Tripterygium Glycosides Tablets Market — Strategic Outlook for 2026

PW Consulting is pleased to release an executive briefing drawn from our full Tripterygium Glycosides Tablets (TGT) Market Report. As senior strategic advisors and industry analysts, our objective is to translate complex clinical, regulatory and commercial dynamics into a pragmatic decision framework executives can use in 2026. This briefing showcases the analytical depth of the full study while reserving core segmented datasets and model outputs for report subscribers.

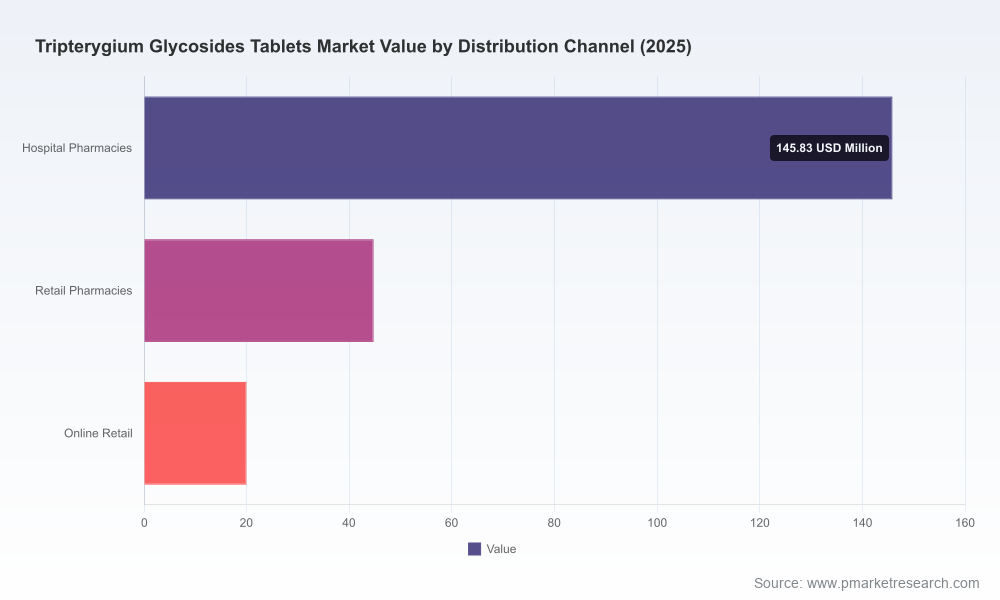

Tripterygium Glycosides Tablets Market

Market trajectory and macro view

TGT is an established therapeutic class within China’s treatment landscape for autoimmune conditions, and our macro model captures the market’s recovery and mid-term expansion. Using 2025 as the base year, our historical window (2020–2025) shows a rebound from disruption earlier in the decade to a stabilized market in 2024–2025. The total market grew from USD 165.2 Million in 2020 to USD 210.5 Million in 2025. Our forecast for 2026 begins at USD 224.0 Million and the model projects growth through the 2026–2032 horizon, arriving at USD 298.6 Million by 2032—a compound annual growth rate (CAGR) of 5.12% across the forecast period.

Tripterygium Glycosides Tablets Market

These headline figures reflect a market driven by persistent clinical demand in rheumatology and nephrology, continued guideline inclusion in China, and incremental product and quality developments. However, growth is not uniform across channels or applications—details and region/application splits are included in the full report to support market entry or portfolio prioritization decisions.

Tripterygium Glycosides Tablets Market

What the full report delivers (practical, ready-to-use modules)

- Proprietary market-model (2020–2032) with scenario engines for demand, pricing and reimbursement—enables rapid re-forecasting under alternative assumptions.

- Regulatory and clinical roadmap mapping: approval status, safety profile synthesis, and recommended evidence generation strategies to reduce regulatory risk.

- Supply-chain and CMC stress-tests: raw material variability analysis, batch-level fingerprint comparisons, and contingency planning for upstream shortages.

- Commercial playbooks by channel and stakeholder: hospital formulary engagement, physician outreach, and digital patient acquisition tactics tailored to the TGT context.

- Competitive benchmark and capability heatmaps: strength/weakness matrices across manufacturing, clinical support, quality systems and IP/know‑how.

- M&A and partnership scouting: prioritized target lists and valuation sensitivity—designed to accelerate inorganic growth or secure capabilities quickly.

- Financial templates and pricing sensitivity tools calibrated to local payer dynamics and guideline inclusion scenarios.

Why this matters for 2026 decision-makers

Executives face three interlocking imperatives in 2026: (1) protect and grow incumbent revenues amid safety and quality scrutiny, (2) de-risk potential international expansion where regulatory acceptance is limited, and (3) identify acquisition or partnership targets that provide manufacturing standardization and clinical evidence capabilities. Our market model and scenario planning are purpose-built to inform capital allocation, R&D prioritization and go-to-market sequencing under each of these imperatives.

Key strategic insights

- Evidence-first commercialization: Given TGT’s safety profile and limited global approvals, investment in rigorous, well-designed clinical studies that address hepatotoxicity and reproductive risk will materially expand strategic optionality. The studies published and ongoing through 2025–2026 show renewed focus on mechanism elucidation and toxicity mitigation—corporate sponsors should prioritize trials that generate both safety biomarkers and real-world outcome data.

- Quality and analytical differentiation: Reported variability in chemical composition across manufacturers is not a downstream nuisance—it is a core commercial inhibitor. Companies that build validated UPLC/biomarker-based release strategies and transparent batch comparability will win formulary trust and shorten procurement cycles.

- Regulatory pathway engineering: With TGT approved and widely used in China but lacking approvals outside, 2026 should be the year to develop de-risked regulatory programs (e.g., bridging studies, pharmacovigilance-led dossiers) rather than immediate global filings. Our regulatory playbooks provide stepwise approaches that balance cost, timeline and risk.

- Consolidation and capacity plays: The market exhibits moderate concentration—leading manufacturers control a sizeable share. Expect acquisition interest in high-quality production assets and analytical labs capable of reducing batch variability.

- Reimbursement and guideline engagement: TGT’s inclusion in Chinese clinical guidelines provides a platform for adoption, but payer engagement remains essential to protect margins. Early dossiers emphasizing comparative effectiveness and safety monitoring lower payer resistance.

Competitive landscape — who matters and why

The TGT manufacturing base is concentrated among a handful of established players that serve research and clinical markets. Key domestic manufacturers have differentiated on supply to clinical studies, cost-efficient production for the domestic market, or positioning as reliable suppliers for hospital systems. For executives evaluating partnerships or M&A, the following high-level profiles summarize capability clusters and strategic implications (full company profiles and SWOTs are in the report):

- Manufacturers supplying clinical studies and university hospitals—these firms bring credibility and trial experience; partnering can accelerate evidence generation.

- Cost-focused producers that dominate commodity supply—acquisitions here can secure margin improvement and scale, but often require investment in analytics and quality systems.

- Regionally focused suppliers that maintain close hospital relationships—strategic distribution partnerships with such players are efficient routes to hospital adoption.

- Emerging technology providers and research-focused organizations—these partners are useful for mechanism studies, formulation improvements and toxicity mitigation research.

Our competitive analysis also flags likely near-term moves: upgrades to GMP and analytics, selective capacity expansion to capture hospital formulary wins, and consolidation activity by domestic players targeting higher-margin segments. The full report contains ranked acquisition targets and partnership fit matrices with valuation sensitivities.

Recent developments shaping 2026 strategy

- Academic and clinical publications in 2025–2026 reinvigorated discussion about mechanism-of-action, mitigation of toxicity, and potential novel indications—this trend creates windows for differentiated clinical programs.

- Supply and composition variability studies from 2023 onwards have increased buyer scrutiny; procurement teams now request batch-level analytical data and comparability reports before awarding contracts.

- Guideline and payer dynamics in China continue to support clinical use for rheumatoid arthritis and certain nephrotic syndromes, underpinning baseline demand even as safety monitoring becomes more stringent.

Operational recommendations — a 90- to 180-day action plan for 2026

- Initiate a targeted clinical evidence program focused on safety biomarkers and head-to-head comparative endpoints; use adaptive designs to shorten timelines and reduce cost.

- Invest in analytic center-of-excellence (UPLC/MS and bioassay capabilities) or secure a technology partnership to standardize release and comparability testing.

- Run a payer-scenario simulation (included in our report) to determine optimal price points and reimbursement submission sequencing in China.

- Screen and prioritize inorganic targets using the PW Consulting M&A scorecard—focus on quality upgrades and trial supply capability rather than pure volume plays.

- Design a pharmacovigilance-led post-marketing surveillance program that answers hepatotoxicity and reproductive risk questions—this materially reduces regulatory friction for any cross-border steps.

- Stress-test your supply chain against raw-material variability and create a dual-sourcing plan for critical inputs.

Why PW Consulting’s report is strategically valuable

Decisions in 2026 will be made under a mix of clinical uncertainty, tightening quality expectations, and persistent domestic demand. Our report converts these conditions into executable options: calibrated investment cases, regulatory playbooks, and commercial go-to-market sequences tied to quantified market scenarios. We provide the tools to triage investment opportunities, prioritize transactions, and operationalize quality and safety as commercial differentiators.

Next steps — access and engagement

This briefing is a strategic preview. The full Tripterygium Glycosides Tablets Market Report includes the granular segmentation, channel- and application-level models, downloadable financial templates, and full company dossiers that underpin the recommendations above. PW Consulting offers bespoke workshops to translate the report’s outputs into an executable 12–24 month plan tailored to your organization’s objectives.

For executives evaluating portfolio moves, supply agreements, or evidence programs in 2026, the report provides the analytical scaffolding to act with speed and confidence. Visit our website to request the full report and to schedule a private briefing with our lead analysts.

For detailed analysis of this topic, please visit the official page:Tripterygium Glycosides Tablets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com