Liquid Hazardous Waste Management Market 2026: Strategic Intelligence Brief for Executive Decision-Making

Executive snapshot

PW Consulting’s latest market intelligence for the Liquid Hazardous Waste Management sector frames 2026 as an inflection year for asset owners, service providers, and industrial generators. Our analysis—anchored in a historical baseline (2020–2025) and a detailed forecast through 2032—shows a resilient global market that has expanded from approximately USD 36 billion in 2020 to roughly USD 48.5 billion in 2025, and is projected to reach about USD 73.3 billion by 2032. This trajectory corresponds to a compound annual growth rate (CAGR) of 6.08% across the 2026–2032 forecast window.

Liquid Hazardous Waste Management Market

Why this matters for 2026 decision cycles

- Capital allocation: Increasing scale, predictable growth, and pockets of tightening capacity mean that investment timing for treatment capacity, high-temperature incineration, and solvent recovery assets will determine multi-year cost of service and market share.

- M&A and consolidation: Strategic acquirers and financial sponsors are actively reshaping footprints—domestically and cross-border—creating windows for bolt-on acquisitions, roll-ups, and capacity buys that can alter regional supply-demand balances.

- Regulatory risk and upside: Near-term rulemaking (including digital manifest mandates and evolving universal-waste treatments) is re-writing compliance costs and operational requirements; early movers that align systems, data flows, and transport logistics will convert compliance into competitive advantage.

- Commercial optimization: Generators face rising disposal complexity and unit-cost variability. Contract design, local access to specialized treatment, and logistics optimization are now primary levers to protect margins and ensure continuity of operations.

Market trajectory and what the numbers mean

The sector’s steady expansion in the last half-decade reflects three interacting forces: steady industrial output in core generator industries, rising environmental compliance complexity, and targeted capacity investments by service providers. The headline figures—growth from roughly USD 36 billion in 2020 to USD 48.5 billion in 2025, and a projected climb to ~USD 73.3 billion by 2032 at a 6.08% CAGR—are indicators of both enduring demand and attractive near-term return profiles for strategically sited capacity.

Liquid Hazardous Waste Management Market

For 2026 strategy planning, this implies that:

Liquid Hazardous Waste Management Market

- Capacity investments initiated now will likely capture the next wave of demand growth; project lead times and permitting cycles make early action essential.

- Service providers with diversified treatment technologies and integrated logistics networks will be positioned to extract disproportionate value as customers consolidate vendors to manage complexity.

- Pricing power will increasingly reflect localized capacity tightness and regulatory compliance costs rather than purely commodity disposal rates.

Competitive landscape: capabilities, moves, and implications

The market combines a set of global integrators, national champions, and specialized technology providers. Leading incumbents bring differentiated strengths:

- Veolia Environnement SA (Aubervilliers, France) operates as a global integrator with broad capabilities across collection, incineration, recycling, and solvent recovery, and has been highly acquisitive to expand U.S. hazardous waste capabilities—moves that materially enhance both transport and high-temperature treatment capacity.

- Clean Harbors, Inc. (Norwell, MA) remains a North American leader in emergency response, vacuum collection, and industrial services, with deep operational scale in hazardous liquid treatment.

- Waste Management, Inc. (Houston, TX) and Republic Services, Inc. (Phoenix, AZ) leverage national logistics networks and innovation in treatment technologies to support large commercial and industrial generators.

- Specialist providers such as Stericycle, Covanta, GFL Environmental, Heritage-Crystal Clean, and others fill niches—regulated medical hazardous liquids, energy-from-waste synergies, and solvent/oil-centric services—creating a layered competitive set across scale and specialization.

- Smaller, technology-focused firms (including Perma-Fix, Tradebe, Liquid Environmental Solutions) provide differentiated solutions for mixed, radioactive, or non-standard streams and are frequently partners or targets in consolidation plays.

Recent strategic developments underscore the pace of change. Notable transactions and capacity moves—reported in 2025–2026—include multi-company acquisitions and targeted capacity expansions that materially shift accessible treatment capacity for liquid streams. These developments create near-term dislocations in regional capacity that astute market participants can exploit through network optimization, contract renegotiation, and selective capital deployment.

Regulatory and policy dynamics shaping 2026 choices

- Digital transition in manifests: Regulatory bodies are accelerating digital manifesting systems that will standardize data flows across generator, transporter, and treatment nodes. Operational readiness for electronic manifests is a critical compliance and efficiency lever.

- Expanded waste definitions: Emerging rulemakings—targeting battery and photovoltaic wastes and amendments to international waste transfer protocols—are increasing cross-border complexity and the need for compliant handling of liquid components in electronic and battery waste streams.

- Permitting headwinds: State-level moratoria and planning requirements are lengthening lead times for new or expanded treatment facilities in select jurisdictions, elevating the value of permitted capacity and influencing siting strategies.

For executives, the takeaway is clear: regulatory developments are not a distant compliance item but a core commercial variable that reshapes cost curves, transport patterns, and the economics of decentralization vs. centralized treatment.

What PW Consulting’s report delivers (practical, executable content)

This report is designed as a decision-grade toolkit for 2026 and beyond. It combines market-level forecasting with operational diagnostics and commercial playbooks to translate macro trends into executable steps. Key deliverables include:

- Transparent market-sizing and forecasting methodology with scenario-based sensitivities that allow users to model alternative regulatory and capacity outcomes across the 2026–2032 horizon.

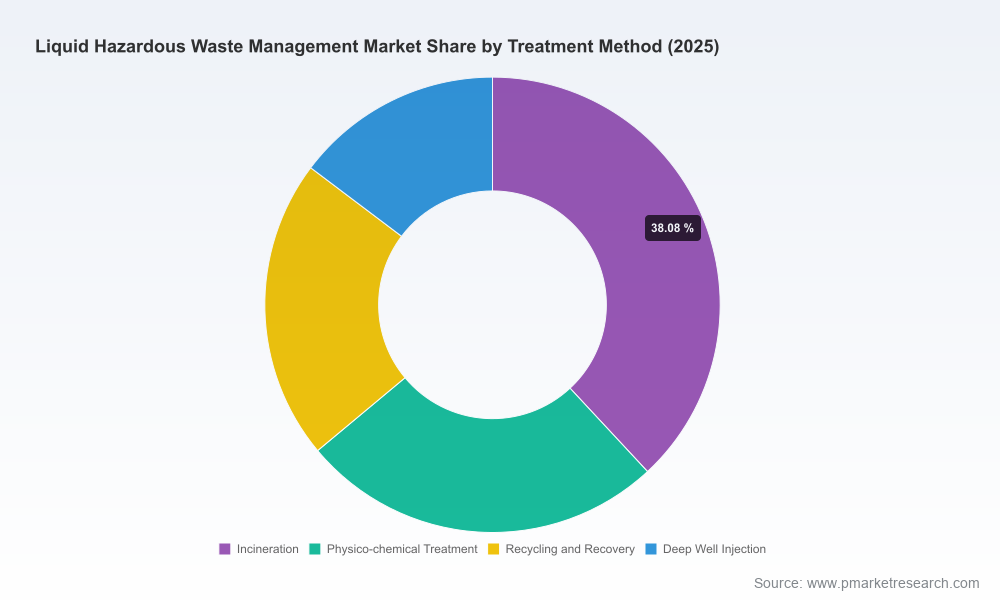

- Service-line and technology profiles that map treatment pathways (from incineration and physico-chemical approaches to recycling/recovery and deep injection) to capital intensity, operating cost bands, and typical project timelines—presented as comparative decision matrices rather than raw segment allocations.

- Permitting and siting playbook: best-practice checklists, typical approval timelines, and contingency planning for jurisdictions with heightened permitting risk.

- Commercial and contracting templates: risk-sharing structures, indexed pricing approaches, and logistics optimization models designed to improve margin capture for both service providers and large generators.

- M&A and partnership diagnostic: valuation benchmarks, integration risk maps, and a prioritized list of capability gaps that are most accretive to scale or specialization strategies.

- Regulatory impact scenarios and compliance roadmaps: practical steps to operationalize electronic manifests, manage international shipment constraints, and prepare for expanded universal waste categories.

- Data assets and proprietary models: a suite of financial models, unit-cost simulators, and capacity utilization dashboards that clients can license and adapt to their portfolios.

How different stakeholders should use this intelligence in 2026

- Operators and asset owners: fast-track permitted-capacity acquisitions, prioritize investments in treatment flexibility (to handle mixed and emerging streams), and lock in logistic corridors to defend generator relationships.

- Private equity and infrastructure investors: use our scenario models to stress-test cash flows under regulatory tightening and localized capacity shocks before committing to greenfield assets.

- Industrial generators (chemical, pharmaceutical, manufacturing): redesign waste-sourcing strategies to reduce single-point exposure, implement digital manifest readiness projects, and revisit long-term treatment contracts to incorporate flexibility and compliance pass-throughs.

- Technology and service innovators: target partnerships with networked integrators to scale piloted recovery and recycling technologies; treat regulatory change as a demand-creation mechanism for safer, more traceable solutions.

Why PW Consulting’s report is different

We combine macro forecasting rigor with front-line operational expertise. The report is not a static dataset: it includes playbooks used in client engagements, a validated pipeline of likely capacity changes, regulatory scenario modeling, and an M&A readiness checklist tailored to hazardous liquid streams. Importantly, to preserve immediate commercial value for report purchasers, we present complete segmentation and granular competitive positioning within the full report—guided by strict confidentiality and source validation—while this briefing intentionally focuses on strategic implications rather than detailed splits.

Next steps and how to access the full intelligence

For decision teams planning 2026 capital allocation, commercial negotiation, or regulatory engagement, the full PW Consulting Liquid Hazardous Waste Management Market report provides the granular segmentation, region- and treatment-level detail, proprietary cost curves, and supplier-by-supplier analysis required to convert strategy into executable plans. The public briefing above highlights the strategic contours and data-backed direction of travel—our premium report supplies the underlying models and targeted intelligence that enable confident deals and operational moves.

To discuss bespoke applications of the report or to arrange a private briefing for your executive team, contact PW Consulting’s Chemicals & Waste Practice. Our advisory engagements translate the report’s insights into board-ready recommendations, transaction support, and implementation roadmaps tailored to your portfolio.

For detailed analysis of this topic, please visit the official page:Liquid Hazardous Waste Management Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com