Europe Orthopaedic Braces and Supports Market Industry Report: Opportunities & Future Trends

Health |

2026-04-30 12:38:08

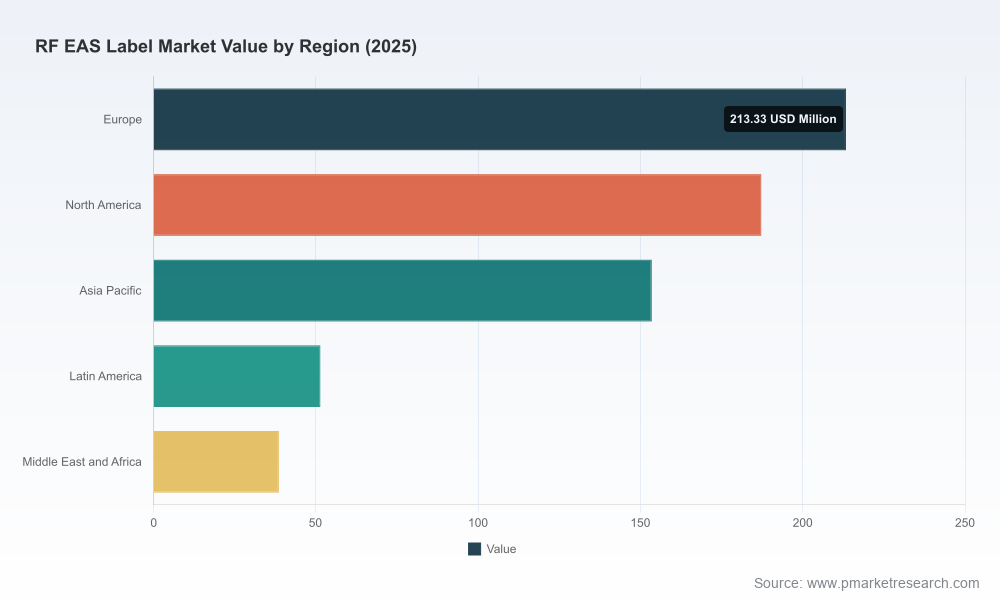

As retailers, brand owners, and security technology providers plan capital allocation and sourcing strategies for 2026, a clear, operational view of the RF EAS label market is essential. PW Consulting’s new Rf Eas Label Market report (base year 2025; historical review 2020–2025; forecast 2026–2032) synthesizes longitudinal market data, supplier intelligence, regulatory trajectories, and deployment playbooks to translate macro trends into executable decisions. The global market reached roughly USD 644 million in 2025 and, at a projected 3.99% CAGR, is expected to expand toward the upper end of the forecast envelope by 2032—an environment that rewards targeted investments rather than broad, unfocused expansion.

Rf Eas Label Market

Convergence of technologies: RF EAS labels are no longer a standalone loss-prevention commodity. Vendors and retailers are integrating RF EAS with RFID, point-of-sale antennas, cloud management, and inventory orchestration—creating new capture points for data and new vendor lock-in dynamics.

Rf Eas Label Market

Heightened organized retail crime and shrink pressures have increased willingness to invest in more advanced label types and source-tagging programs, while operational budgets remain constrained by modest overall market growth.

Rf Eas Label Market

Regulatory reshaping of packaging economics—driven by Extended Producer Responsibility (EPR) schemes and EU packaging policy—creates both cost and compliance imperatives for labels and adhesives that are embedded in packaging streams.

Actionable executive summary with 12–24 month decision windows for procurement, sourcing, and technology pilots.

Validated market-sizing and a transparent forecasting model (2026–2032) that illustrates sensitivity to adoption rates, retail mix shifts, and commodity cost shocks.

Supplier scorecard and concentration analysis that maps strengths, manufacturing footprints, and strategic fit for different retail operating models.

Technology and operations playbooks: RF-to-RFID integration patterns, anti-metal and micro-label solutions, automated source-tagging workflows, and in-store checkout antenna strategies.

Compliance & sustainability toolkit: EPR readiness checklist, material substitution pathways, and an impact assessment for packaging regulation scenarios.

Commercial negotiation frameworks: sample RFP templates, contract clauses for supply continuity, and total cost of ownership (TCO) calculators that incorporate regulatory fees and end-of-life handling.

Case studies and staged implementation timelines to move from pilot to roll-out while preserving store ops continuity.

The RF EAS label market sits in a moderately concentrated competitive structure: the top three players account for a meaningful share of market sales, and the top five increase that concentration further. This positioning favors well-capitalized global suppliers that combine R&D, platform capabilities and manufacturing scale with nimble regional producers able to serve source-tagging and customization needs.

Key supplier archetypes and strategic implications highlighted in the report:

Platform-integrated incumbents: Firms that pair large product portfolios with cloud and systems integration capabilities—exemplified by vendors introducing cloud-based store operations platforms and POS-integrated antennas—are focusing on the higher-margin systems and services layer. These vendors are best positioned to monetize long-term service contracts and cross-sell RFID and data services to enterprise retailers.

Source-tagging specialists: Manufacturers with deep expertise in apparel and consumer-goods source tagging (including micro-labels, anti-shielding variants, and specialized adhesives) are capitalizing on retailer pushes to migrate tagging upstream into the supply chain.

Regional low-cost manufacturers: Several China-based suppliers continue to scale by offering highly customizable soft labels and aggressive price-performance trade-offs. They are often the preferred partner for high-volume, price-sensitive rollouts, but bring additional diligence requirements around quality assurance and environmental compliance.

Packaging & labeling groups: Global packaging players that add RF EAS capabilities to a packaging portfolio are leveraging customer relationships to win bundled engagements, particularly where sustainability and circularity programs intersect with labeling choices.

Checkpoint Systems (Division of CCL Industries) — Broad portfolio and systems depth; recent moves toward cloud orchestration and checkout-integrated antennas signal a push to own more of the in-store capture and analytics stack.

ALL-TAG Corporation — U.S.-based specialist in apparel source tagging and customizable high-shrink solutions; strategically relevant for retailers prioritizing upstream tagging and loss prevention consistency.

Hangzhou Century Co., Ltd. — Investment in anti-organized-crime hardware (notably new metal-detection integrated systems) and recent trade-show presence indicate a product-led push into higher-security segments.

All4Labels Global Packaging Group — Represents the packaging-embedded label strategy: integrating EAS into broader packaging and sustainability offerings to simplify vendor consolidation for brand owners.

Novatron, Alien-Security, Nanjing Bohang — Regional producers that supply scale, customization, and integrated smart-retail components; they are key partners in cost-driven or regionally focused rollouts.

Notable recent developments—such as cloud-based store operations platforms and POS-integrated antennas from leading suppliers, and new metal-sensitive detection systems—are reshaping procurement criteria. Buyers should evaluate suppliers not only on label performance but also on systems interoperability, data security, and managed-service options.

Materials dependency: RF EAS soft labels typically rely on paper substrates combined with embedded aluminum or copper circuits for resonant antennas. These component choices create exposure to paper, metal foil and adhesive supply chains; buyers should model lead-time and cost volatility scenarios.

EPR and packaging regulation: Evolving EPR schemes and EU packaging rules are introducing cost and reporting obligations for packaging components that include labels. Brands and retailers must evaluate label design and material composition now to avoid retrofitting costs and fee escalations as schemes scale.

Regulatory milestones: Regional law developments are accelerating compliance requirements; state-level packaging EPR laws are already being introduced and should be factored into supplier selection and SKU-level cost models.

Adopt a platform-first procurement stance: Prioritize suppliers that offer integration between EAS hardware, RFID, and cloud store management—this reduces long-term operational friction and creates data capture synergies at checkout and in inventory reconciliation.

Hedge supply via multi-tier sourcing: Maintain a blend of global incumbents for scale and regional or specialty vendors for customization and price flexibility. Include quality, compliance, and sustainability KPIs in supplier SLAs.

Invest in anti-metal and micro-label pilots: For categories with metallic packaging or high-value items, evaluate specialized anti-metal label technology and POS-integrated antennas in controlled pilots before broad deployment.

Embed sustainability into RFPs: Require material disclosure, recyclability metrics, and EPR compliance support from suppliers; quantify potential EPR fee exposure in procurement scoring.

Design modular rollouts: Use phased deployment to preserve store operations continuity: pilot, regional roll-out, cross-category expansion. Attach performance gates tied to shrink reduction and TCO metrics.

Price & margin management: With the market growing modestly at the projected CAGR, prioritize initiatives that improve margin per SKU—automation, source tagging, and inventory accuracy deliver measurable ROI more quickly than broad label portfolio expansion.

Baseline: Modest, steady growth aligned with historical trend lines—invest selectively in systems integration and cost efficiencies.

Upside: Accelerated RFID adoption and stronger regulatory pressure on packaging drive demand for higher-value, integrated labels and managed services—accelerate platform partnerships and premium product development.

Downside: Commodity disruptions or regulatory uncertainty slow deployments—prioritize supply continuity, inventory buffers, and cost-reduction pilots to protect margins.

Supplier selection and contract negotiation support, including supplier scorecards, RFP templates, and transition playbooks.

Pilots and scaling plans for RF-to-RFID integration, anti-metal deployment, and checkout-embedded antenna trials.

Regulatory readiness services: EPR impact modeling, materials substitution pathways, and compliance reporting templates.

Commercial and cost-to-serve modeling to assess lifecycle costs under different uptake and regulatory scenarios.

PW Consulting’s Rf Eas Label Market report is designed as a practical guide: it combines validated market sizing and a clear forecast framework with supplier intelligence and implementation toolkits so decision-makers can move quickly and confidently in 2026. For organizations that need to preserve cash while improving shrink performance and regulatory readiness, the report helps prioritize initiatives that deliver measurable ROI.

To access the full set of data, supplier matrices, scenario models and deployment templates, visit our report landing page for the complete intelligence package and tailored advisory options.

For detailed analysis of this topic, please visit the official page:Rf Eas Label Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com