Overhead Cranes Market Report and Competitive Landscape

Dance |

2026-07-01 13:19:22

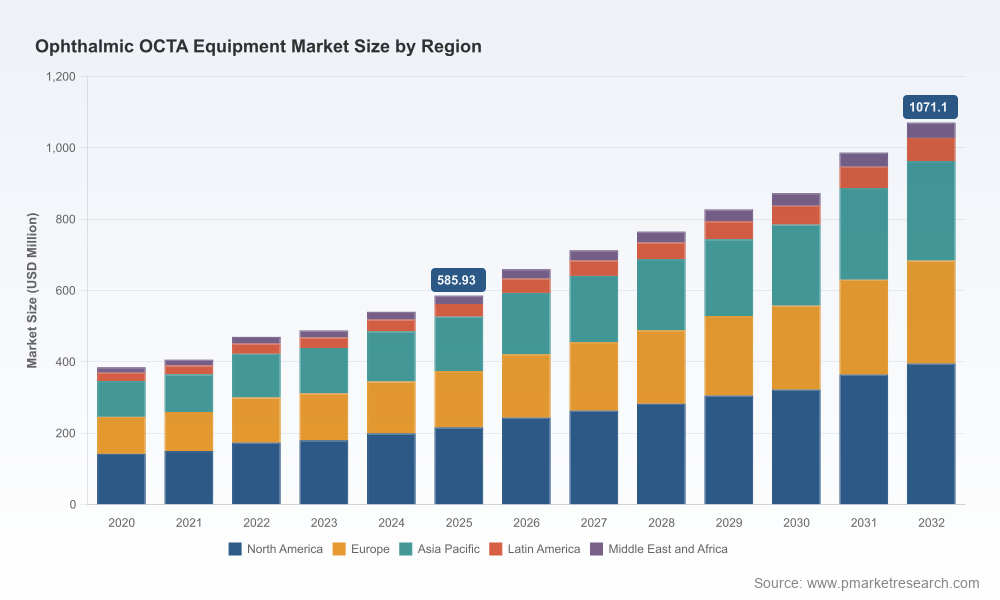

The Ophthalmic Optical Coherence Tomography Angiography (OCTA) equipment market is entering a phase of sustained commercialization and clinical maturation that will shape strategic choices in 2026. PW Consulting’s latest analysis uses 2025 as the base year and projects the market to expand at a compound annual growth rate (CAGR) of 9.0% across the 2026–2032 forecast window. In dollar terms the market moves from a base near USD 586 million in 2025 to roughly USD 660 million in 2026 and surpasses the USD 1 billion threshold by the end of the forecast period—an inflection that alters how vendors, hospital systems and investors should prioritize product development, go-to-market investment, and capital allocation.

Ophthalmic Octa Equipment Market

Reimbursement alignment: The introduction and adoption of CPT code 92137 for OCT angiography (effective January 1, 2025) materially changed the reimbursement landscape—with a 2025 MPFS national average reimbursement of approximately USD 56.93 versus USD 31.38 for the traditional OCT code. This differential changes commercial math for both equipment vendors and outpatient providers and accelerates discussions on billing workflows, clinical pathways, and diagnostic stewardship.

Ophthalmic Octa Equipment Market

Regulatory and product momentum: Over the last 24 months several vendors secured pivotal clearances and approvals that expand use cases (for example, supine and pediatric imaging) and facilitate regional commercialization. These regulatory milestones are not only product-competitive events but also timing triggers for customer procurement cycles and marketing pushes.

Ophthalmic Octa Equipment Market

Capital uncertainty inside provider systems: Hospitals report a median capital equipment budget in the vicinity of USD 15 million, while nearly 40% of executives cite cuts or deferrals in planned purchases. At the same time, hospital capex as a percentage of depreciation has risen—reflecting competing priorities as facilities manage aging infrastructure and technology renewal. The net effect is a shift toward creative procurement, lifecycle pricing and financing solutions in 2026.

Technology bifurcation and upgrade economics: Imaging platforms exhibit clear technological differentiation (high-speed spectral-domain implementations, swept-source deep-imaging systems, multimodal integrations). Vendors that present clear upgrade paths and modular architectures circumvent the “rip-and-replace” hurdle and gain traction in both clinics and hospital systems.

Concentration and competitive positioning: Market concentration metrics indicate a market dominated by a handful of global OEMs, creating a structure where three-to-five players exert significant influence on pricing, distribution and standards. This opens openings for agile challengers with niche clinical claims, lower cost structures, or disruptive commercial models.

Commercial levers: Reimbursement gains increase the procedure-level economics for OCTA, but procurement restraint at institutional buyers elevates the importance of total cost of ownership (TCO), uptime guarantees, remote service, and bundled offerings that include training and billing support.

Clinical workflow adoption: Adoption is being driven less by single-study superiority and more by integration into diagnostic pathways—screening, chronic disease surveillance, perioperative assessment—requiring vendors to invest in clinical evidence, AI-enabled analytics, and EMR interoperability.

Our vendor review covers established global players and several emerging entrants. Incumbents typically compete on platform breadth, clinical evidence and installed base service. Recent device-level differentiators include high acquisition speeds (some systems offer scanning rates measured in the 100k scans/sec range), wide-field angiography, deep-penetration swept-source architectures, and modular upgradeability that supports retina, optic nerve and anterior-segment angiography from a common hardware base.

Large OEMs emphasize platform ecosystems—bundling diagnostic modules, analytics suites and training to protect margins and customer relationships. They also leverage clinical partnerships and longitudinal datasets to embed their systems into care pathways.

Technology-focused specialists prioritize sensor performance, acquisition speed and algorithmic post-processing as their go-to-market differentiators. Regulatory clearances for expanded use (e.g., pediatric or supine imaging) have already shifted competitive dynamics by opening new clinical verticals.

Price and service challengers from lower-cost manufacturing geographies focus on compelling TCO propositions, rapid shipment cycles and local service partnerships to displace legacy incumbents in select markets and segments.

Notable recent developments that materially influence competitive calculus include CE marking of a swept-source platform in mid‑2025 enabling broader commercialization in Europe, and FDA 510(k) clearances in 2024 that expanded use-cases for some leading systems. These events accelerate procurement conversations and increase the importance of regulatory roadmaps in commercial planning.

Vendors (OEMs, service providers, and device-focused startups)

Prioritize modular product roadmaps that enable field upgrades. Given tight capital cycles, buyers prefer upgradeability over full replacement.

Build billing and coding enablement into commercial offers. The uptick in procedural reimbursement for OCTA means vendors that help customers capture revenue legally and efficiently remove a key adoption barrier.

Adopt flexible commercial models: subscription/managed services, outcomes-based contracts, and capital-light lease offers will win incremental deals where outright purchase is deferred.

Invest selectively in clinical evidence and AI-driven analytics that demonstrate differentiation in specific disease pathways (e.g., diabetic retinopathy surveillance, glaucoma progression).

Evaluate M&A or partnership plays. With a moderately concentrated market structure, bolt-on acquisitions can accelerate access to complementary modules, software analytics, or regional distribution networks.

Hospitals and large buyers

Build procurement scenarios that incorporate reimbursement upside, training costs, and service lifecycles into NPV calculations rather than looking solely at acquisition price.

Negotiate bundled deals that include data connectivity, long-term service level agreements, and revenue cycle support to mitigate operational risk.

Leverage pilot programs to test modular upgradeability and software analytics before enterprise rollouts, thereby reducing depreciation-schedule risk.

Investors and private equity

Prioritize assets with recurring revenue potential—service, consumables, software subscriptions—over pure hardware plays.

Assess regulatory pathway timelines and reimbursement sensitivity when modeling exit multiples and growth scenarios.

The full PW Consulting report goes beyond high-level narrative to provide actionable materials that decision-makers will use in 2026 planning cycles. Deliverables include an independently-verified market-sizing model with historical time series and forecast scenarios, a sensitivity matrix that quantifies reimbursement and capital-spend shocks, a strategic vendor scorecard that maps clinical claims to commercialization strength, and buyer decision templates (RFP checklists, TCO calculators, pilot evaluation protocols).

Interactive Excel models and slide decks that allow scenario-testing against changes in reimbursement, CAPEX availability and adoption velocity.

Detailed regulatory and reimbursement timelines tied to commercial launch playbooks and billing guidance.

Commercial readiness checklists covering sales compensation, service network design and training pathways to shorten time-to-revenue.

To preserve the tactical value of these deliverables, the report intentionally withholds granular regional/applicational splits from this public brief. Those segment-level allocations, price-benchmark sheets and an exhaustive vendor feature matrix are available only within the full report and the accompanying data pack.

Vendors: finalize modularization roadmaps and pilot one subscription-based commercial offer with a regional system buyer to validate elasticity of demand under constrained CAPEX.

Buyers: run a TCO comparison across vendors that includes billing uplift from OCTA-specific reimbursement and evaluate upgrade versus replacement economics.

Investors: stress-test leveraged growth cases against scenarios where capital budgets are deferred and where reimbursement adoption lags clinical adoption.

PW Consulting’s market analysis shows that OCTA is no longer an experimental add-on: it is becoming a core diagnostic modality with commercial levers that can be directly monetized. Firms that align product architecture, commercial models and regulatory strategy to the macro dynamics outlined here will be best positioned to convert market growth into durable share gains in 2026 and beyond.

For the full dataset, including the regional, technology and end-user splits, complete price benchmarking, and the interactive forecast model that supports board-level decision-making, download the PW Consulting Ophthalmic OCTA Equipment Market report. The full package contains the confidential spreadsheets and playbooks that executives and deal teams will rely on for procurement, R&D prioritization, and M&A workstreams in 2026.

For detailed analysis of this topic, please visit the official page:Ophthalmic Octa Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com