Mobile Business Intelligence (BI) Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-07-01 10:34:11

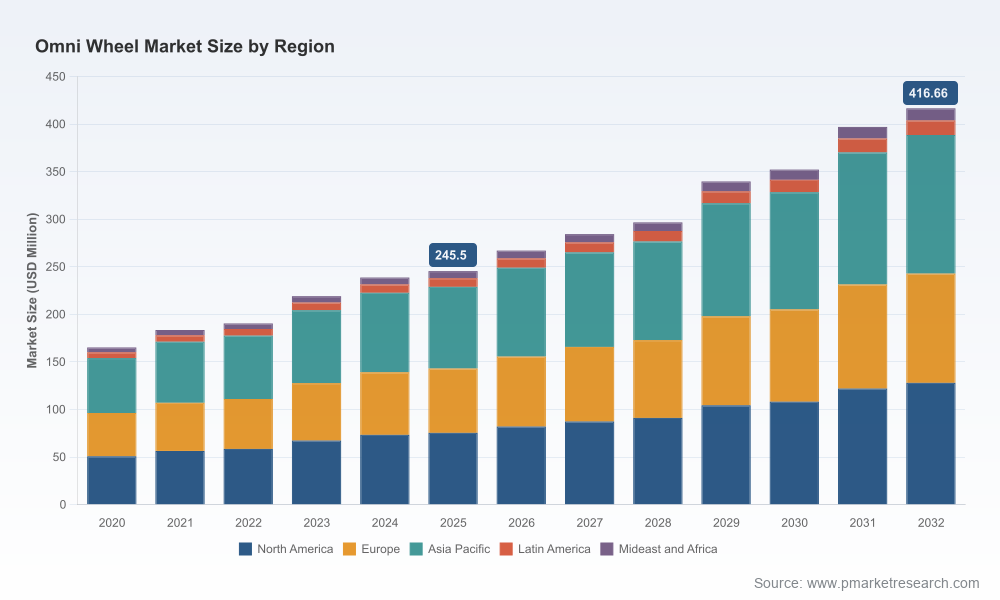

PW Consulting’s latest Omni Wheel Market report (base year 2025, forecast 2026–2032) delivers a concise, decision-focused preview for executives planning capital allocation, sourcing, product development, and M&A in 2026. The market is at an inflection point: measured expansion is supported by durable demand coming from robotics, automated material handling, and constrained-space logistics. Our high-level projections show the global omni wheel market reaching approximately USD 245.5 Million in 2025 and growing to an estimated USD 416.7 Million by 2032, a compound annual growth rate (CAGR) of roughly 7.85% over the forecast period. This brief outlines the strategic implications we expect to shape 2026 decision-making without disclosing our proprietary segmentation matrices — access to the full report provides the granular splits and scenario tables necessary for execution.

Omni Wheel Market

Two concurrent forces are accelerating demand: (1) the ongoing wave of warehouse and factory automation that requires omni-directional mobility in confined environments, and (2) the maturation of robotics platforms into mission-critical roles where maneuverability translates directly into throughput and safety gains. These structural drivers are reinforced by ergonomics and occupational-safety regulations that favor solutions enabling intuitive, low-effort handling.

Omni Wheel Market

Growth momentum — The market’s mid-single-digit to high-single-digit CAGR reflects both steady adoption in established industrial settings and increasing uptake in new verticals (medical devices, service robotics, and last-mile logistics).

Omni Wheel Market

Technology consolidation — Engineering polymers (notably polyoxymethylene via injection molding) dominate as the manufacturing substrate, balancing cost, impact resistance, and corrosion resistance. Material cost volatility is an immediate operational consideration for 2026 plans.

Supply-side stratification — Concentration metrics indicate a market where leading suppliers capture a meaningful share but where opportunities remain for specialized and regional players to compete on service and customization.

Raw material dynamics are more than a passthrough to price lists; they influence design, sourcing strategies, and inventory buffers. For example, recent POM pricing trends show observable increases in leading markets — a variable that has direct implications for gross margins and vendor negotiations. For procurement teams, the choice between long-term fixed-price contracts, indexed pass-throughs, and localized sourcing will be a primary determinant of 2026 cost control. Our full report models several procurement scenarios tied to raw-material trajectories and their impact on supplier ROIs.

The competitive map combines traditional component suppliers, dedicated omni wheel manufacturers, and distributors embedded in broader robotics portfolios. Key players we profile include (selection): OMNIA Wheel Ltd (Rotacaster Wheel Pty Ltd), WestCoast Products & Design LLC, VEX Robotics, Active Robots, TOK America, NEXUS Robot, and MATRIX ROBOTICS. Each brings distinct strengths that shape strategic options for buyers and competitors.

OMNIA Wheel Ltd — A leader in patented, full polymer injection-molded omni wheels, focused on high-performance, 360° mobility for industrial robotics and conveyance applications. Recent product updates and trade show engagements signal an emphasis on commercial expansion into sortation and conveying systems.

WestCoast Products & Design LLC — Operates as a key distributor within the U.S. robotics hardware ecosystem; their role exemplifies the importance of channel depth for scale and aftermarket support.

VEX Robotics and MATRIX ROBOTICS — Anchors in the educational and training segment; their presence supports a steady pipeline of awareness and adoption, which often precedes commercial deployment.

Active Robots, TOK America, NEXUS Robot — Regional and specialized suppliers supplying configurations and materials expertise; attractive partners for OEMs seeking customization or rapid prototyping.

Recent corporate activity reflects two priority behaviors: product-range refreshes aimed at industrial integration and trade-show-led market positioning to capture systems-level opportunities. These actions underscore a market where product differentiation and channel strategy are as important as unit economics.

Market concentration is meaningful but not prohibitive: the top-tier suppliers collectively hold a significant share of revenue, yet the mid-market remains accessible to focused entrants. This structural balance creates four primary opportunity windows for 2026:

Product differentiation through materials engineering (e.g., higher-performance polymer blends, wear coatings) and modular designs enabling quick swaps and maintenance.

Systems integration partnerships — bundling omni wheels with guided motion controls, encoders, and software to deliver higher total value to integrators and end-users.

Service and aftermarket models — spare-part subscriptions, predictive-wear analytics, and white-glove logistics support that increase lifetime value and margin resilience.

Geographic and vertical expansion — targeted push into medical/research and high-turn robotics deployments where safety and precision justify premium pricing.

Executives reading this brief should treat 2026 as a year to convert strategic intent into operational preparedness. Our advisory recommends five immediate priorities:

Lock in material-cost exposure: Decide on an approach (hedging, multi-sourcing, local inventory) informed by the price sensitivity of your product portfolio. Our models quantify the P&L impact of each option under conservative and aggressive price scenarios.

Pursue modular platforms: Invest in wheel architectures that simplify interchangeability and enable system-level upgrades without requalifying entire platforms.

Build channel anchor partnerships: For OEMs, secure distribution agreements or co-marketing with established regional channel partners to accelerate adoption in constrained-space logistics markets.

Differentiate through services: Design aftermarket and predictive-maintenance offerings that convert one-time sales into recurring revenue streams.

Prepare for consolidation: Identify acquisition targets or strategic alliances among specialized suppliers that can accelerate time-to-market for integrated solutions.

The full report is designed as an operational toolkit for 2026 planning. Highlights include:

Top-line forecast and sensitivity scenarios (2026–2032), with model access so buyers can re-run assumptions under custom inputs.

Supplier matrix and capability maps showing design, production, and channel strengths — useful for vendor selection and RFP design.

Commercial playbooks for market entry, pricing strategies, and service models tailored to OEMs, systems integrators, and distributors.

Procurement decision frameworks that translate raw-material trends into contract and inventory recommendations.

Case studies and use-cases illustrating ROI for omni wheel adoption across industrial automation, medical devices, and material handling.

Note: To preserve competitive confidentiality, our public synopsis omits the detailed segmentation tables (regional, type, and application splits) that underpin the report’s revenue and unit forecasts. These are included in the full report and interactive data appendices.

Q1–Q2: Conduct a supplier health assessment, focusing on capacity, lead times, and exposure to polymer sourcing constraints.

Q2–Q3: Pilot modular wheel assemblies in a controlled facility to measure maintenance windows and interchangeability benefits.

Q3–Q4: Negotiate distribution or co-development agreements with a targeted list of partners; prioritize contracts that include performance SLAs and inventory commitments.

Ongoing: Monitor POM pricing and available substitutes; update costing models monthly and re-assess pricing strategies on a rolling basis.

PW Consulting’s Omni Wheel Market report is intended to be a practical decision-support asset for 2026. The numbers we preview — including the market’s 2025 baseline and the 2026–2032 growth trajectory — represent the high-level contours executives need to justify investments. The full report contains the granular segmentation, supplier scorecards, scenario models, and negotiation playbooks that convert those contours into executable plans.

For manufacturing leaders, procurement heads, product executives, and private equity teams targeting industrial mobility, the 2026 window offers a chance to shape the next phase of market structure. PW Consulting stands ready to support bespoke analyses, integration roadmaps, and M&A diligence derived from the full omni wheel dataset.

For detailed analysis of this topic, please visit the official page:Omni Wheel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com