Refractory Bricks Market 2026: Strategic Intelligence Briefing for Executive Decision-Making

PW Consulting’s new Refractory Bricks Market report (base year 2025; historical period 2020–2025; forecast 2026–2032) translates granular sector dynamics into boardroom-grade strategic options. The global shaped-refractories market has demonstrated steady recovery and structural growth through the recent cycle — expanding from roughly USD 17.1 billion in 2020 to about USD 21.45 billion in 2025 — and PW’s forecast models indicate a continuation of that trajectory to the end of the forecast window. At a compound annual growth rate (CAGR) of 4.62% for the forecast period, the market’s absolute scale and progressive resilience create a window of strategic choices for raw-material buyers, plant operators, investors and M&A teams in 2026.

Refractory Bricks Market

Why this report matters for 2026 corporate plans

Refractory bricks sit at the nexus of heavy industry, raw-material markets and decarbonization pressures. For executives preparing 2026 budgets and three- to five-year capital plans, the report provides actionable intelligence across four decision vectors:

Refractory Bricks Market

- Supply security and raw-material risk mitigation: contextualized exposure assessments that map critical input concentrations to procurement strategies and contingency buffers;

- CapEx prioritization: scenarios that align refractory lifespan and replacement cycles with modernization investments in steel, cement and glass plants;

- M&A and partnership screening: value maps that synthesize capacity, technology and geographic footprint into acquisition scorecards; and

- ESG and regulatory alignment: tactical roadmaps for compliance with emissions regimes and low-carbon product positioning—important as policymakers increase scrutiny of energy- and material-intensive ceramics manufacture.

What the report contains — practical, execution-focused deliverables

- Market sizing and multi-scenario forecasts (USD Million; 2026–2032) that translate top-line growth into unit-demand and replacement cycles for major industrial applications.

- Supply-chain heatmaps identifying single-source exposures for alumina, magnesia and silica, and a quantitative assessment of how raw-material volatility can move cost structures (raw materials constitute a dominant share of production costs).

- Competitive landscape dossiers on the sector’s leading and regional players, benchmarked on capacity, product mix, integration and service models, together with an M&A readiness checklist.

- Commercial playbooks for procurement and aftermarket services — including negotiation levers, vendor consolidation tactics and logistics optimization templates designed for 2026 tender cycles.

- Technology and product roadmaps highlighting near-term substitution risks (e.g., monolithics and fused-cast alternatives), performance-improvement levers, and product differentiation pathways for premium high-temperature bricks.

- Regulatory and carbon transition matrices specific to key jurisdictions, with pragmatic compliance timelines and cost estimates for policy-driven scenarios.

- Investment cases and stress tests tailored to private equity and corporate M&A teams, inclusive of integration risks and upside levers under different demand and raw-material price assumptions.

Market dynamics and structural themes to watch in 2026

Our analysis identifies three durable forces that will shape strategic returns in the coming 18–36 months:

Refractory Bricks Market

- Raw-material concentration and price volatility. Production of refractory bricks is highly sensitive to movements in key inputs—alumina, magnesia and silica—and these inputs account for a large portion of manufacturing cost. Price spikes and trade-policy moves materially influence margins and sourcing strategies.

- Decarbonization and regulation. Emissions regulations are converging on high-temperature industrial ceramics. For example, producer-level emissions regimes in the EU now explicitly target ceramic-product firing within defined capacity thresholds. This raises capital and operating-cost implications for incumbent producers and creates openings for low-carbon product differentiation.

- Demand hinge on primary metal outputs. The fortunes of refractory bricks continue to be tied to global steel output and other heavy industries. PW’s scenario models incorporate both cyclical demand shocks and structural shifts in steelmaking routes and glass/cement production patterns.

Competitive landscape: who is shaping the sector

The market remains moderately fragmented: the three largest firms capture a meaningful but not dominant share of global revenue, with the top five firms controlling under half the market—creating space for regional champions and focused specialists. Major players include vertically integrated global producers and nimble regional manufacturers.

- RHI Magnesita (Vienna) operates an end-to-end platform across magnesia-carbon, high-alumina and fireclay bricks, leveraging scale and integration to serve steel and cement clients globally.

- Vesuvius PLC (London) competes on high-performance shaped refractory solutions for metals and foundry sectors, with product engineering and metallurgical expertise as differentiators.

- Shinagawa Refractories (Tokyo), Krosaki Harima (Kitakyushu) and several East Asian manufacturers maintain strong regional positions and export footprints that influence global pricing and capacity balance.

- Specialist and regional firms—IFGL Refractories (Kolkata), HarbisonWalker International (Pennsylvania), Resco Products (Pittsburgh) and selected Chinese and Korean groups—support local maintenance cycles and bespoke product needs, often dominating aftermarket and service contracts.

Recent market moves reinforce strategic themes. A 2026 regional acquisition by Plibrico sharpens inventory reach in the U.S. Southeast; a substantial capacity expansion by a North American plant operator underscores the consolidation of monolithic and shaped-product supply; and awards for low-carbon initiatives highlight the competitive premium for innovation. PW’s company dossiers synthesize these events into forward-looking competitor intent matrices and integration playbooks.

Regulatory, trade and raw-material considerations

Three regulatory and trade signals deserve immediate attention from procurement and strategy teams:

- Emissions trading and compliance scopes that now encompass ceramic product firing in certain jurisdictions increase the pass-through risk from energy and carbon costs to finished-brick pricing.

- Trade measures affecting critical refractory minerals have shifted supply dynamics in recent years; import-duty decisions and export controls alter sourcing economics and merit contingency stock strategies.

- Given the sector’s raw-material intensity, even modest resource-price moves can compress margins rapidly. PW’s sensitivity matrices quantify the profit and working-capital implications of headline swings in alumina and magnesia markets.

Strategic playbook for 2026

Based on our integrated forecasting and competitive analysis, PW recommends five prioritized actions for different stakeholders:

- For buying organizations: accelerate supplier qualification to include low-carbon and near-sourced options; adopt forward-purchase protocols for critical minerals tied to budget cycles.

- For producers: prioritize retrofit and energy-efficiency investments that reduce exposure to emissions pricing and improve product cost curves; consider strategic alliances to access feedstock or logistics synergies.

- For investors and M&A teams: screen targets using PW’s proprietary scorecard that weights technical capability, aftermarket service capture, and regulatory readiness more heavily than simple capacity metrics.

- For plant operators: integrate refractory-replacement scheduling into outage planning to capture those synergies that reduce thermal shocks and extend brick life—delivering immediate cash-flow improvements.

- For innovation leaders: invest selectively in performance bricks that extend campaign life in electric-arc and alternative-route steelmaking; early movers on demonstrably lower-carbon products can capture premium procurement slots.

What you won’t find in this briefing — and why

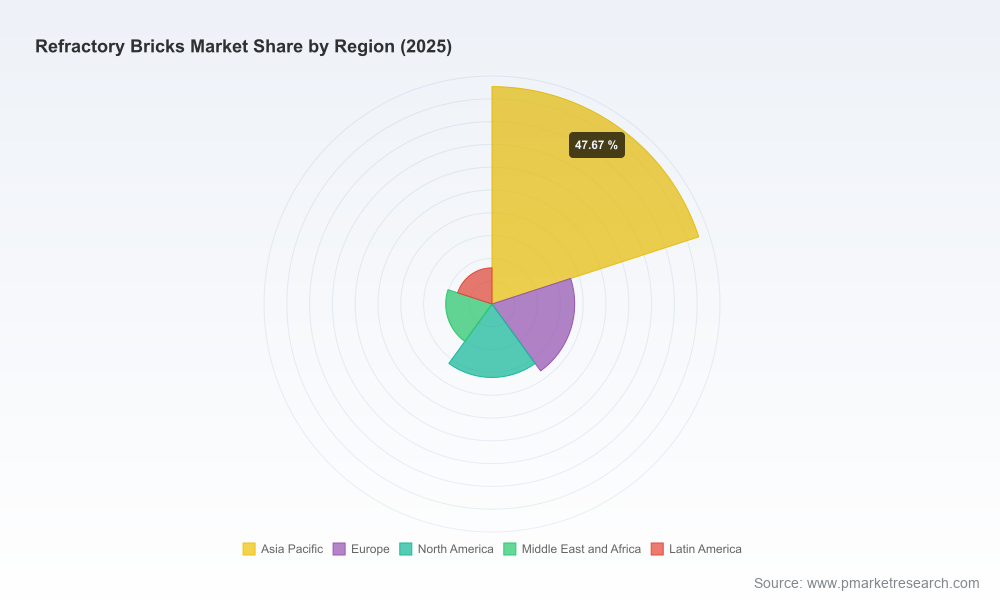

To preserve PW’s value-led advisory model and drive engagement with the full dataset, this briefing intentionally does not disclose detailed regional and application-level segment percentages or proprietary unit-price schedules. The core report contains those critical segmentation tables, regional demand curves and application-specific replacement cycles which are essential for transaction-level diligence and procurement tendering. PW’s “trailer” approach provides strategic clarity while channeling sensitive, actionable data through the full report delivery.

How PW Consulting supports implementation

Beyond analysis, PW offers tailored engagements designed to convert insight into outcome in 2026:

- Operational due diligence for M&A and JV formation, including site-level refractory audits;

- Procurement transformation sprints to implement hedging, vendor rationalization and near-sourcing pilots;

- CapEx prioritization workshops that align refractory lifecycle planning with decarbonization roadmaps;

- Scenario-based stress testing for investors to model downside shocks and upside demand accelerations.

Next steps

Executives preparing 2026 strategies should treat refractory bricks not as a commoditized input but as a strategic lever that intersects supply-chain risk, decarbonization policy and industrial performance. PW’s full report furnishes the confidential segment matrices, supplier rankings, cost-sensitivity tables and jurisdiction-by-jurisdiction regulatory timelines necessary to convert the strategic imperatives above into executable plans. Contact PW Consulting to access the full dataset, tailored regional annexes and engagement options for rapid implementation.

For detailed analysis of this topic, please visit the official page:Refractory Bricks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com