Shadowless Lamps Market 2026: Strategic Priorities for Capitalizing on a Stable, Tech-Driven Upcycle

By PW Consulting — Senior Strategic Advisor & Chief Industry Analyst

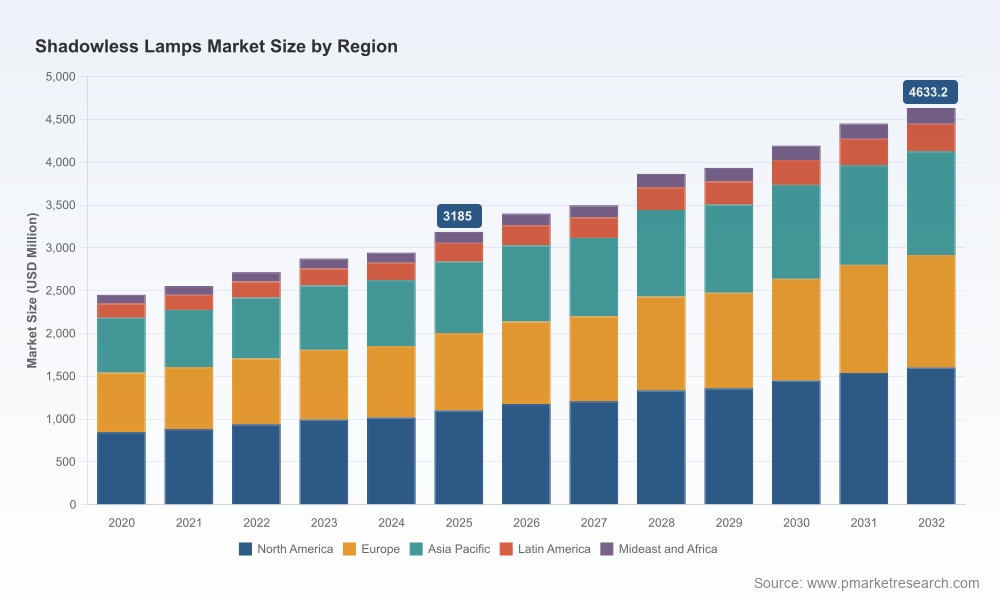

The shadowless lamps market is entering 2026 from a position of steady expansion and technological consolidation. PW Consulting’s latest market study — covering historical performance (2020–2025) and a forward-looking forecast to 2032 — identifies a resilient growth trajectory underpinned by LED adoption, OR modernization spending, and tighter integration of lighting systems into broader surgical workflows. Our base-year modelling (2025) and forecasted compound annual growth rate of 5.5% provide a robust frame for capital expenditure planning, vendor selection, and product strategy throughout 2026.

Shadowless Lamps Market

Why this report matters for 2026 decision-makers

- Actionable timing: The market is neither hypercyclical nor collapsing — it is expanding at a predictable pace. That predictability lets hospital networks, ambulatory surgery operators, and medical device OEMs calibrate procurement cycles and retrofit programmes rather than rush into sub-optimal purchases under false urgency.

- Technology convergence: Surgical lighting is migrating from a single-purpose capital good to a node in the hybrid-OR ecosystem. Procurement choices in 2026 will therefore have outsized downstream impacts on imaging, documentation, and interoperability budgets.

- Supplier negotiation leverage: With moderate concentration among leading vendors, buyers who enter 2026 armed with comparative lifecycle models, service-cost benchmarks, and upgrade-path clarity can materially improve terms without sacrificing performance.

Market trajectory — headline macro view

PW Consulting’s market model quantifies a multi-year expansion from the early 2020s into the next decade. After a consistent recovery during the historical window, the market reaches its 2025 base and continues to grow into the forecast period, reflecting both unit replacement cycles and rising average selling prices driven by feature-rich LED platforms. The projected CAGR of 5.5% underpins our scenarios for conservative, base, and accelerated adoption through 2032.

Shadowless Lamps Market

For executives planning 2026 budgets, the key implication is straightforward: plan for steady growth, prioritize interoperable investments, and avoid one-off procurement that could become stranded in the next upgrade cycle.

Shadowless Lamps Market

Dynamics shaping the opportunity

- LED-led product evolution: The ongoing shift to LED architectures remains the dominant product trend. LED systems deliver lower heat, longer life, and reduced energy draw — all features that are compelling in hospital CapEx planning focused on total cost of ownership (TCO).

- Integration into hybrid operating rooms: Manufacturers are increasingly shipping lighting platforms with integrated 4K in-light cameras, wireless connectivity, and OR-system APIs enabling real-time documentation, guided workflows, and telemedicine support.

- Regulatory and safety baseline: Surgical lighting systems are regulated as medical electrical equipment and require compliance with regionally relevant pathways such as the FDA 510(k) and IEC 60601 electrical safety standards. These compliance constraints shape time-to-market and upgrade timelines for new entrants and incumbent suppliers alike.

- CapEx and procurement behaviour: Hospital investment in OR infrastructure is being driven by rising surgical volumes and the push for minimally invasive procedures. Procurement teams are prioritizing energy efficiency, serviceability, and predictable upgrade paths when allocating 2026 budgets.

- Reimbursement context: Lighting systems are typically capitalized as OR infrastructure rather than reimbursed per procedure. The commercial case for a lighting upgrade therefore rests on throughput gains, staff efficiency, and risk reduction rather than direct CPT/DRG payments.

Competitive landscape — what matters for selection and partnership strategy

The industry footprint combines established global medical-device brands and regionally focused manufacturers. Market concentration metrics indicate that the top three companies account for a meaningful share but leave substantial room for differentiated competitors: CR3 at 38.5% and CR5 at 52.3% suggest a market that is neither a tight oligopoly nor fully fragmented. That structure creates strategic openings for both premium innovators and cost‑efficient challengers.

- Stryker (Kalamazoo, MI) — Continues to push platform differentiation. Recent launches have emphasized precision beam technologies and modes designed to maximize intraoperative visibility across diverse procedures. Their platform approach prioritizes upgradeability and service ecosystems.

- TRUMPF Medical (Hillrom/Baxter) — Focuses on multi-lens matrix optics and adaptive light management which support consistent, shadow-free fields in high-acuity settings.

- STERIS — Emphasizes integration readiness, 4K camera compatibility, and OR systems convergence, targeting healthcare systems investing in high-definition video and documentation workflows.

- Getinge (Maquet) and KLS Martin — Maintain strengths in high color-rendering and ergonomics, appealing to centers of excellence and specialty surgery markets.

- Dräger — Advanced LED optics and 3D shadow compensation have earned recent recognition; their Polaris family gained regional availability and design awards, signaling stronger competitive positioning in North America.

- Chinese manufacturers (e.g., Mindray, Heal Force, Shanghai Huifeng, Jiangsu Yigao) — Offer competitive price-performance propositions and are increasingly relevant in emerging markets and cost-conscious ambulatory settings; their role in global supply chains remains strategically important.

Recent product and recognition milestones — including publicized launches and award wins — are accelerating buyer attention toward newer, upgradeable lighting platforms that promise both immediate performance gains and mid-cycle software-enabled feature add-ons.

Practical, decision-ready insights for 2026

- Prioritize upgradeable platforms: Opt for platforms with modular optics and firmware-upgrade pathways. This minimizes capital obsolescence while preserving the option to add camera and connectivity features as budgets permit.

- Build TCO models that include service and spares: Warranty terms, field-service coverage, and spare-part logistics materially impact multi-year cost profiles. Our modelling shows that differences in service contracts can exceed vendor price differentials over a typical 7–10 year lifecycle.

- Demand systems-level interoperability: Procurement RFIs should require API/end-point availability for integration with OR video, EMR tagging, and OR scheduling systems to enable immediate and future efficiencies.

- Plan CapEx around clinical priorities: Align lighting upgrades with surgical portfolio expansion or specialty program launches to maximize marginal returns on throughput and outcomes.

- Use competitive tension strategically: With moderate market concentration, invite a cross-section of incumbents and regional suppliers to bid; include performance-based payment terms tied to uptime and light quality metrics.

- Mitigate supply-chain and regulatory timing risk: Validate vendors’ compliance pathways (510(k), IEC) and component sourcing plans to avoid unexpected approval delays or spare-part shortages.

- Consider lifecycle financing: Leasing and managed-service models can smooth budgetary impact and enable more frequent technology refreshes aligned with OR digitalization roadmaps.

Report contents — what PW Consulting delivers

PWC’s Shadowless Lamps Market report is structured to support both strategy teams and procurement practitioners. Key deliverables include:

- A validated market model spanning 2020–2032 with scenario testing around adoption rates, ASP trajectories, and service economics.

- Regulatory and standards roadmap (regional differences and approval timelines) to support go/no-go and launch planning.

- Detailed vendor profiles, technology capability matrices, and capability gaps for product-roadmap benchmarking.

- Commercial playbooks for hospitals and ambulatory centers outlining RFP templates, service-level benchmarks, and negotiation tactics.

- Investment and M&A screening tools highlighting value pools, margin profiles, and integration risks for strategic investors and OEMs.

In keeping with PW Consulting’s “preview-first” approach, this release highlights strategic implications and validated macro figures (including our CAGR and market trajectory). For commercial confidentiality and to preserve the investigative value of our segmentation model, granular regional splits, application-level revenue tables, and unit-level ASPs are reserved for the full report and interactive model available through PW Consulting’s portal.

Strategic next steps for 2026

- Healthcare providers: Convene clinical, biomedical engineering, and procurement stakeholders to build a two-year upgrade roadmap that sequences lighting, imaging, and OR digitalization investments together.

- OEMs and suppliers: Prioritize modularity, service proposition clarity, and documented interoperability to win the next wave of hospital tenders.

- Private equity and corporate development teams: Use our market-concentration and growth modelling to identify acquisition candidates that provide distribution lift, service-network density, or specific technology IP.

Conclusion — the strategic imperative

Shadowless lighting is no longer merely illumination; it is an enabling technology within modern surgical ecosystems. The 5.5% CAGR and steady market expansion projected by PW Consulting provide a planning envelope large enough to absorb innovation while small enough that strategic missteps (poor upgrade choices, weak service contracts, or lack of interoperability) will be costly. Organizations that align capital allocation with systems-level thinking — emphasizing upgradeability, service economics, and standards compliance — will convert steady market growth into competitive advantage in 2026 and beyond.

Request the full study

PW Consulting has prepared a comprehensive dataset, interactive model, and procurement playbook to support your 2026 strategy. Detailed regional and application splits, unit economics, and downloadable vendor scorecards are available in the full report. Visit our website to request access and discuss a tailored briefing with our senior analysts.

For detailed analysis of this topic, please visit the official page:Shadowless Lamps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com