Enzalutamide API Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

Executive summary

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I present a high-level preview of our forthcoming Enzalutamide API Market report (base year 2025). The market is on a pronounced growth trajectory driven by generic launches, shifting reimbursement landscapes, and supply-chain realignments. Our model shows the total market scaling materially between 2025 and the early 2030s at a compound annual growth rate (CAGR) of 8.01%, reflecting a structural uplift in API demand as encephalitic patent cliffs and policy changes accelerate generic adoption. This preview outlines the strategic value the full report delivers to executives preparing decisions in 2026 — while preserving the granular, proprietary splits and price forecasts that we reserve for the full report access.

Enzalutamide Api Market

Why this matters for 2026 decision-makers

- Timing: A key composition patent reaches expiry in February 2027. The 12–24 months surrounding that date represent a concentrated window for contract negotiation, capacity build-out, and competitive positioning.

- Volume inflection: Our base-year analysis captures a clear knee in demand starting 2026, tied to generics entering payer formularies and expanded Medicare coverage. Buyers and manufacturers must sequence investments and contracts now to capture scale economics.

- Concentration and commercial dynamics: The market concentration profile indicates a moderate-to-high level of supplier concentration among the leading firms, producing a landscape where strategic partnerships and DMF portfolios matter more than ever.

Market trajectory — macro view (what we disclose here)

PW Consulting’s topline model, calibrated against 2020–2025 historicals and our proprietary demand-supply simulations, estimates meaningful expansion in absolute market size through the forecast horizon 2026–2032. This growth is underpinned by three structural drivers: (1) accelerated generic substitution post-patent expiry and broader formulary access, (2) consolidation of manufacturing capacity into cGMP-certified sites with export capabilities, and (3) ongoing price pressure mitigated by volume-led economies of scale. Our compound growth assumption for the forecast period is 8.01% — a realistic baseline for planning capacity, working capital, and M&A timing in 2026.

Enzalutamide Api Market

Key dynamics shaping the market

- Regulatory and IP timing: The impending patent expiry in early 2027 is the single-largest catalyst for market change. The period immediately before and after this date will see heightened regulatory filings, DMF activity, and tactical launches by established API suppliers and generics manufacturers.

- Regulatory hygiene and quality risk: Over a dozen drug master files are already on record with regulators, concentrated in a small number of producing countries. This depth of filings lowers some regulatory entry barriers, but also elevates the importance of quality continuity and impurity controls (notably nitrosamine risk vectors) as a differentiator.

- Raw-material exposure: Key intermediates drive a disproportionate share of production cost volatility. Procurement teams must understand that certain intermediates account for a large single-component share of manufacturing cost and therefore represent primary levers for cost control or, conversely, supply disruption.

- Payer and reimbursement shifts: Generics eligibility under major public programs has already begun to materialize. This will stimulate volume but compress per-unit pricing, shifting the competitive battleground from list price to service, reliability, and supply guarantees.

Competitive landscape — what leading suppliers signal

The supplier ecosystem is anchored by several established API producers and CDMOs with cGMP footprints and regulatory dossiers in major regulated markets. Recent public developments underscore a strategic pattern:

Enzalutamide Api Market

- MSN Laboratories advanced commercial readiness with regulatory approval for a finished-dosage product in mid-2024, signaling integrated supply capability and an ability to support scale-formulation partners.

- Hetero executed a rapid U.S. market entry with a generic launch in early 2024 supported by in-house API manufacturing—illustrating the vertical-integration route to market share capture.

- Aurobindo’s tentative approvals and other filings reveal a continuation of capacity build-out to supply global generics.

Other incumbent suppliers and CDMOs maintain strategic roles as scale manufacturers and contingency providers. Our competitive scoring matrix in the full report benchmarks these players across regulatory footprint, DMF coverage, capacity elasticity, impurity-control systems, and commercial reach — the precise weightings and scores are intentionally reserved for subscribers.

What the PW Consulting report contains (practical deliverables)

We designed the full report to be directly actionable for procurement, manufacturing, regulatory, and corporate development teams. Highlights include:

- Bottom-up market model with scenario variants (baseline, accelerated generic adoption, supply shock) — inclusive of sensitivity to raw-material shocks and regulatory delays.

- Supply map and capacity audit that identifies not just who can supply today but who can scale reliably through 2028 under different demand scenarios.

- Regulatory tracker and DMF inventory, mapping filing status, inspection histories, and potential regulatory risk flags — enabling an early-warning system for sourcing teams.

- Commercial playbook for contract design: recommended clauses, service-level commitments, and hedging constructs to align price with volume and quality risk.

- Deal-screen and partnering thesis for M&A or tolling arrangements, including preliminary valuation multiples and transaction structures suited to the API space.

- Operational resilience checklist: recommended CAPEX timelines, dual-sourcing templates, and contingency stock strategies to mitigate impurity or raw-material disruptions.

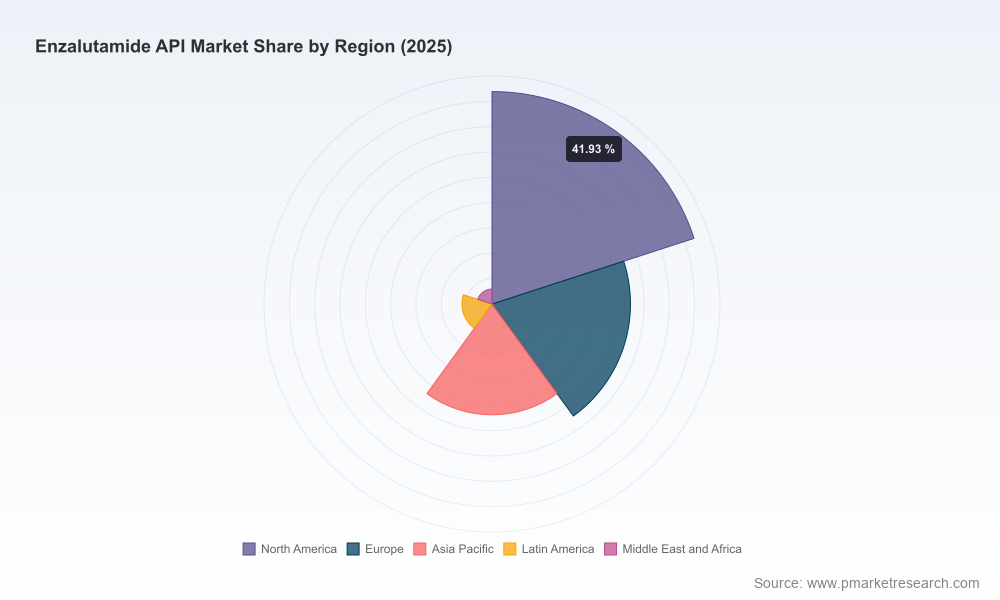

We deliberately omit granular regional and application revenue splits from this preview to preserve the strategic value of the subscription product; those granular matrices are a core asset of the full report.

Risk matrix and blind spots

- Quality incidents and impurity findings (e.g., nitrosamine-related import alerts) can rapidly constrict available supply; contingency capacity is limited and costly to activate at short notice.

- Raw-material price cyclicality means that without procurement hedges or vertical integration, margin compression will accelerate as generics scale.

- Regulatory bottlenecks — not market demand — are the most common cause of delayed launches. Firms with robust DMF portfolios and clean inspection histories hold outsized advantage.

Practical strategic imperatives for 2026

For executives preparing budgets and deals in 2026, our advisory suggests the following prioritization:

- Secure optionality now. Execute staged capacity reservations and opt-out clauses tied to regulatory milestones to balance flexibility with market-capture potential.

- Prioritize validated quality footprints. Shortlist suppliers not merely by price but by recent inspection outcomes, impurity-control capabilities, and DMF completeness.

- Design procurement contracts for asymmetric risk sharing. Sliding-scale pricing tied to volume bands, conditional CAPEX commitments, and inventory buy-down mechanisms reduce downside for both parties.

- Consider strategic partnerships or tolling arrangements rather than outright capacity expansion if time-to-market is constrained — CDMOs with inspected facilities can be deployed faster than greenfield projects.

- Model scenarios where raw-material cost pressure is persistent; lockable offtake on key intermediates or backward integration can be value-accretive in multi-year view.

How PW Consulting’s work adds value compared with public intelligence

Public filings and press releases show activity; our differentiated value is the synthesis: cross-mapping regulatory status to physical capacity and payor-driven demand curves, then converting that into executable procurement and M&A roadmaps. The preview you are reading establishes the strategic themes; the full report contains the proprietary matrices, ranked supplier scorecards, and contract templates that translate strategic intent into executable programs.

Next steps and access

We have intentionally positioned this document as a “trailer”: enough insight to shape boardroom debate and procurement prioritization, but not the full tactical dataset. Subscribers to the full PW Consulting Enzalutamide API Market report will receive the complete model, supplier scorecards, the regulatory DMF log, and a downloadable commercial-playbook template designed for immediate deployment in 2026 procurement cycles.

For executives considering manufacturing investments, sourcing switches, or M&A in the Enzalutamide value chain, the coming 18 months are decisive. PW Consulting’s report is built to convert uncertainty into calibrated action. Visit our report page to request the full dataset, licensing options, and an executive briefing tailored to your organization’s exposure.

For detailed analysis of this topic, please visit the official page:Enzalutamide Api Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com