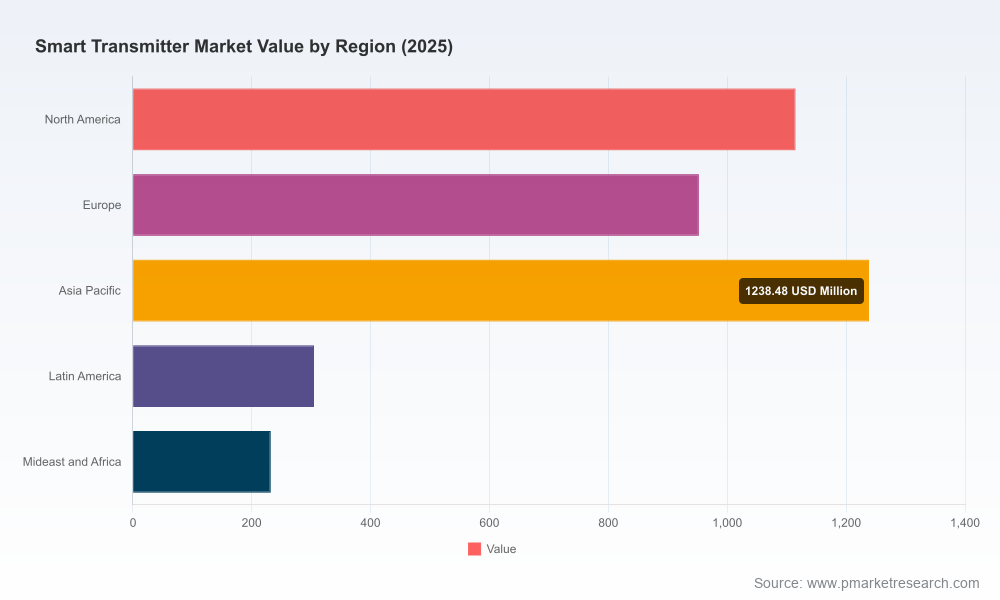

The smart transmitter market reached a robust scale by 2025 and resumes growth entering 2026, underpinned by steady industrial automation investments and intensified requirements for diagnostics, remote monitoring, and digital interoperability. Our forecast period (2026–2032) projects a mid-single-digit compound annual growth rate of 5.4%, reflecting a market that is both mature and primed for incremental modernization.

Smart Transmitter Market

Market concentration data indicate a moderately consolidated supply base: the three largest suppliers account for a meaningful share of industry revenue, and the top five capture well over half the market. This concentration shapes competitive dynamics — established players wield distribution, integration partnerships, and standards influence, while mid-tier and specialist vendors compete on application-specific performance, price, and service agility.

Smart Transmitter Market

The smart transmitter market is driven by five converging forces. First, industrial customers continue to demand higher-fidelity measurements and embedded diagnostics to reduce unplanned downtime. Second, digital communication protocols and field-level Ethernet technologies are moving from pilot to standard practice, enabling richer device-level telemetry and asset-centric analytics. Third, regulatory and standards evolution is raising the bar for testing and calibration processes. Fourth, energy transition and water efficiency initiatives are creating pockets of accelerated investment. Finally, component supply risks — notably semiconductor constraints — introduce both disruption and premium pricing opportunities.

The market’s competitive map is characterized by a mix of global platform incumbents and focused specialists. Leading industrial automation groups leverage broad portfolios and systems-level partnerships, while regional and niche vendors compete on performance, cost, and service agility. Below is a synthesized view of core players and the strategic implications for customers and partners.

Emerson’s strength lies in deep integration with process automation systems and broad protocol support (HART, FOUNDATION Fieldbus, wireless). Their position makes them an attractive choice for large-scale brownfield upgrades where interoperability with legacy control systems is paramount.

ABB emphasizes high-performance digital pressure transmitters and recently previewed an expanded P-Series portfolio. ABB’s product cadence and global service footprint are advantages for utility and industrial customers seeking ultra-accurate measurement and lifecycle services.

Yokogawa’s offerings focus on advanced diagnostics and robust digital protocol support, positioning them well in process-intensive segments where measurement assurance and long-term reliability are critical.

Honeywell highlights IIoT connectivity and predictive maintenance features. Their value proposition is compelling for operators pursuing asset performance management and predictive asset health initiatives.

Siemens integrates transmitters tightly into automation and control ecosystems, making them a natural partner for greenfield projects driven by digital twin and plant-wide optimization programs.

Endress+Hauser is notable for field-oriented innovations (Bluetooth, Ethernet-APL support) and strong application know-how, especially in water and process industries where easy commissioning and diagnostics reduce lifecycle costs.

These vendors range from global measurement specialists to regional suppliers. They often compete on application specificity, price, or service proximity and can be preferred partners for bespoke or regional projects.

Recent notable activity includes ABB’s late-2024 preview of a high-performance P-Series pressure transmitter portfolio — an explicit signal that leading vendors are continuing to invest in sensor accuracy, robustness, and digital communication features. Expect product refresh cycles and targeted launches to accelerate as standards and field Ethernet adoption rise.

Note: To preserve competitive sensitivity and to drive you straight to practical insights, the report summarizes detailed regional and application revenue splits, price curve trajectories, and product-segment level forecasts within subscriber-only exhibits.

Executives should treat this report as a playbook: use the procurement templates to update supplier contracts now; run a targeted pilot (3–6 months) using the integration playbook to validate device telemetry use cases; and apply the vendor scorecards to reset supplier rationalization decisions ahead of major 2026 CAPEX cycles. For M&A or supplier partnership considerations, the concentration metrics and vendor capability assessments provide immediate, defensible inputs to valuation and integration planning.

Our analysis combines rigorous market-sizing with pragmatic implementation tools. The result is a single source of truth that bridges strategy and execution: forecasts to budget against, playbooks to act on, and vendor intelligence to negotiate from strength. Because the most valuable slices of the dataset — the granular regional, application and product-segment revenue splits — are decision-grade and sensitive, they are presented in full within the report to subscribers and clients.

For procurement teams, engineering leaders, and corporate strategists preparing 2026 plans, the PW Consulting Smart Transmitter Market report converts uncertainty into a prioritized action agenda. Contact PW Consulting to access the full report and the proprietary exhibits that operationalize the insights summarized here.

For detailed analysis of this topic, please visit the official page:Smart Transmitter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com