Ethyl Phenyl Acetate Market: Strategic Imperatives for 2026 — PW Consulting Insights

PW Consulting today publishes an executive preview of its latest market study on Ethyl Phenyl Acetate (EPA), designed to inform board-level and commercial decisions throughout 2026. Built on a 2020–2025 historical base and a 2026–2032 forecasting horizon, the study delivers a fact‑based roadmap for product strategy, supply‑chain design, regulatory compliance and M&A prioritization in an ingredient market that is growing steadily at an expected compound annual growth rate (CAGR) of 4.95%.

Ethyl Phenyl Acetate Market

Snapshot: Why EPA merits focused strategic attention in 2026

Ethyl Phenyl Acetate occupies a niche but strategically important position across fragrances, flavors, cosmetics and pharmaceutical intermediates. PW Consulting’s market sizing shows a clear expansion trajectory: the global market rose from approximately USD 42.15 million in 2020 to around USD 54.5 million in 2025, and our baseline forecast anticipates continued expansion through the 2026–2032 period, approaching the upper range of our modeled scenarios by 2032. This growth is steady rather than explosive — presenting different strategic choices than hyper-growth commodities: optimization, resilience and targeted differentiation deliver disproportionate shareholder value.

Ethyl Phenyl Acetate Market

What the report contains — operationally useful and decision‑ready

- Robust market-sizing and scenario forecasts (2026–2032) under alternative demand and feedstock-price assumptions, with transparent modeling so corporate planners can run their own sensitivity analyses.

- Supply‑side diagnostics: a bottom-up view of cost structures, capital intensity and plant economics for greenfield, brownfield and toll‑manufacturing options.

- Feedstock exposure analysis that quantifies operating‑cost sensitivity to phenylacetic acid and alcohol pricing, plus pragmatic hedging and procurement playbooks.

- Regulatory and compliance compendium mapping precursor controls, cross‑border shipping obligations, customer‑screening requirements and audit checklists for high‑risk jurisdictions.

- Commercial go‑to‑market guidance for producers and distributors, including product positioning (synthetic vs. natural variants), pricing strategy and channel segmentation principles.

- Competitor and capability benchmarking with partnership, JV and M&A screening frameworks tuned to acquisition economics in this mid‑concentration market.

- Operational risk register and mitigation plans for 2026, focused on supply‑chain disruption, feedstock availability, and enforcement‑driven compliance costs.

Key market dynamics that will shape 2026 decisions

Three dynamics deserve special emphasis for executives planning budgets, capital projects or commercial expansion in 2026:

Ethyl Phenyl Acetate Market

- Feedstock economics and OPEX exposure. Production of EPA is feedstock‑intensive: a majority share of operating expenses is typically attributable to raw materials. Companies that proactively manage feedstock sourcing, integrate upstream where feasible, or secure long‑dated supply agreements will hold a material cost advantage.

- Regulatory and compliance burden. Phenylacetic acid — a primary precursor for EPA — has been subject to elevated controls in several jurisdictions due to diversion risk. These controls increase onboarding friction for new buyers, add record‑keeping costs and can influence the choice of logistics and custody partners. Compliance‑aware suppliers and buyers will outcompete peers on reliability.

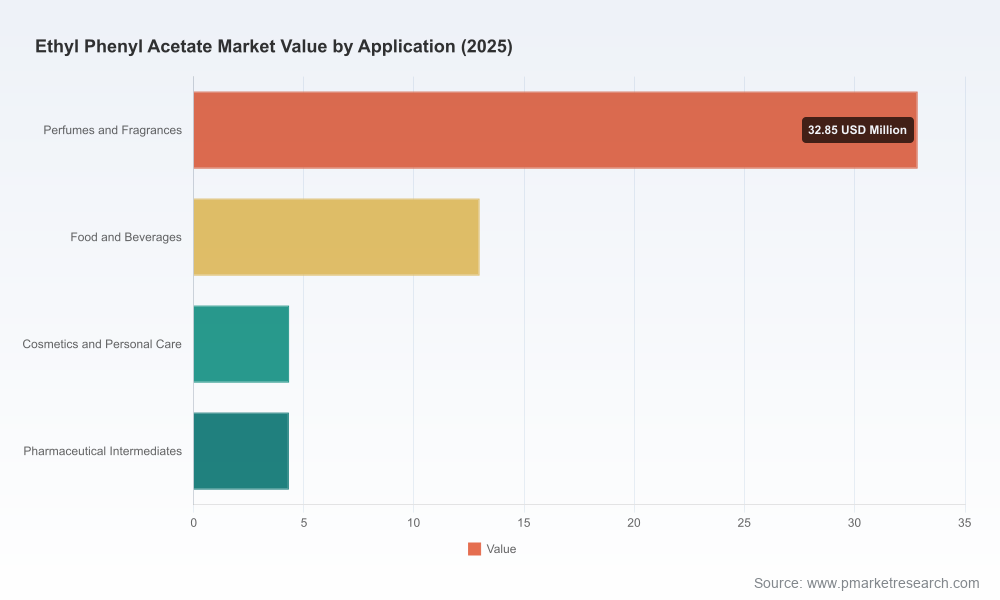

- Commercial differentiation through product grade and provenance. Demand drivers vary across fragrance, flavor and specialty applications. Premium grades (including natural or Kosher-certified variants) command strategic value in developed‑market channels, while industrial grades and bulk supply remain the backbone for formulation houses. Balancing product mix is a key commercial decision in 2026.

Competitive landscape — mapping opportunities and risks

The EPA market is moderately concentrated: the top three global players account for a sizeable share of supply while the top five expand that concentration further. This structure creates both competitive pressure and M&A opportunity: scale matters for regulatory compliance and global logistics, but niche specialists capture margin through grade, purity and certification.

PW Consulting’s vendor review in the report highlights a cross‑section of global players covering different strategic positions:

- Global aroma and flavor houses that integrate EPA into broader product portfolios and offer strong customer access in developed markets.

- Specialty chemical manufacturers and catalog suppliers that emphasize high‑purity, research‑grade and application‑specific variants for cosmetics, pharma intermediates and R&D channels.

- Regional manufacturers and distributors — particularly in Asia and India — that provide cost‑competitive supply for industrial applications and local formulation industries.

- Natural and Kosher‑oriented suppliers that have positioned EPA variants for premium flavor and fragrance segments.

For procurement and strategy teams preparing 2026 plans, the report benchmarks each archetype across capability dimensions: regulatory compliance posture, quality/certification portfolio, logistic reach, product breadth (synthetic vs natural), and commercial flexibility (minimum order quantities, tolling and contract manufacturing). The public company and private supplier profiles included in the study are curated to highlight tradeoffs when selecting partners, without disclosing confidential market share data.

Practical guidance for corporate decision‑makers in 2026

Based on our scenario modeling and supplier mapping, PW Consulting recommends that executives prioritize the following actions during 2026 planning cycles:

- Embed feedstock stress‑tests into every capital and commercial plan. Model at least two adverse feedstock‑price scenarios and quantify the margin and breakeven impacts on new capacity, contract pricing and tolling economics.

- Build compliance capabilities as a competitive moat. Investing in compliance systems, traceability and pre‑qualified logistics partners reduces onboarding time for high‑quality customers and lowers transaction costs associated with regulated precursors.

- Consider upstream partnerships or partial integration where scale justifies it. For mid‑sized players, tolling agreements or joint procurement consortia can deliver similar cost stability with less capex.

- Differentiate product portfolios through targeted certification. Natural, Kosher and high‑purity grades can unlock premium buyers; invest in small‑scale production lines that allow flexible grade switching rather than single‑purpose assets.

- Pursue bolt‑on M&A in capability pockets: smaller specialty producers with robust quality systems, niche natural‑ingredient specialists, or regional distributors with strong route‑to‑market are higher‑probability targets than large, diversified chemical acquisitions.

- Implement dynamic commercial contracts. Use pricing mechanisms that share feedstock risk with buyers where possible, combined with option structures for volume flexibility and minimum‑commitment buyouts.

Supply‑chain resilience: tactical recommendations

Given the combined pressure of feedstock cost volatility and regulatory controls, three tactical moves can materially reduce execution risk in 2026:

- Secure multi‑tiered sources for phenylacetic acid and qualifying co‑suppliers to avoid single‑point failure; include alternative esterification routes in technical due diligence to reduce supplier lock‑in.

- Pre‑qualify a set of logistics partners with documented permissions for handling controlled precursors and with audit histories in regulated shipments.

- Adopt inventory strategies that balance working capital with the cost of potential supply interruption — for many buyers, a hybrid rolling buffer linked to key demand seasons is optimal.

Why this report matters now

2026 will be a year of execution for companies that have spent 2024–2025 planning supply‑chain robustness and product differentiation. The EPA market’s steady growth — supported by end‑market expansion in flavor, fragrance and specialty applications — rewards tactical precision rather than headline investments. Our analysis shows that firms that optimize feedstock exposure, harden compliance processes and selectively invest in premium grades will achieve better margin resilience and faster commercial traction.

PW Consulting’s full report is purposely selective in this preview: it demonstrates methodological rigor and offers actionable frameworks while withholding detailed proprietary splits and transaction‑level data to ensure readers access the complete dataset and modeling workbook on our website. For executives evaluating capital projects, supplier contracts or M&A targets in 2026, the full report provides the granular inputs and downloadable scenario models needed to convert strategy into measurable outcomes.

Next steps for executives

- Download the full report and scenario workbooks to stress‑test your 2026 plans against our baseline and alternative scenarios.

- Engage PW Consulting for a tailored supplier due‑diligence package or a capital‑project cost‑of‑production assessment.

- Schedule a 60‑minute briefing with our lead analyst team to review implications for your portfolio and receive a customized action plan.

Contact PW Consulting to access the full Ethyl Phenyl Acetate Market report, the underlying models, and our advisory services designed to translate these insights into executable 2026 strategies.

For detailed analysis of this topic, please visit the official page:Ethyl Phenyl Acetate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com