Revealed: Engineering Outsourcing Services Driving Energy Sector Innovations

Other |

2026-06-30 09:30:16

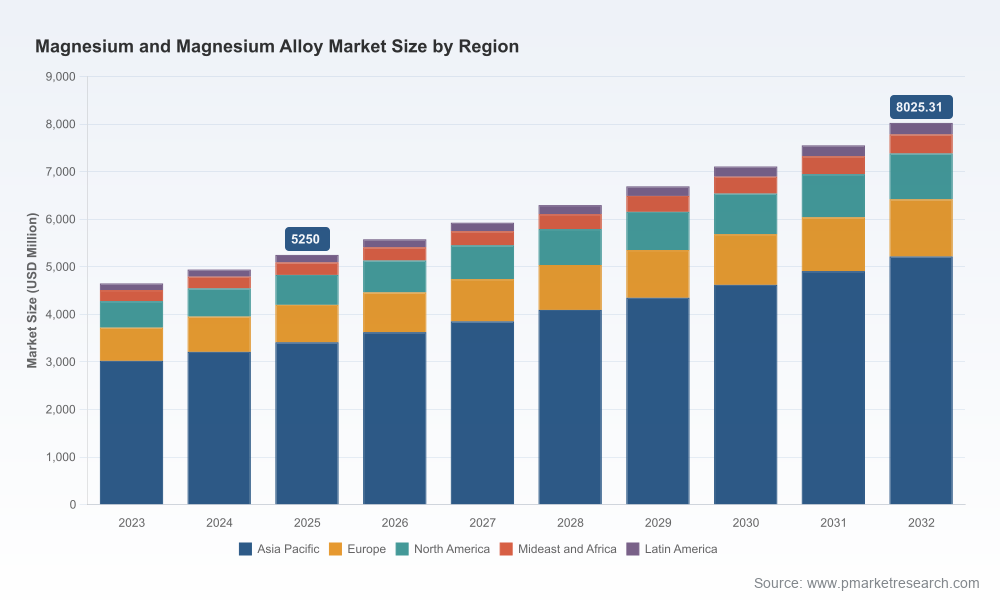

As global manufacturers, materials investors, and national policymakers prepare for a pivotal year, PW Consulting’s latest Magnesium And Magnesium Alloy Market report (base year 2025, forecast 2026–2032) offers a concentrated set of strategic tools and actionable insights to inform decisions across sourcing, product development, and capital allocation. The market is on a steady expansion path — our modeled market size grows from an estimated USD 5,250 million in 2025 to roughly USD 8,025 million by 2032, reflecting a compound annual growth rate (CAGR) of 6.25% over the forecast horizon. This growth is being driven by lightweighting momentum in mobility, selective aero/defense demand, electrification-related component redesign, and incremental gains in die-casting and electronics applications.

Magnesium And Magnesium Alloy Market

Timing: 2026 is the first full planning year after a series of supply-side shocks, tariff changes and financing moves that reshaped producer economics in 2024–2025. Our analysis translates those perturbations into forward-looking scenarios that link short-term operational choices to mid-term market positioning.

Magnesium And Magnesium Alloy Market

Practicality: Beyond market sizing, the study provides operational playbooks — procurement hedges, supplier risk matrices, and modular capex templates — designed for rapid deployment by procurement teams, engineering leads, and corporate development groups.

Magnesium And Magnesium Alloy Market

Strategic clarity: The report distils macro drivers into decision-ready recommendations for three types of stakeholders: (a) OEMs and Tier 1s seeking design-to-cost pathways that balance magnesium’s light-weighting benefits against cost and supply volatility; (b) material producers and recyclers evaluating scaling or technology pivots; and (c) investors and public policy planners assessing onshore capacity initiatives and strategic stockpiling.

Geopolitical supply concentration and policy response: Magnesium’s upstream dynamics remain heavily influenced by a concentrated source base. Recent policy actions — including the addition of magnesium to the USGS Critical Minerals List and the reinstatement of a 25% tariff on certain imports from China in April 2025 — have immediate and medium-term implications for cost, sourcing patterns, and the pace of non-domestic capacity development. These moves contributed to visible spot-price adjustments in late 2025 and sharpened the economics of locality for key end users.

Price evolution and market sensitivity: Import price data through late 2025 indicate materially elevated landed costs in specific markets, while regional pricing trends diverged during the period. Our scenario models quantify how price shifts of the magnitude observed in 2024–2025 can compress OEM margins or re-open substitution discussions (aluminum, high-strength steels, composites) when combined with technological or regulatory changes.

Raw material and process concentration: The Pidgeon thermal-reduction route — dependent on dolomite and other feedstocks — continues to underpin the majority of global primary production in certain regions. This techno-geographic reality informs our supply disruption simulations and feedstock sensitivity matrices.

The market exhibits moderate concentration (our analysis shows top-three and top-five operator concentration metrics that indicate a market with sizable national champions alongside specialized regional players). Competitive dynamics reflect a split between primary magnesium producers, alloy specialists, die-cast component manufacturers, and firms advancing new low-carbon production routes or recycling solutions.

Primary producers and resource-based players: Companies producing magnesium from brine or reduction routes — particularly those with integrated feedstock access — remain pivotal to supply security. Several established producers have adjusted operations or sought upstream infrastructure to mitigate environmental and feedstock risks.

Alloy and component specialists: High-pressure die-casting specialists and alloy developers are advancing to capture design-in opportunities in automotive powertrain and structural components. Their value lies in application know-how, tooling ecosystems, and the ability to convert alloy performance into system-level benefits.

New entrants and technology projects: A wave of financing and joint-venture activity aims to create non-traditional or lower-carbon primary magnesium supply chains. Recent examples include project-level financing commitments and memorandum agreements targeting domestic electrolytic or alternative feedstock production, signaling opportunities for strategic investors and offtake partners.

US Magnesium LLC — a primary brine-based producer with a long-standing role supplying high-purity metal for aerospace and defense; recent operational filings underscore the importance of infrastructure resilience in brine intake and water-level risks to production continuity.

Norsk Hydro ASA — positioning magnesium and alloy recycling as part of a broader sustainability and lightweight-materials offer to transportation OEMs.

Meridian Lightweight Technologies — representing the die-casting and component expertise needed to convert alloy advances into manufacturable automotive systems.

Latrobe Magnesium and other project developers — securing large-scale project finance indications and partnerships to bring alternative feedstock routes (e.g., fly ash conversion) to commercial scale, highlighting how non-traditional raw material pathways can alter future supply maps.

Specialized alloy producers and engineering suppliers — multiple firms across Europe, North America, Asia Pacific, and Australia are pursuing niche high-performance alloys tailored to aerospace and defense applications.

Robust market sizing and trajectory models: A transparent top-down and bottom-up framework calibrated to 2020–2025 historicals (base year 2025) and generating a detailed forecast to 2032. Readers will find scenario-ready outputs that map to procurement and capital planning cycles.

Supply risk and concentration analytics: Stress-testing tools that quantify the impact of supplier outages, tariff shocks, and feedstock price spikes on total landed costs and component-level economics.

Practical procurement playbooks: Tender templates, contract clause recommendations (force majeure, change-in-law, price pass-throughs), and supplier diversification scoring models to shorten decision cycles.

Technology and capex decision frameworks: Comparative techno-economic assessments of primary production routes, recycling-expansion economics, and a modular capex-return model to support greenfield or retrofit investment decisions.

Commercial opportunity maps: Application-focused pathways for automotive, aerospace, electronics, die-casting, and adjacent markets — including design-to-cost levers and substitution risk matrices.

M&A and partnership playbooks: Due-diligence checklists, valuation sensitivities, and integration-risk templates for acquirers and investors looking to consolidate scale or verticalize supply.

Prioritize flexible sourcing: Build two-tiered supplier strategies combining long-term trusted suppliers with agile spot-market routes and contractual optionality. Where strategic, secure capacity via joint ventures or offtake-linked financing to de-risk critical components.

Integrate feedstock and processing risk into product-systems design: Engineering teams should be supplied with costed material substitution scenarios and lifecycle tradeoffs to make faster go/no-go decisions when commodity-driven cost shocks occur.

Accelerate recycling and circularity pilots: Given the economics and policy tailwinds favoring secondary material pathways, pilot scalable recycling loops for production scrap and end-of-life returns that can provide a hedge against primary-price volatility.

Embed tariffs and regulatory scenarios into planning: The return of tariff measures and critical-mineral designations means procurement and tax teams must stress-test supply options for sudden policy shifts and compliance costs.

Target selective M&A for capability and geographic diversification: Consolidation opportunities exist where buyers can add processing, alloy development, or downstream component integration to their footprint, thereby capturing more of the value chain.

Our methodology combines granular primary research with scenario-based financial modeling and a practitioner lens designed for implementable outcomes. The deliverables are intentionally structured to be operational: templates for procurement and contracting, technology selection matrices, capex return playbooks, and an M&A pipeline prioritization algorithm. We surface decision levers — not just forecasts — so executives can translate a projected market growth trajectory into executable roadmaps for sourcing, manufacturing footprint, and capital deployment.

Procurement and supply chain leads: Use the supplier risk matrix and the contract clause library in Q1 2026 to update master supply agreements and hedge strategies.

R&D and product teams: Leverage the substitution and lifecycle models to prioritize design changes that yield the largest system-level cost and weight benefits under simulated price scenarios.

Corporate development and investors: Apply our M&A playbook and valuation sensitivities to triage targets and structure deals that reflect supply risk premiums and regulatory overlays.

PW Consulting’s Magnesium And Magnesium Alloy Market report equips leaders with the intelligence to make informed, timely, and resilient decisions in 2026. The market’s trajectory — from an estimated USD 5,250 million in 2025 to roughly USD 8,025 million by 2032 at a 6.25% CAGR — presents distinct opportunities and measurable risks; our report converts those into operational roadmaps. For access to the full dataset, segmentation analytics, and downloadable tools cited in this brief, consult the full report on the PW Consulting platform.

For detailed analysis of this topic, please visit the official page:Magnesium And Magnesium Alloy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com