Rugby Equipment Market 2026: Strategic Briefing from PW Consulting

As global sport ecosystems rebound and participation patterns shift, the rugby equipment market is entering a phase where strategic foresight will determine winners and laggards. PW Consulting’s new market study — anchored on a 2025 base year and projecting through 2032 — quantifies the market trajectory and, more importantly, translates implications into an operational playbook for executives preparing budgets and product roadmaps in 2026.

Rugby Equipment Market

Executive snapshot: the market in macro terms

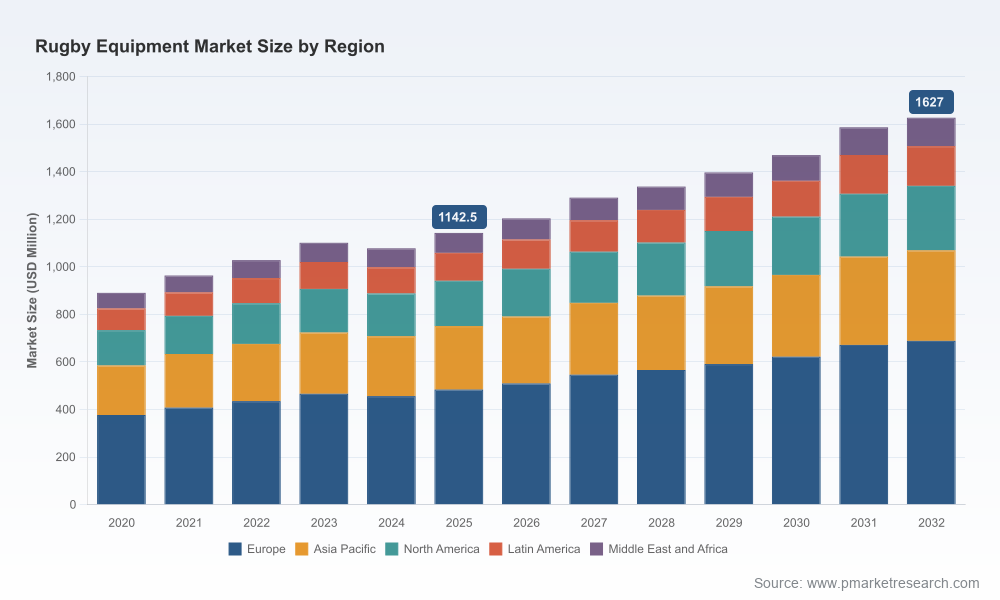

Our model shows the global rugby equipment market expanding from a 2025 baseline of approximately USD 1,142.5 Million to an estimated USD 1,627.0 Million by 2032, implying a compound annual growth rate (CAGR) of about 5.18% over the 2026–2032 forecast window. After a period of mixed year-on-year performance during 2020–2025, driven by event cycles, supply-chain shocks and raw-material volatility, the market enters a sustained growth phase underpinned by rising grassroots participation, commercialization of elite competitions, and accelerated digital retail adoption.

Rugby Equipment Market

Market concentration is moderate: the top three vendors capture under half of total market value, and the top five fall around the mid‑50s percentage range — a structure that supports premium brand strategies but leaves room for niche specialists and private-label entrants to scale.

Rugby Equipment Market

Why this report matters for 2026 decision cycles

- Investment prioritization: The growth path to 2032 makes clear where incremental spend on product development and go-to-market yields the highest expected returns. The macro growth rate indicates a market large enough for competitive investments, yet fragmented enough to reward focused differentiation.

- Risk calibration: Our scenario analysis integrates commodity-price shocks, regulatory tightening and event scheduling to produce stress-tested revenue paths. This directly supports 2026 capital-allocation decisions and contingency planning for manufacturing and inventory.

- Commercial timing: With World Rugby-led competitions continuing to shape demand spikes, the report maps optimal timing for product launches and sponsorship negotiations to maximize visibility and order fill rates for the 2026–2028 window.

- Channel mix optimization: We quantify the growing role of e-commerce against specialty retail and mass channels and show tactics to safely shift margin mix while protecting club and institutional relationships.

What the PW Consulting report delivers (operationally focused)

- Complete market model (2020–2032): annual revenue series, CAGR by horizon, and high‑resolution demand scenarios to support budgeting and investor diligence.

- Actionable go‑to‑market playbooks: product launch calendars aligned to competition cycles, recommended pricing envelopes by product family, and promotional timing to capture youth-season demand peaks.

- Supply‑chain impact matrix: sensitivity analysis showing how 8–12% swings in synthetic-leather and petrochemical feedstocks affect margins across product types, plus mitigation levers (dual-sourcing, SKU rationalization, buffer-stock sizing).

- Regulatory and compliance checklist: a practitioner’s guide to World Rugby Law 4 compliance, EU REACH considerations for imported gear, and documented testing paths to avoid market refusals and costly recalls.

- Competitive intelligence dossier: capability maps, recent product and certification moves by category leaders, and tactical play-by-play for regional market penetration.

- Commercial KPI dashboard: leading indicators for demand (registered player counts, youth-club registrations, event calendar metrics) and a recommended set of margin, fulfillment and digital engagement metrics for 2026 tracking.

Competitive landscape — who matters and why

The market is shaped by a mix of global sports conglomerates, heritage specialists, category innovators and mass-market retailers. Key profiles from our analysis:

- Canterbury of New Zealand (New Zealand) — Longstanding specialist across jerseys, boots and protective gear with deep professional and amateur distribution. Strengths: brand authenticity, team kit partnerships, and product durability credentials.

- Adidas (Germany) — Global scale and official competition partnerships give Adidas high visibility in marquee events. Strengths: supply-chain capacity, co‑branding leverage, and premium performance positioning.

- Under Armour (United States) — Focused on performance apparel and compression technologies, with growing interest in protective equipment that complements a training-first narrative.

- Mitre Sports (United Kingdom) — Specialist ball manufacturer whose match-grade products serve major domestic competitions; experience with post‑recall quality control is a differentiator.

- Gilbert Rugby (United Kingdom) — Category heritage and tournament ball supply position Gilbert as a benchmark supplier for official match balls and skill‑level differentiation.

- Maddox Rugby (United Kingdom) — Nimble innovator in protective wear (headguards, shoulder pads), recently launching compliant new models designed to meet the strict World Rugby impact standards.

- Rhino Rugby (United Kingdom) — Training and club equipment specialist; their focus on durability and institutional sales is aligned to the rising demand from clubs and schools.

- Altin Rugby (United Kingdom) — Custom kits and regional distribution expertise suit federations and clubs seeking localized identity and flexible order sizes.

- World Rugby (Ireland) — As the sport’s governing body, it shapes specifications, compliance rules and certification pathways that materially affect product development cycles.

- Decathlon (France) — Mass-market channel that competes on affordability and distribution breadth, putting pressure on price-sensitive segments and private-label positions.

Recent industry moves highlight how leaders are positioning for 2026:

- Adidas launched official match balls and team kits tied to marquee tournaments, reinforcing event-driven commercial windows.

- Gilbert upgraded ball grip technology with IRB-approved product iterations — an illustration of how incremental engineering can sustain market share in a core product line.

- Maddox introduced a headguard that aligns with current World Rugby Law 4 safety thresholds, signaling the accelerating importance of certified safety innovation.

- Canterbury’s exhibition of a sustainable apparel line underscores the rising strategic premium for durable, lower‑impact materials.

Market dynamics and key operational risks

The market’s near-term trajectory is shaped by four interdependent dynamics:

- Regulatory tightening: World Rugby’s Law 4 mandates and regional chemical restrictions (e.g., REACH in the EU) create compliance costs and gatekeeping friction for imported components. Manufacturers must embed testing and certification into NPI timelines to avoid market delays.

- Raw-material volatility: Synthetic leather inputs (PVC, PU) experienced notable price increases recently. Our supply‑chain stress tests show that unhedged exposure to petrochemical price swings can compress gross margins materially within a single fiscal year.

- Participation and youth demand: Global registered-player growth and youth engagement are primary demand drivers for entry-level equipment and training gear — an area where affordability and distribution strategy determine market share gains.

- Quality and recall risk: Product recalls (documented cases in recent years) emphasize the need for tightened QC protocols across outsourced production and clear liability frameworks with vendors.

Strategic playbook for 2026 — six priority moves

- Embed compliance early: Operationalize Law 4 and chemical compliance into R&D gating criteria. Budget 2026 NPI timelines to include third‑party certification steps; this prevents costly post-launch corrections and market access delays.

- Securitize material supply: Implement multi-sourcing and hedging where feasible for synthetic-leather inputs. Consider nearshoring critical components for flagship lines to reduce lead-time and freight exposure ahead of major competitions.

- Differentiate through verified safety: Convert safety-compliant protective gear into a brand asset — certified impact testing should be central to product marketing for clubs and parents of youth players.

- Pursue hybrid channel models: Protect specialty-retail relationships while investing in direct-to-consumer digital experiences that raise lifetime value. Use data-driven promotions tied to registration cycles to acquire club and youth customers cost-effectively.

- Optimize portfolio for margin capture: Rationalize SKUs with low sell-through in favor of core, high-margin models for elite and training use. Use the report’s SKU-level profitability templates to model SKU pruning with minimal sales disruption.

- Activate sustainability as a demand lever: Prioritize lower-impact materials in team‑kit and apparel lines. Sustainable claims should be verifiable and tied to durability metrics to avoid greenwashing exposure.

Next steps and how to use this intelligence

For executives planning 2026 budgets, this report serves as both a forecasting tool and an operational checklist. Use the market model to stress-test your P&L under commodity and event-driven scenarios. Apply the compliance and supply‑chain playbooks to lock NPI timelines. And align sponsorship and product launches to the event windows highlighted in our timing maps.

To preserve strategic value for decision-makers, we have presented a concentrated slice of findings here. The full report includes granular regional and product segmentation, SKU-level profitability matrices, downloadable model files and a detailed supplier evaluation framework — all designed to be plug-and-play for CFOs, head of product and supply-chain leads.

Accessing the full study

PW Consulting’s Rugby Equipment Market report is available with accompanying datasets and implementation templates. Clients and partners who require tailored scenario runs or a bespoke brief for internal stakeholders can commission an executive workshop with our analysts to translate findings into a 90‑day action plan.

For teams preparing to act in 2026, this is the moment to move from intention to structure: lock compliance into R&D, harden supply channels, and design channel strategies that capture rising youth and institutional demand. The macro growth trajectory is clear — the differentiator will be companies that convert regulatory and supply-chain challenges into competitive advantage.

For detailed analysis of this topic, please visit the official page:Rugby Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com