Uncovering New Frontiers and Emerging User Experience Research Software Market Opportunities

Other |

2026-04-16 09:03:58

PW Consulting today publishes an executive briefing drawn from our new Intellectual Disabilities Service Market research report, designed specifically to inform C-suite and board-level decisions for 2026. The sector is at an inflection point: after steady expansion through the first half of this decade, market scale reached meaningful breadth by 2025 and is projected to continue growing through the end of our forecast window. Our base-year analysis (through 2025) and forward-looking modelling for 2026–2032 show a compound annual growth trajectory that underpins multiple strategic opportunities across services, payor engagement, and capability consolidation.

Intellectual Disabilities Service Market

Key macro takeaways you will find embedded in the report: the market has expanded substantially since 2020, rebounded after a short plateau, and is expected to grow at a mid-single-digit CAGR through 2032. That trajectory reinforces the business case for targeted investments in home- and community-based delivery models, workforce stabilization, and digital enablement to capture durable demand over the coming investment horizon.

Intellectual Disabilities Service Market

Resource allocation must be anticipatory, not reactive. The market’s scale and projected growth mean that incremental investments in operational resilience (workforce, data systems, and payer contracting) can compound into substantial competitive advantage. Organizations that prioritize scalable care models and payer-aligned outcomes measurement in 2026 will be better positioned for both organic growth and strategic transactions.

Intellectual Disabilities Service Market

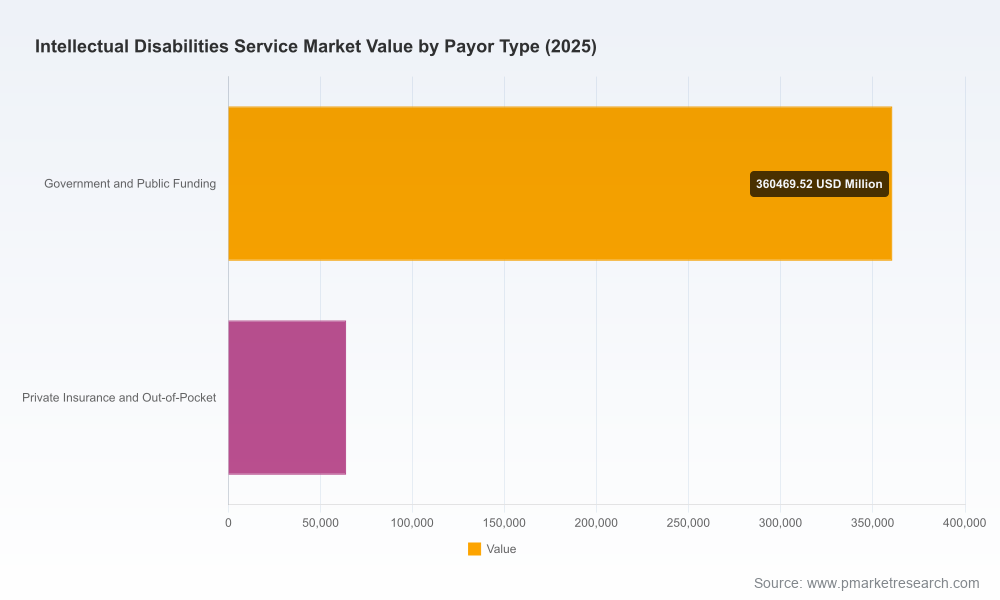

Payer strategy is central. State-level Medicaid programs and managed care implementations are increasingly shaping where value accrues. Recent policy and reimbursement shifts are accelerating the move toward outcomes- and performance-based contracting — transforming how providers price services, allocate clinical resources, and measure success. Practically, this means investment in outcomes analytics and flexible contracting capabilities will be a differentiator.

Service model evolution is a strategic lever. Demand is moving toward community-integrated, person-centered supports delivered across heterogeneous settings. Organizations that combine robust community-based services with scalable telehealth and remote-monitoring capabilities will be able to extend reach without linear increases in fixed costs.

Labor strategy is a make-or-break issue. Where states have invested in rate reforms, providers have successfully reduced vacancy and turnover among direct support professionals; conversely, chronic labor pressures remain the primary constraint on capacity and quality elsewhere. Workforce design — from targeted wage strategies to technology-enabled supervision — will determine 2026 capacity and service quality.

M&A and partnership remain active playbooks. The market dynamics favor both bolt-on acquisitions to extend geographic reach and capability deals that add specialized clinical or digital services. However, buyers should prioritize cultural fit, regulatory readiness, and payer relationships over headline scale alone.

Our research is intentionally operational. The full report is built as a playbook for executives and investors, not just as a market overview. Highlights include:

Decision-ready scenario planning — three forward-looking scenarios with trigger points and tactical responses to guide capital allocation across 12–24 month horizons.

Provider growth playbooks — step-by-step guidance on expanding home- and community-based services, integrating tele-rehabilitation and remote supports, and structuring blended payment arrangements with managed care plans and Medicaid authorities.

M&A due-diligence templates — operational checklists, regulatory risk matrices, staff retention plans, and a valuation sensitivity model that translates service-line performance into enterprise value.

Payer engagement toolkit — negotiation frameworks, outcome-linked KPI sets, and contract clauses that reflect current regulatory expectations and quality reporting requirements.

Workforce stabilization playbook — staffing models, compensation levers mapped to state rate structures, and technology adoption roadmaps to drive productivity without compromising quality.

Regulatory readiness checklists — including federal and state compliance touchpoints for residential and HCBS programs and practical steps to prepare for updated quality measurement and reporting regimes.

The market remains broadly fragmented, with national and regional nonprofit and for-profit providers operating across a mix of residential, community, vocational, and clinical service lines. Rather than presenting headline share tables, the report synthesizes competitive positioning across capability vectors — scale, payer relationships, clinical depth, digital enablement, and organizational integration.

Sevita: Has strengthened geographic continuity and operational scale through portfolio integration plays, emphasizing a person-centered model and a broad service footprint that enables cross-referral and care-continuity strategies.

BrightSpring Health Services: Active in portfolio reshaping and capability expansion; recent transactions reflect a strategy to consolidate community living services while enhancing pharmacy and complex-care capabilities to serve high-acuity populations.

Mosaic: Positions itself through personalized residential supports and 24-hour care offerings, leveraging deep engagement models to support long-term community inclusion objectives.

The Arc and large national networks: Play a critical advocacy and partnership role, scaling inclusive employment and community integration services through a mix of locally led operations and national programmatic initiatives.

Regional leaders (Keystone, Community Options, Devereux, Lifeworks, Easterseals, AbleLight, KenCrest, Bayada): These organizations sustain their competitive position through strong local payer relationships, specialized clinical programs, and high-touch community engagement models.

Recent market moves underscore themes that should inform 2026 strategy: capability consolidation to secure payer contracts and continuity of care; digital and tele-rehabilitation rollouts to increase access and efficiency; and strategic partnerships aimed at scaling supported employment and inclusive living models. Executives should expect continued deal activity that prioritizes operational synergy and payer alignment over simple footprint expansion.

Reimbursement and state program design are increasingly decisive. State-level Medicaid commitments to the intellectual and developmental disabilities population can run into the multi-billion-dollar range and often prioritize residential supports and day/employment services. These funding patterns create both opportunities and constraints for providers depending on local policy choices and waiver structures.

Regulatory expectations are tightening around safety and quality. Federal conditions of participation for institutional settings and updated HCBS quality measure sets require tangible investments in compliance, outcomes tracking, and reporting. Providers will need to operationalize quality measurement to maintain eligibility for certain reimbursement streams.

Labor market interventions show tangible benefit. Where jurisdictions have increased service rates tied to workforce investments, providers have seen declines in vacancy and turnover among direct support professionals; such examples offer operational roadmaps for workforce-focused investments that yield measurable capacity improvements.

Managed care expansions and program-specific waivers are reshaping service delivery. As states and plan sponsors move to broader managed care approaches for intellectual and developmental disability services, providers must be able to demonstrate outcomes, cost-effectiveness, and care-coordination capacity to succeed under new contracting models.

This report is built to be operationally actionable. For boards and executive teams, we recommend three immediate uses in 2026:

Run a 90-day payer-readiness sprint informed by the report’s contract templates and outcome measure sets to position for near-term managed care procurements.

Adopt the workforce stabilization playbook to align wage and recruitment investments with projected capacity needs and state rate environments.

Use the M&A due-diligence and valuation frameworks to prioritize targets that deliver both payer alignment and operational synergies, rather than purely geographic expansion.

PW Consulting’s full report delivers the granular datasets, segmented forecasts, and modelled scenarios that underpin the strategic guidance summarized here. To preserve the high-level decision focus of this release, we have deliberately withheld detailed segment and region-level tables from this briefing. Executives, investors, and policy teams seeking the complete data package — including regional and service-line breakdowns, detailed competitor benchmarking, and the downloadable toolkits mentioned above — can access the full report and supporting materials on our site.

For decision-makers preparing 2026 budgets and strategic plans, the window to convert market growth into sustainable, high-quality services is now. PW Consulting’s report equips you with the frameworks and practical tools to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Intellectual Disabilities Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com