Mining Gas Alarm Market: Strategic Imperatives for 2026 — A PW Consulting Industry Brief

Executive Summary

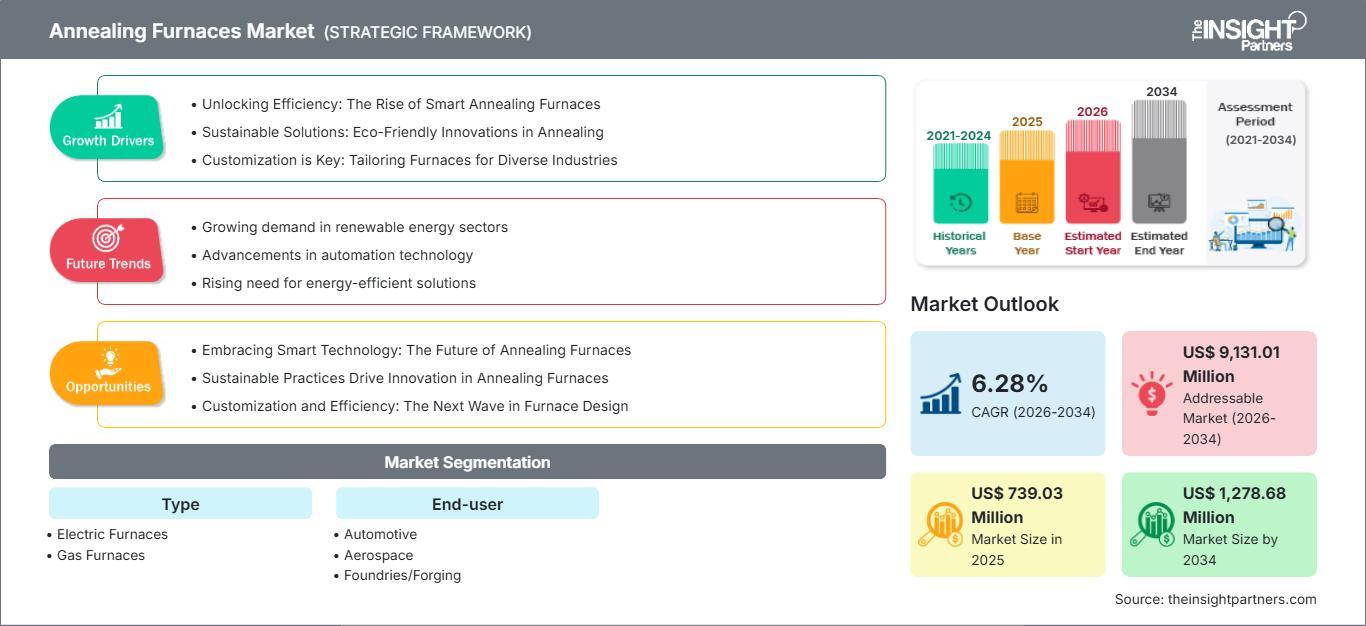

PW Consulting’s latest Market Research Report on the Mining Gas Alarm market (base year 2025; forecast 2026–2032) crystallizes what operational leaders, procurement heads, and safety strategists must know as they plan capital and operational decisions for 2026. The market has expanded steadily from the start of the decade and reached a mid‑year 2025 valuation that confirms an ongoing recovery and upgrade cycle across underground and surface mining operations. Our model projects continued expansion through 2032 at a compound annual growth rate (CAGR) of 5.85%, driven by regulatory pressure, digitalization of safety systems, and supply‑chain dynamics affecting sensor inputs.

Mining Gas Alarm Market

Why this report matters for 2026 decision-making

- Actionable forecasting: Our centralized scenario engine maps adoption curves for both portable and fixed gas detection solutions across multiple mine archetypes. The forecast horizon (2026–2032) is tuned to typical procurement and fleet-refresh cycles, allowing procurement teams to align multi‑year capital plans with risk mitigation thresholds and expected equipment lifecycles.

- Regulatory-first playbook: With evolving enforcement and certification expectations—such as MSHA requirements for methane monitoring on mobile mining equipment and ATEX/IECEx mandates for explosive atmospheres—the report turns regulatory texts into procurement triggers and compliance roadmaps.

- Supply-chain sensitivity: The report quantifies the downstream sensitivity of detector BOM cost to raw material price pressure (notably precious metals used in electrochemical sensors) and translates commodity price scenarios into supplier risk scores and stockpiling recommendations.

Market trajectory in context

From 2020 through 2025 the market recorded consistent year‑on‑year expansion as mines accelerated modernization and compliance upgrades. Our top‑line time series shows a steady rise through 2025, and the forecast to 2032 implies not just recovery but an inflection toward integrated, connected safety architectures. The projected CAGR of 5.85% across the 2026–2032 forecast window reflects a mix of retrofit demand, new mine developments in select geographies, and a growing replacement cycle as legacy non‑certified units are phased out.

Mining Gas Alarm Market

Core dynamics shaping 2026 choices

- Regulatory enforcement converts into capex: Mandatory thresholds such as methane alarm setpoints required on mining equipment are driving equipment OEMs and mine operators to prioritize certified detection systems during scheduled capital refreshes.

- Digital convergence and wireless connectivity: Increasing appetite for near‑real‑time worker monitoring and remote telemetry (including LTE/LPWAN options) is elevating the value proposition of connected wearables and networked fixed systems, changing procurement evaluation from pure sensor accuracy to data‑integration capability.

- Materials and component risk: Electrochemical sensor production depends on platinum group metals; spot price volatility for these inputs materially alters unit economics for detectors and affects lead times for replacements and calibration spares.

- Human factors and ILO guidance: The ILO’s emphasis on early‑warning, real‑time detection to cut underground fatalities is prompting organizations to expand beyond compliance to performance targets tied to safety KPIs.

Competitive landscape — what to expect in vendor selection

The market exhibits moderate concentration: the leading three vendors account for a substantive share of revenue, with the top five firms controlling a majority portion of market value. This mix produces a supplier ecosystem where established brands remain critical for certified, mine‑grade solutions, while niche players and connectivity specialists push the envelope on integration and data services.

Mining Gas Alarm Market

Our vendor scan deep dives into product and go‑to‑market strategies of the established manufacturers and innovators who dominate the procurement shortlists. Companies covered include (selection):

- MSA Safety — focus: certified multi‑gas wearables and connected telemetry showcased at recent industry expos.

- Dräger — focus: ATEX/IECEx certified portable analyzers and upgrades aimed at mining environments.

- Honeywell — focus: single and multi‑gas monitors with remote monitoring add‑ons for remote operations.

- Industrial Scientific (Fortive) — focus: wireless‑capable detectors with mining‑specific configurations.

- RKI Instruments, GfG Instrumentation, Trolex, Blackline Safety — focus: a mix of intrinsically safe hardware, fixed monitoring systems, and LTE‑enabled wearable devices.

Recent vendor signals—product upgrades at major trade shows and targeted product releases—confirm two strategic themes: (1) incumbents are investing in connected device platforms and mining‑graded certification, and (2) competition is increasingly about the software and services wrapped around sensors (fleet management, proof‑of‑calibration workflows, event analytics), not only sensor accuracy.

What the PW Consulting report contains (practical, procurement-ready content)

- Quantitative market sizing and scenario forecasts (2020–2032), including base‑case, downside, and upside demand scenarios mapped to commodity prices, regulatory tightening, and macro capital cycles.

- Vendor scorecards and procurement decision trees that translate certification, connectivity, service footprint, and TCO into prioritized vendor shortlists for three mine archetypes.

- Deployment playbook: stepwise timelines for pilot → scale → sustain, with resource estimates for field calibration, spare parts, and training interventions.

- Regulatory compliance matrix: succinct mapping of US, EU, and international certification requirements into audit‑ready procurement specifications and acceptance tests.

- Supply‑chain stress tests and mitigation levers: sourcing diversification, strategic stocking policies for critical sensor spares, and supplier contract clauses to manage lead‑time risk.

- ROI and TCO models calibrated to real‑world duty cycles and sensor replacement cadences — presented as configurable worksheets so executives can plug in site‑specific parameters.

- Use case blueprints for common mine operations (underground longwall, open‑pit haulage, ventilation control), including integrations with mine ventilation models and emergency response playbooks.

Risk framework and scenarios that matter for 2026

Our risk matrix prioritizes the variables that will most influence procurement outcomes in 2026:

- Commodity‑price shock to sensor inputs (e.g., platinum group metals) — impacts unit economics and replenishment costs.

- Regulatory shocks — accelerated enforcement cycles or expanded certification requirements raise compliance urgency and shorten procurement lead times.

- Connectivity and cyber‑resilience risks — adoption of LTE/IoT introduces new operational dependencies and cyber risk vectors that need to be priced into vendor SLAs.

- Supplier consolidation vs. new entrants — concentration dynamics can affect bargaining power and service levels in five‑to‑seven year lifecycle planning.

How senior leaders should use this report in 2026 planning

- Align safety and capital plans: Use the report’s scenario maps to translate regulatory and commodity trends into capex phasing, so that compliance upgrades align with fleet refresh windows and minimize stranded asset risk.

- Create an RFP template based on certification and data integration requirements: Our procurement checklist accelerates RFP drafting and ensures bids are comparable across hardware, software, and services.

- Implement a supplier‑risk dashboard: Operationalize the supply‑chain stress tests into quarterly supplier health reviews and initiate strategic supplier partnerships for calibration services and spares.

- Prioritize pilots for connectivity-first solutions: Run time‑boxed pilots that validate LTE/wireless telemetry, data ingestion to safety command centers, and alarm management workflows before enterprise roll‑out.

What we are deliberately not disclosing here — and why

This brief follows a “trailer” approach: we surface the report’s unique value and executive implications but withhold the granular segmentation tables, region/application revenue splits, and the full vendor financials in order to protect the analytical IP and drive direct access to the full report. The complete dataset includes detailed regional and application breakouts, product‑level forecasts, and downloadable TCO calculators that are essential for procurement negotiations and financial modelling.

Conclusion — immediate next steps for 2026

For 2026, the optimal playbook balances compliance urgency with strategic modernization. Organizations should convert regulatory obligations into phased investments that upgrade both hardware and digital infrastructure; secure supply‑chain resilience for sensor criticals; and select vendors on combined criteria of certification, service coverage, and data‑platform interoperability. PW Consulting’s Mining Gas Alarm Market report provides the operational blueprints, vendor scorecards, and financial tools to execute that strategy with confidence.

Access the full intelligence

To obtain the complete market model, vendor scorecards, procurement templates, and scenario workbooks designed for executive use in 2026, please visit the PW Consulting report page (full report access details and licensing options are available there).

For detailed analysis of this topic, please visit the official page:Mining Gas Alarm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com