PW Consulting: Edta Solution Market — Strategic Preview for 2026 Decision-Making

Executive summary

The global EDTA (ethylene-diamine-tetraacetic acid) solution market has emerged from a period of steady recovery and structural transformation. Our new market model shows the industry expanding from USD 688.12 Million in 2020 to USD 845.5 Million in the base year (2025), and set to continue along an upward trajectory with a projected market value exceeding USD 900 Million in 2026 under a 2026–2032 CAGR of 4.38%. For executives, procurement leaders, R&D heads and corporate strategy teams preparing plans for 2026, this landscape presents both near-term operational risks and multi-year strategic opportunities.

Edta Solution Market

Why this report matters for 2026 corporate decisions

- Tactical buying and cost control: Raw material price shocks — notably the rise in formaldehyde costs — and trade policy shifts have condensed the window for effective procurement cycles. Our analysis translates price-volatility scenarios into procurement playbooks that are executable within 60–180 day planning horizons.

- Regulatory and formulation risk: New regulatory constraints and labeling regimes are already changing allowable EDTA formulations in key markets. The report maps regulatory levers to product portfolios and identifies low-friction reformulation pathways to defend revenue in regulated segments.

- Product and go-to-market strategy: The introduction of biodegradable chelating alternatives and certifications for potable water use are altering segmentation economics. We provide scenario-based revenue impacts and GTM tactics tailored for suppliers, brand owners, and private-label manufacturers.

- Capital deployment and M&A prioritization: With selective capacity expansions announced and market consolidation underway, the report gives an evidence-based framework for prioritizing brownfield expansion, capacity sharing agreements, and target screening for inorganic growth.

What is in the report — practical, executable content

This is not a high-level primer. The report is a hands-on toolkit designed for teams that must make 2026 commitments. Key deliverables include:

Edta Solution Market

- Bottom-up market-sizing and trend model (historical 2020–2025, forecast 2026–2032) with downloadable assumptions and sensitivity toggles in Excel.

- Short-, medium-, and long-term price scenarios driven by feedstock indices and trade-policy shock simulations; actionable hedging and contract-structure recommendations for procurement.

- Regulatory impact matrices mapping current and pending restrictions (e.g., concentration limits and labeling regimes) to formulations and sales channels, plus compliance roadmaps by product group.

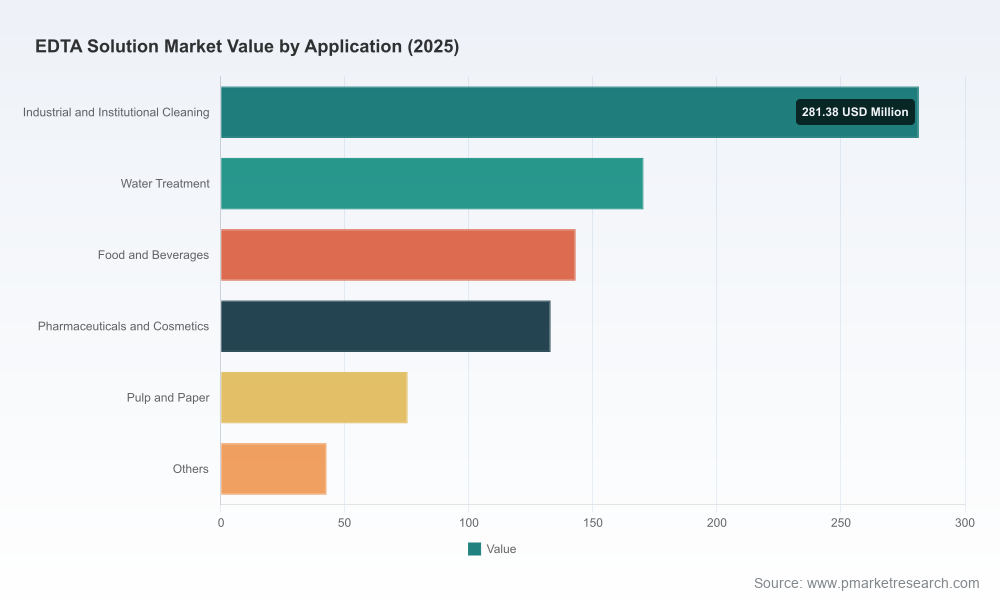

- Segment-level demand drivers and unit-economics playbooks for industrial cleaning, water treatment, food & beverage, pharma & cosmetics, pulp & paper and adjacent uses — with specific guidance on reformulation, margin protection and premiumization strategies.

- Supplier profiling and risk heatmaps covering operational capacity, certification footprints, product portfolios and strategic intent — designed to support sourcing decisions, preferred-vendor programs and dual-sourcing plans.

- Investment decision templates for capacity expansion, joint ventures and M&A, including payback-period simulations and integration checklists tailored to EDTA value chains.

Market dynamics you need on your radar in 2026

Several structural and cyclical forces are converging this year, and the winning playbooks will be those that translate these dynamics into operational countermeasures.

Edta Solution Market

- Feedstock inflation and input risk: Formaldehyde price increases have materially raised production costs for EDTA solutions. The report quantifies margin erosion under realistic pass-through assumptions and provides short-list mitigation tactics such as alternative feedstocks, blended procurement, and tolling arrangements.

- Regulatory tightening: Restrictions implemented in major regulatory jurisdictions — including concentration limits and labeling requirements — are compressing formulations available for certain consumer-end applications. We outline compliance-first product roadmaps and labeling strategies to preserve shelf presence while minimizing reformulation costs.

- Trade and supply-chain shocks: Anti-dumping duties and higher trade friction are reconfiguring where companies source intermediate EDTA solutions. We analyze the competitive consequences and provide a sourcing decision matrix balancing landed cost, reliability and regulatory exposure.

- Green substitution and certification: The market is responding to sustainability and biodegradability demands: vendors introducing alternative chelants and winning certifications for potable-water use are reshaping buyer requirements in sensitive end-markets. The report maps substitution cascades and identifies which customer segments are most susceptible to switching.

Competitive landscape — profiles and implications

The EDTA solutions market is characterized by a mixture of global chemical majors, specialty suppliers, and laboratory distributors. Leading suppliers combine brand equity, technical support, and regulatory capabilities — attributes that matter more than ever when regulatory or certification barriers rise. Our competitive study includes deep profiles of incumbent players, including product portfolios, strategic moves and near-term capacity dynamics.

- Dow Inc. (Midland, MI, USA): Established supplier of Versene EDTA solutions with strong commercial positions in industrial water treatment and detergents. Recent certification wins have opened potable-water applications, strengthening credential sets for utility and municipal buyers.

- BASF SE (Ludwigshafen, Germany): Leverages a global footprint and brand presence in personal care and pulp & paper. Capacity expansions announced in proximity to detergent demand indicate a high-conviction bet on volumes in legacy segments.

- Nouryon (Amsterdam, Netherlands): Focused on specialty formulations and recently launched a biodegradable chelate aimed at personal care, signaling strategy alignment with sustainability-driven customers and regulatory-safe formulations.

- Jungbunzlauer (Wagen, Austria): Niche strength in food-grade and nutritional applications with tailored liquid EDTA systems and regulatory know-how around food additive standards.

- Sigma-Aldrich (Merck KGaA) and VWR (Avantor): Important channels for high-purity and ready-to-use EDTA buffers serving labs, diagnostics and biotech — segments where traceability and quality far outweigh commodity pricing.

- Mitsubishi Gas Chemical and Huntsman Corporation: Specialized offerings in electronics cleaning and water-treatment scale inhibition, respectively, that underscore how application-specific value propositions maintain margin insulation.

Our analysis shows a market where top-tier players maintain scale and regulatory competency advantages, while agile specialists capture premium niches. For 2026, competitive advantage will hinge on certification footprints, sustainable product alternatives, and the ability to navigate trade barriers.

Five strategic imperatives for 2026

- Rework sourcing playbooks: Use blended supplier strategies and conditional contracts to hedge against feedstock inflation and anti-dumping duties. Prioritize suppliers with local certification and contingency production capacity.

- Accelerate formulation audits: Conduct rapid audits of product portfolios against new concentration limits and labeling requirements. Implement prioritized reformulation pilots where regulatory impact is highest.

- Invest in greener chelates selectively: Target R&D and co-development with specialty suppliers where end-customer willingness to pay covers the incremental cost of biodegradable alternatives.

- Leverage certification as a market lever: For players selling into potable-water and sensitive applications, pursue targeted certifications that convert to procurement privileges and premium pricing.

- Identify acquisition and alliance targets: Screen targets based on regional regulatory barriers, technical competencies and downstream channel access; prefer bolt-on assets that shorten time-to-market for regulated formulations.

How PW Consulting can support your 2026 program

Our Edta Solution Market report is built for execution. Clients who subscribe receive the full forecast model, supplier heatmaps, scenario dashboards and an implementation pack including playbooks and slide-ready decision frameworks. We also offer tailored advisory sprints: three-week rapid assessments for procurement re-negotiations, eight-week reformulation feasibility studies, and custom M&A diligence packages.

Closing — the strategic value proposition

As companies set budgets and make sourcing, R&D and M&A decisions for 2026, the combination of input-price volatility, regulatory tightening and evolving end-customer preferences turns the EDTA solutions market from a routine procurement category into a strategically significant lever. Our report equips leaders with the data, scenarios and tactical workstreams to protect margins, secure supply and capture upside from the shift toward sustainable chelation chemistries — while deliberately withholding granular segmentation tables in this public summary to preserve the full commercial context for report subscribers.

Accessing the full intelligence

To unlock the complete dataset, detailed segmentation, supplier share matrices and the downloadable model that underpins our recommendations, visit the PW Consulting insights portal to download the full Edta Solution Market report and associated implementation materials.

For detailed analysis of this topic, please visit the official page:Edta Solution Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com