Rhinoplasty in Riyadh: Essential Information for First-Time Patients

Health |

2026-06-17 12:17:19

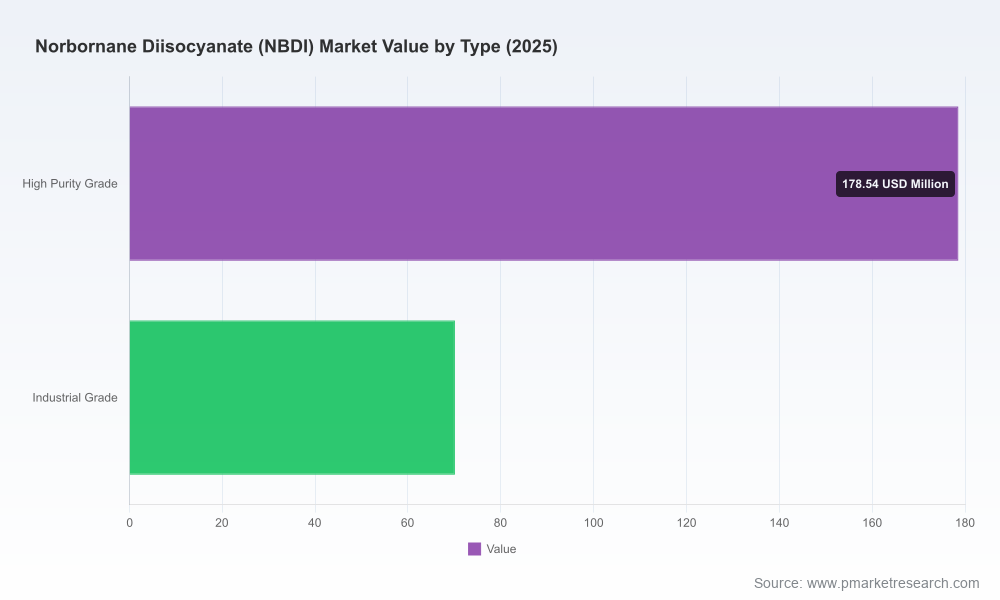

PW Consulting’s latest market intelligence on Norbornane Diisocyanate (NBDI) synthesizes technical, commercial, and regulatory inputs into an executable playbook for executives planning capital allocation, procurement, or product strategy in 2026. Our independent analysis tracks the market from 2020 through a 2025 base year and provides an evidence-based forecast covering 2026–2032. Key macro takeaways: the NBDI market is expected to expand at a compound annual growth rate (CAGR) of 5.24%, with total market value rising from USD 224.52 Million in 2023 to USD 248.66 Million in 2025, and a projected trajectory reaching USD 355.52 Million by 2032 (figures in USD Million).

Norbornane Diisocyanate (NBDI) Market

Timing: 2026 is the inflection window for many exposure-driven decisions — capacity investments, long-term off-take agreements, and entry/exit choices for specialty chem players. Our forecast and scenario frameworks convert near-term market signals into discrete decision milestones.

Norbornane Diisocyanate (NBDI) Market

Concentration: NBDI is a highly concentrated market (CR3 ~91.2%; CR5 ~96.5%), which magnifies the commercial impact of a single supplier’s capacity moves, technology shifts, or regulatory events. Buyers and investors must price in supplier concentration risk when structuring contracts or considering vertical integration.

Norbornane Diisocyanate (NBDI) Market

Complex upstream and compliance landscape: NBDI’s synthesis pathways and regulatory footprint create both technical barriers and compliance liabilities that materially affect cost-to-serve and go-to-market timing. These characteristics change the risk-return calculus for greenfield projects and for existing polyurethane value-chain participants.

The report combines primary interviews with leading producers, OEMs, formulators, and selected downstream customers, with proprietary supply-chain modeling and a granular bottom-up market sizing approach. We triangulated data from regulatory inventories and chemical reference sources to validate production feasibility and compliance status. Outputs include baseline and alternative scenarios, ready-to-use commercial models, and interactive decision tables designed to plug into capital planning cycles.

Timeframe: Historical analysis (2020–2025), base year 2025, forecast period 2026–2032.

Currency and unit convention: USD, revenue figures in USD Million to ensure comparability with corporate planning templates.

Evidence sources: Primary supplier interviews, trade flows, patent and regulatory inventories, Werner Blank’s chemical reference datasets for synthesis and toxicology context, and PW Consulting’s proprietary demand elasticities.

Demand drivers: NBDI’s value proposition rests on its rigid bicyclic architecture, which translates to performance advantages in specialty coatings, optical polymers, and certain elastomeric formulations. As higher-value end uses grow, demand for high-purity, product-consistent grades increases, supporting premium pricing and margin resilience.

Supply-side complexity: NBDI is synthesized from norbornene-based precursors through Diels–Alder type chemistry involving cyclopentadiene intermediates — routes that impose synthesis complexity, selectivity challenges, and intermediate handling constraints. These technical barriers reduce the number of feasible new entrants and compress the supply elasticity of the market.

Regulatory and safety profile: NBDI is catalogued in multiple national chemical inventories, and its toxicology (including documented oral LD50 and skin/eye irritation endpoints) requires structured handling, worker protection, and product stewardship programs. Regulatory listing does not equate to uniform acceptance across jurisdictions; compliance timelines and label requirements vary and can influence market access and formulation strategies.

Concentration-led volatility: The high market concentration means that capacity additions, unplanned outages, or strategic repositioning by incumbent suppliers can trigger pronounced short-term price and availability shifts. Buyers seeking continuity must consider multi-sourcing, medium-term contractual commitments, or backward integration.

Our competitive assessment synthesizes public company disclosures, supplier interviews, IP landscape reviews, and end-customer sentiment. Leading the commercial base is Mitsui Chemicals, Inc. (headquartered in Tokyo, Japan), positioned as the primary commercial producer and supplier of NBDI, marketed as a high-performance aliphatic diisocyanate with a distinctive rigid bicyclic structure. Mitsui’s scale, established customer relationships in optical and specialty coatings segments, and integrated quality control protocols confer first-mover advantages.

Strategic implications for market participants:

For buyers and formulators: Engage Mitsui and other incumbents early to negotiate supply agreements that embed quality, delivery, and price-adjustment mechanisms. Where continuity is critical, explore strategic inventories or consigned stock arrangements tied to performance KPIs.

For investors and potential entrants: Assess whether backing niche capacity — focused on high-purity grade production with tight QA — can overcome scale economies. Any new-build must account for feedstock sourcing complexity and regulatory readiness.

For incumbents and tier-1 chemical companies: Consider selective capacity debottlenecking, incremental downstream integration into urethane formulations, or licensing models to monetize IP while mitigating capital intensity.

This report is designed as a decision facilitator, not just an academic exercise. Deliverables include:

Commercial playbooks: Negotiation templates for offtake agreements, recommended contract tenors by use-case, and clauses to manage force majeure and regulatory change risk.

Scenario models: A set of interactive demand/supply scenarios (base, accelerated-adoption, regulatory-shock, and feedstock-disruption) calibrated to the 2026 planning horizon, with clear trigger points and recommended tactical responses.

Supply-chain mapping: Tiered supplier maps showing where technical bottlenecks are most likely to emerge (feedstock synthesis, purification, and QC testing), and mitigation options such as toll manufacture or dual-sourcing strategies.

Regulatory playbook: Practical compliance checklists and a jurisdictional matrix for registration/status and stewardship requirements, with steps to accelerate market access for new grades.

Commercial due diligence templates: For private equity and corporate M&A teams evaluating targets or strategic partnerships in the NBDI value chain.

Technology and IP snapshot: Patent landscaping and technological risk assessment to inform R&D prioritization and defensive IP strategies.

Lock in mid-term supply where product specifications are mission-critical. Given the market’s concentration and the projected CAGR of 5.24%, securements that align supply certainty with demand ramp profiles reduce P&L volatility.

Differentiate on formulation and service rather than raw NBDI arbitrage. End-users that can co-develop formulations capturing NBDI’s performance premium will extract higher total-margin capture than commodity resale.

Invest in regulatory and product stewardship capabilities. Compliance readiness shortens time-to-market for new grades and reduces the risk of sudden market access constraints.

Stress-test capex decisions against upstream feedstock risk. The norbornene precursor supply chain is specialized; contingency planning for feedstock interruption should be priced into NPV models and contractual clauses.

Explore partnership structures with primary producers. For buyers seeking prioritized access, joint development, co-location, or financial participation in processing capacity can create defensible supply positions without full ownership.

Feedstock scarcity: Watch shipment lead-times and crude intermediate price inflation as early indicators of tightening availability.

Regulatory shifts: Changes in labeling, exposure limits, or inventory statuses in key markets can materially affect formulations and logistics.

Supplier strategic shifts: Public signals of capacity rationalization, M&A activity among incumbents, or strategic shifts into downstream adhesives/coatings should trigger immediate contract and risk re-evaluation.

Technological substitution: Breakthroughs in alternative chemistries that emulate NBDI’s performance at lower cost or with simplified supply chains would alter the competitive dynamics and growth assumptions.

For C-suite leaders and strategy teams, the report functions as a decision-support toolkit. Use the scenario models to stress-test your 2026 capex and procurement plans, apply the negotiation templates during supplier discussions, and employ the regulatory matrix to sequence registrations and market entries.

For private equity and corporate development teams, the commercial diligence modules and valuation sensitivity analyses reduce execution risk by converting qualitative supplier concentration and synthesis complexity into quantifiable valuation levers.

The public briefing above outlines the strategic contours and high-confidence macro projections for NBDI through 2032. To execute on the recommendations — including access to the granular regional, grade, and application segmentation data, supplier-by-supplier benchmarking, and the interactive Excel-based scenario models — please visit our report landing page to obtain the full dataset and supporting annexes. The full report contains the detailed split tables, capacity maps, and supplier scorecards intentionally omitted here to preserve the substantive value of the source package.

PW Consulting’s NBDI study is built to be immediately operational for 2026 planning cycles. If you would like a bespoke briefing workshop that applies the scenarios to your company’s balance sheet and commercial pipeline, our consulting team is available to run an executive session and deliver customized recommendations within a 4–6 week engagement.

For detailed analysis of this topic, please visit the official page:Norbornane Diisocyanate (NBDI) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com