5G Radome Market 2026: Strategic Intelligence for Executive Decision-Making

As 5G deployments move from early rollouts to scaled commercial expansion, radomes — the often-overlooked enclosures that protect and preserve antenna performance — are transitioning from commodity components to strategic assets. PW Consulting’s latest 5G Radome Market study synthesizes market economics, technology trajectories, supplier positioning, and regulatory tailwinds to deliver actionable guidance for enterprise leaders planning capital investments and supplier strategies in 2026.

5G Radome Market

Executive snapshot

The market for 5G radomes has shown sustained acceleration: from a baseline measured in the low hundreds of millions in 2020, it roughly doubled by 2025 and our forecast anticipates continued expansion through 2032 at a compound annual growth rate of approximately 13% during the 2026–2032 horizon. That trajectory reflects a combination of intensified macro CapEx in 5G infrastructure, material and design innovation to support mmWave performance, and policy moves designed to speed network buildouts.

5G Radome Market

Why radomes matter now

- Network economics no longer tolerate avoidable loss. As operators densify networks and push mid‑band and mmWave spectrum, even small insertion losses or angle-dependent attenuation translate into measurable capacity and ROI impacts.

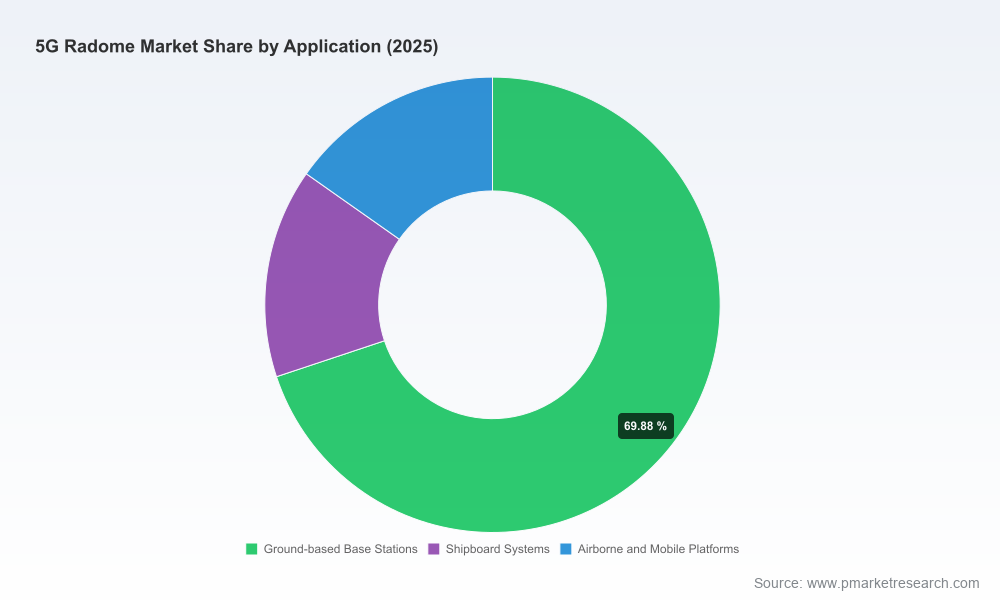

- Integration complexity is rising. Small cells, rooftop macro sites, shipboard and airborne platforms, and indoor distributed architectures impose distinct mechanical, RF and thermal constraints that radome design must reconcile.

- Procurement and life-cycle costs are critical. Given that average deployment cost per 5G base station is substantial, radome selection is increasingly viewed through a total cost of ownership lens — not just a bill-of-materials line item.

Market dynamics shaping 2026 decisions

Several convergent forces will influence radome demand and procurement choices in the coming 12–24 months:

5G Radome Market

- CapEx intensity. Global 5G capital expenditures approached quarter‑trillion‑dollar scale during the recent build cycle, underpinning a steady pipeline of radome‑equipped antennas across deployment types.

- Policy tailwinds. Regulatory actions intended to streamline tower and small‑cell approvals — including proposals in major markets to reduce siting delays — are shortening project timelines and favoring suppliers able to meet compressed delivery windows.

- Spectrum events. Anticipated mid‑band auctions and re‑allocations through the middle of the decade will spur targeted capacity upgrades, creating pockets of near‑term demand for radomes optimized for higher frequencies.

- Supply‑chain and materials pressure. Rising costs in fiber backhaul and imported materials, plus intermittent labor and tariff shocks, emphasize the need for localizable supply options and design approaches that reduce installation complexity.

Technology and product trends to watch

- Material innovation for mmWave transparency. New composite formulations and precision molding approaches are reducing signal attenuation and supporting wider beam angles — a critical capability as massive MIMO and beamforming proliferate.

- Modular, serviceable designs. The move toward modular radome assemblies simplifies field maintenance, accelerates swaps for upgrades, and lowers life‑cycle service costs — a differentiator for operators running dense, heterogeneous networks.

- Injection molding for indoor and small‑cell use cases. Thermoplastic injection‑molded radomes that ensure consistent performance over wide angular domains are gaining traction in indoor and small cell markets where form factor repeatability and cost control matter most.

- Composite core and sandwich constructions. Advanced core materials are enabling lighter, stiffer structures with superior environmental resistance, important for sites exposed to marine or extreme weather conditions.

Competitive landscape — what executives need to know

The supplier ecosystem spans global systems integrators, specialized composites manufacturers, and several vertically integrated defense/aerospace firms adapting technologies for telecom. Rather than a fragmented mass‑market model, the industry exhibits a moderate degree of concentration: a meaningful share of demand flows to well‑established suppliers that combine RF engineering, materials know‑how, and quality control under a single delivery model.

Key players and strategic implications:

- CommScope — With deep antenna enclosure expertise and scale in telecom infrastructure, organizations should view CommScope as a first‑tier supplier capable of supporting wide regional builds and complex macro deployments. Their engineering focus on RF transparency and environmental resilience makes them a strong option for large operator RFPs.

- Exel Composites — An innovator in composite solutions, Exel’s recent patent activity underscores its push to reduce signal attenuation through bespoke composite architectures. Operators and OEMs seeking proprietary performance improvements should engage Exel early for collaborative design work and IP considerations.

- Saint‑Gobain (SHEERGARD) — Known for a portfolio across laminate, sandwich, and tensioned fabric systems, Saint‑Gobain is positioned to serve both macro and small‑cell applications where hydrophobic and environmental performance is prioritized.

- General Dynamics Mission Systems & Meggitt (Cobham AES) — Defense and aerospace radome expertise translates well into high‑frequency telecom use cases. Expect these suppliers to be preferred partners for critical‑environment or dual‑use platforms that demand rigorous qualification processes.

- Laird Connectivity — The company’s recent introduction of an injection‑molded polyolefin radome targeted at indoor mmWave equipment demonstrates the productization trend for small‑cell and indoor markets; this is a signal for operators to explore molded solutions where repeatability and cost per unit are primary drivers.

- Component and materials specialists (e.g., Diab Group) — These suppliers play a subtle but vital role; core materials and sandwich components materially influence radome performance and manufacturability. Supply chain due diligence should explicitly cover availability and qualification timelines for such inputs.

Recent market moves that matter for 2026

- Product launches and patents. Notable examples include Laird Connectivity’s 2025 rollout of an injection‑molded radome optimized for mmWave indoor usage and a 2025 European patent awarded to Exel Composites for a composite radome design focused on reduced attenuation. Such developments signal both accelerating product maturity and increasing IP activity.

- Procurement urgency driven by policy. Regulatory initiatives to streamline siting and approvals are reducing time to market for site deployment — organizations that can shorten procurement lead times will convert that regulatory acceleration into competitive advantage.

- Cost pass‑through and localization. With deployment economics sensitive to material and labor costs, operators are evaluating localized manufacturing and multi‑sourcing strategies to hedge tariff and logistics volatility.

Strategic recommendations for 2026

Executives planning 2026 capital programs should translate market intelligence into concrete actions. Our prioritized recommendations:

- Reframe radomes as performance levers, not mere enclosures. Include RF performance metrics and life‑cycle impact in procurement scorecards; insist on validated insertion loss and angular performance curves rather than vendor assertions.

- Shortlist suppliers across three archetypes. Pair a scale systems supplier for mass deployments, a specialist composite vendor for high‑performance macro/specialty sites, and a molded‑part provider for indoor and small‑cell volumes. This triangulation balances risk, cost and performance.

- Accelerate qualification cycles through early engagement. Begin RF and environmental qualification in Q1–Q2 2026 for any equipment planned for rollout later in the year to avoid program slippage tied to custom radome iterations.

- Factor regulatory calendars into procurement cadence. Align ordering and field trials with anticipated spectrum auctions and local permit streamlining to capture windows of elevated demand.

- Lock in supply of critical core materials. Negotiate medium‑term supply contracts for specialized composite cores and thermoplastic resins to mitigate cost and delivery volatility.

What PW Consulting’s full report delivers

Our comprehensive 5G Radome Market report layers quantitative forecasting with operational playbooks. Highlights include:

- Verified market sizing and forward forecasts through 2032 with scenario stress tests under alternative deployment and spectrum outcomes.

- Supplier benchmarking across RF performance, manufacturing capacity, qualification timelines, and after‑sales service readiness.

- Procurement templates and RFQ language designed to elicit comparable technical data and life‑cycle cost estimates.

- Detailed risk mapping for supply chain, regulatory and material price exposures, including mitigation options.

- Case studies showing radome selection trade‑offs in macro, small‑cell, and non‑terrestrial platforms.

How to use this intelligence in 2026 planning

For CPOs, network planners and product leaders, the practical step is to convert insight into constrained experiments: pilot a dual‑supplier approach on a quarter of the upcoming rollout, validate performance against operator KPIs, and then scale with preferred partners while retaining a secondary qualified source. For CTOs, invest in a six‑month accelerated qualification window for any novel radome material or geometry tied to new antenna form factors. For strategy teams, monitor regulatory timelines and spectrum auction schedules as high‑impact triggers that will create demand waves needing fast supplier responsiveness.

Conclusion — the strategic delta

The 5G radome market is moving from incremental procurement to strategic asset management. With market value having expanded materially since 2020 and forecasts indicating a robust double‑digit CAGR into the early 2030s, the decisions teams make in 2026 about supplier mixes, qualification timelines, and material sourcing will materially affect network performance, deployment speed, and total cost of ownership. PW Consulting’s report provides the executable intelligence to convert that market growth into competitive advantage.

Next steps

To access in‑depth segmentation, supplier scorecards, and the practical procurement toolkit that accompany these insights, please visit our full report page. The public summary is designed as a decisioning trailer — the granular models, scenario outputs, and supplier playbooks are available in the complete study for subscribers and enterprise clients.

For detailed analysis of this topic, please visit the official page:5G Radome Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com