Fluorine-18 Market Insights: Expanding Role in Precision Healthcare

Health |

2026-06-22 08:37:34

PW Consulting’s Tobacco Leaves Market report (base year 2025; historical 2020–2025; forecast 2026–2032) equips commercial leaders and policy teams with the strategic intelligence required to make high‑stakes decisions in 2026. At the aggregate level, the market sits in the low‑tens of billions of USD and is projected to expand from an estimated USD 33.5 Billion in 2025 to roughly USD 41.9 Billion by 2032, reflecting a steady compound annual growth rate (CAGR) of approximately 3.25% through the forecast horizon. This trajectory captures a mix of structural demand resilience, product mix shifts, and evolving cost and regulatory headwinds. The report synthesizes these dynamics into operational playbooks and decision frameworks tailored for producers, merchants, manufacturers and institutional investors.

Tobacco Leaves Market

2026 will be a year of selective repositioning rather than wholesale transformation. Firms that move early to operationalize the report’s recommendations will gain asymmetric advantage in three areas:

Tobacco Leaves Market

PW Consulting’s research deliberately balances strategic narrative with executable tools. The report’s structure is purpose‑built for 2026 deployment and includes:

Tobacco Leaves Market

The leaf market is neither fully atomized nor dominated by a single global buyer. Our concentration analysis shows that the three largest merchants account for a material share of global flows, with the top five controlling a clear majority. That market geometry creates predictable pressure points: bargaining power for large processors when supply tightens, and opportunity for scale‑efficient intermediaries to extract margin through logistics and processing integration. For corporate strategy teams, this implies a twofold priority in 2026 — secure dependable upstream relationships while investing selectively in midstream capabilities to neutralize concentration risk.

Our company‑level coverage synthesizes capability, geographic footprint, and recent strategic moves for leading market participants. Highlights include:

Recent market events reinforce the need for adaptive strategies: Alliance One’s regional facility consolidation, China Tobacco International’s framework agreements to formalize exports, and export expansion moves by large origin firms—each signal a landscape where operational consolidation, contractual formalization, and origin capability investments will define winners in 2026.

Origin economics remain central to strategy. Trade data from early 2026 confirms Brazil’s continued leadership in raw tobacco exports by value and underscores India’s breadth as a high‑volume exporter servicing an extensive global destination set. The United States continues to export significant volumes of premium flue‑cured and Burley leaf, supporting established premium supply chains. Average global export prices have climbed materially, reflecting post‑pandemic freight dynamics, input cost inflation, and selective quality premiums—factors procurement and pricing teams must embed into 2026 budgets.

Regulatory settings are shifting from product‑focused control to supply‑chain governance. Agricultural and sustainability standards—exemplified by the EU Green Deal’s continued influence on import costs and compliance requirements—are increasing the cost of entry into certain markets for non‑compliant suppliers. Parallel initiatives at origin—such as eco‑curing pilots that reduce carbon intensity while lowering fuel cost exposure—offer a dual path to compliance and cost reduction. In 2026, executives should treat sustainability investments as risk mitigants and near‑term commercial differentiators, not just long‑term reputational projects.

We model three plausible scenarios—baseline (moderate steady growth), stress (adverse regulatory and logistics shocks), and upside (faster premium uptake and technological efficiency). Each scenario yields different prescription sets, from securing long‑dated contracts and diversifying origins under stress, to accelerating value‑added processing capacity and premium channel development in the upside case. The report supplies decision matrices that map scenario outcomes to specific capital, procurement and commercial actions, enabling leaders to prioritize scarce investment dollars in 2026.

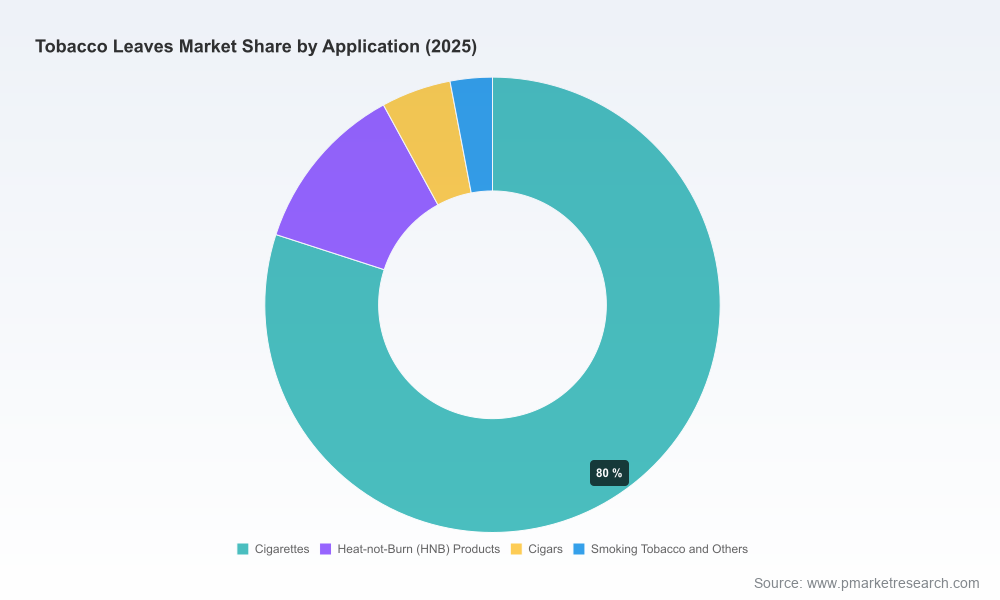

The report follows a “trailer” approach: it discloses high‑level market sizing, growth rates, competitive patterns and strategic playbooks to inform decision urgency and direction. Detailed origin‑level shares, specific application splits, and individual contract templates are intentionally reserved for the full report and supporting datasets. This is to protect commercially sensitive granularity and to ensure interested stakeholders obtain the complete evidence base directly from PW Consulting, where the data is provisioned with validation and update guarantees.

Use this preview to align executive priorities for 2026 planning cycles: integrate the recommended supplier resilience measures into Q1 procurement strategy reviews, scope pilot investments in low‑carbon curing for mid‑year trials, and task corporate development to revisit M&A criteria with an emphasis on midstream capability. For boards and investors, the report provides a concise framework to stress‑test existing exposure to commodity, regulatory and concentration risks and to re‑weight capital allocation toward resilience and value capture.

The full Tobacco Leaves Market report contains the underlying datasets, origin and application scenarios, supplier scorecards, and proprietary modeling templates necessary to operationalize the strategies summarized here. For company‑specific briefings, bespoke scenario runs, or dataset licenses to integrate into planning systems, please visit the PW Consulting report page or contact the author team for authenticated access.

PW Consulting — Strategic insight, operational playbooks, and the market data leaders rely on to make decisions in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Tobacco Leaves Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com