Comprehending the NFL refreshing roster legal guidelines starting inside 2020

Health |

2026-05-25 09:17:41

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a forward-looking synthesis from our latest Ballast Bag Market report — an operationally focused briefing designed to inform boardroom decisions in 2026. This article summarizes the market trajectory, competitive dynamics, regulatory and materials pressures, and the tactical playbook executives need to move from analysis to action. The full report contains the proprietary segmentation models, downloadable financial templates, and deal-ready M&A scenarios; this preview intentionally demonstrates the analytical depth while omitting the granular segment-by-segment figures you’ll find in the source document.

Ballast Bag Market

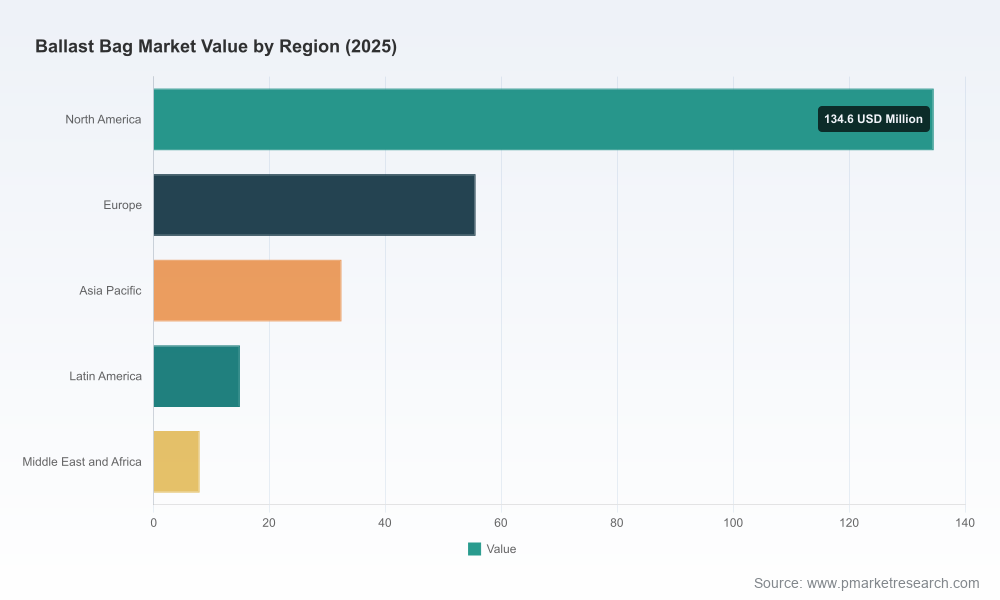

Between PW Consulting’s historical window (2020–2025) and the forecast horizon (2026–2032), the ballast bag market has demonstrated resilient, above-market growth underpinned by both recreational and industrial demand vectors. The market grew from a mid-hundreds USD Million base in 2020 to roughly USD 245.5 Million in the 2025 base year, and our projections apply a compound annual growth rate (CAGR) of 6.5% across the 2026–2032 forecast period. By 2032 the market size is projected to be meaningfully larger than the 2025 base — a trajectory that creates concrete opportunity windows for product innovation, channel expansion and consolidation plays.

Ballast Bag Market

Two observations are critical for strategic planning in 2026: first, growth is not uniform — the market comprises distinct use-cases (recreational wake enhancement, industrial/marine load testing, aviation/aerospace testing) that require differentiated product, certification and go-to-market approaches. Second, the market’s competitive intensity is moderate-to-high: the three largest firms account for a sizable share of revenue, and the top five collectively command a clear majority. This concentration level creates both barriers to entry in certain subsegments and attractive consolidation targets for acquirers seeking scale quickly.

Ballast Bag Market

Our analysis highlights a mix of specialists focused on recreational boating and wakesports, high-volume industrial producers for marine load testing, and regional players that serve adjacent niche markets. Key industry participants include:

From an M&A perspective, the landscape suggests two primary playbooks for 2026:

Material innovation and supply chain resilience are decisive. Ballast products split operationally between flexible water-filled systems (heavy-duty PVC-coated fabrics and welded constructions), shot-filled solutions (polypropylene and Cordura shells with metal shot), and engineered lift/lift-bag systems for heavy testing. Procurement teams must evaluate supplier concentration, lead times for polymer resins, and secondary processing capabilities (e.g., welding, seam reinforcement, custom tooling).

Standards compliance is non-negotiable in industrial and civil applications. IMCA D016 and LEEA 051 continue to be reference points for underwater and proof-load testing respectively; purchasers will increasingly require traceable test certificates and third-party verification. At the same time, regulatory activity in leisure boating is heating up: for example, legislative initiatives targeting wake-enhancing modifications are emerging in several jurisdictions. Wisconsin Assembly Bill 1045 (2025) represents an early signal that state-level rules addressing ballast systems for wake enhancement may proliferate. For OEMs and aftermarket vendors, early engagement in regulatory dialogue and proactive safety documentation convert into faster approvals and reduced liability exposure.

Our full study provides a nuanced segmentation across product types, applications and regions, and couples that taxonomy with cost structures, margin curves and channel economics for each node. While this briefing intentionally omits the granular split figures, the report includes:

Executives should treat the coming year as a window to build capability rather than merely chase short-term volume. Practical steps we advise in 2026:

Our report blends primary interviews, supplier factory audits, and a bottom-up market model. It translates raw market growth into executive-grade decision levers — scenario models, acquisition scorecards, channel economics and procurement playbooks. For boards, the work provides a short list of portfolio moves with quantified returns under each macro scenario. For corporate development teams, it strips the noise from price forecasts and materials risk so that deal valuation is rooted in operational reality, not aspirational synergy.

The ballast bag market offers a clear growth runway, but the path to profitable scale is complex: material constraints, certification requirements and an evolving regulatory landscape require deliberate investment choices in 2026. PW Consulting’s Ballast Bag Market report packages the analytics and executable playbooks you need to make those choices with confidence.

To access the full segmentation data, downloadable financial models, company scorecards and our prioritized M&A target list, visit the report landing page. The online deliverable contains the confidential annexes and interactive tools required to convert insight into a transaction or operational plan.

For detailed analysis of this topic, please visit the official page:Ballast Bag Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com