DGFT Registration Online in 2026 – Get Your IEC Without Delays

Other |

2026-04-30 06:12:53

PW Consulting’s latest market brief on the Plastic Roof Cement market synthesizes macro trends, competitive dynamics, raw-material risk factors, and pragmatic playbooks that senior executives and investors will need to navigate 2026. Anchored on a 2025 base year analysis and a 2026–2032 forecast horizon, the study combines quantitative forecasts with qualitative scenario planning to translate industry signals into executable choices. In short: this is a decision-focused primer designed to shorten your learning curve and sharpen choices—while preserving the proprietary, granular datasets on our portal for subscribers.

Plastic Roof Cement Market

Our market modelling shows the global Plastic Roof Cement market expanding from a 2025 base to a materially larger market by the end of the 2032 forecast horizon, driven by steady demand in repair and reroofing activity and selective product premiumization. On a compound annual basis, the market is projected to grow at approximately 4.85% over the 2026–2032 period, reflecting a balance between continued construction-led demand and margin pressure from raw-material volatility. Measured in USD (Million), the market displays clear expansion from 2025 through to 2032—evidence that the category remains strategically relevant for roofing manufacturers, distributors, and raw-material suppliers.

Plastic Roof Cement Market

Short-cycle decisions will drive medium-term positioning: 2026 is where procurement, pricing, and product-mix choices materially affect margin trajectories over the next five years. A one-year postponement in hedging or a delayed SKU rationalization can cascade into meaningful cost and service disadvantages.

Plastic Roof Cement Market

Regulatory alignment becomes non-negotiable: low-solvent and asbestos-free formulations compliant with ASTM D4586 Type I and relevant federal specifications are table stakes for market access and premium channel placement.

Volatility in feedstock markets (bitumen and allied inputs) introduces asymmetrical risk—winners will be those who pair operational hedging with adaptive pricing and product strategies.

Raw-material volatility. Bitumen and asphalt feedstocks have shown sharp, short-term price moves tied to crude markets and infrastructure demand. Recent market snapshots recorded double-digit month-on-month swings in key regions and elevated year-on-year price pressure—an input dynamic that compresses gross margins for producers without disciplined cost-recovery mechanisms.

Regulatory and product standards. Product compliance with low-solvent, asbestos-free standards (e.g., ASTM D4586 Type I and related federal specifications) is a gating factor for national procurement and many commercial specifications. Beyond compliance, there is a visible premium opportunity for formulations emphasizing lower VOCs, improved adhesion in wet conditions, and fiber reinforcement for crack resistance.

End-market mix. Residential reroofing and commercial/industrial maintenance remain core demand engines. The channel configuration—big-box retail, independent distributors, and professional contractors—shapes product packaging, SKU breadth, and after-sales services (warranty support, technical training).

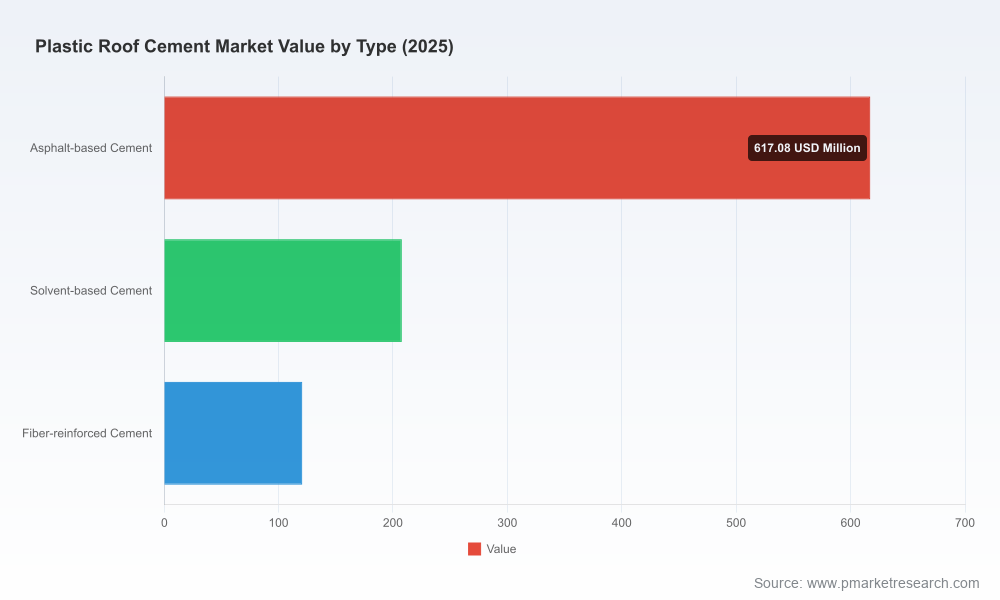

The category today spans traditional asphalt-based mastics, solvent-based formulations, and fiber-reinforced variants. Asphalt-based products continue to anchor volume because of cost and long-standing performance perceptions, while specialty formulations (solvent-reduced, fiber-reinforced) are carving out margin-accretive niches in professional channels. Our analysis emphasizes product architecture—formulation, delivery format (trowel-grade, cartridge, pail), seasonality (summer vs. winter grades), and specification compliance—as primary levers to defend or attack market positions.

The market exhibits moderate concentration, with the top-three and top-five firm groups reflecting material but not overwhelming market shares—creating room for regional champions and hard-niche specialists. Our competitive review synthesizes public product positioning and likely strategic intent across established manufacturers:

Henry Company (El Segundo, CA) — positions premium trowel-grade asphalt sealants toward professional roofers, emphasizing performance on flashings and penetrations. Their ASTM-compliant formulations and channel focus suggest a strategy centered on specification wins and professional loyalty.

GAF (Parsippany, NJ) — with general-purpose, asbestos-free cold-applied cements aimed at broad roof-system compatibility, GAF appears to defend mass channels while leveraging brand equity to support cross-sell across roofing accessories.

Karnak Corp. (Clark, NJ) — with differentiated season-specific grades and a heavy-consistency compound approach, Karnak targets durability-sensitive applications and professional reroof segments.

Gardner-Gibson (Tampa, FL) and Rust-Oleum (Vernon Hills, IL) — these players extend reach into all-weather and fibered-product niches, respectively, signaling strategies that mix retail channel penetration with product-innovation-led differentiation.

Polyglass U.S.A., PrimeSource/Grip-Rite, and TAMKO — each brings regional strengths, distribution networks, or product-specific value propositions (e.g., wet-or-dry adhesion, ASTM Type I compliance). These competitors often exploit channel specialization and local specification relationships.

Taken together, incumbents emphasize two strategic paths: (1) defend through channel entrenchment, specification compliance, and branded system selling; or (2) grow through formulation-led differentiation and premiumization (fiber reinforcement, low-VOC profiles, season-agnostic formulations). New entrants or regional players will need to choose between value-driven volume plays or technical niche plays to avoid direct head-to-head with entrenched incumbents.

Procurement and input risk management: implement dynamic hedging for bitumen exposure, layer fixed-price contracts with short-term spot protection, and regional sourcing diversity to dampen single-source risk.

Product portfolio optimization: rationalize SKUs to prioritize high-velocity, high-margin formulations; accelerate low-solvent and fiber-reinforced launches where specifications command price premiums; pilot cartridge and pail formats aligned to big-box and pro-contractor segments respectively.

Channel and go-to-market: bifurcate GTM strategies—mass retail requires packaging and price-point optimization; professional channels need training, specification support, and performance warranties. Invest in digital merchandising to reduce friction in contractor reorders and specification lookups.

Pricing and commercial safeguards: adopt formula-based escalators tied to agreed bitumen indices for large contracts; implement minimum advertised price (MAP) discipline in retail channels to protect margins and channel relationships.

M&A and partnerships: prioritize targets that add formulation capability (e.g., low-VOC chemistry), geographic reach in underpenetrated markets, or distribution density among pro contractors. Bolt-on acquisitions that provide complementary product lines (sealants, mastics) can increase share-of-wallet.

Operational resilience: digitize demand-sensing, reduce lead times, and create buffer capacity for seasonal surges; invest in small-batch production flexibility to accelerate response to feedstock price swings and bespoke contract requirements.

The full report is engineered for action. Highlights include:

Proprietary, year-by-year market sizing from the historical period through 2032 with base-year 2025 alignment and a transparent forecast methodology.

Scenario-driven margin models that quantify exposure to bitumen price swings and offer break-even analyses for common commercial hedging strategies.

Channel-level playbooks (big-box retail, distributor, pro-contractor) with SKU, packaging, and promotional recommendations tied to profitability targets.

Product benchmarking and specification matrix mapping ASTM compliance, VOC profiles, and delivery formats—designed to accelerate formulation roadmaps and claims substantiation.

Competitive intelligence dossier on leading suppliers and likely strategic moves, supported by a shortlist of acquisition targets and partnership archetypes.

An interactive Excel model for scenario planning and a set of templates for procurement contracting and price-escalation clauses.

To preserve the utility of these deliverables for paying clients, we present high-level conclusions in this release while keeping the granular segmentation tables, regional forecasts, and downloadable models behind our subscription gateway. This ensures decision-makers who need executable detail can access the full dataset and model logic directly.

For stakeholders in the Plastic Roof Cement value chain, 2026 is a year to operationalize resilience, codify specification-led differentiation, and execute disciplined commercial strategies. The market’s steady growth trajectory—underpinned by a mid-single-digit CAGR across the forecast window—creates room for both incumbents and focused challengers. However, feedstock volatility and regulatory dynamics will be the proximate determinants of profitability. Firms that proactively blend procurement sophistication, targeted product innovation, and channel-native commercial models will convert market expansion into sustainable margins.

PW Consulting’s full Plastic Roof Cement market study offers the data, modelling and playbooks needed to move from insight to action. For access to the complete datasets, scenario models, and acquisition shortlists referenced here, visit our report page to download the subscriber materials and interactive tools.

For detailed analysis of this topic, please visit the official page:Plastic Roof Cement Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com