Pet Food Market Trends in Freeze-Dried and Raw Food Products

Food |

2026-03-30 08:22:44

PW Consulting’s latest market study on Magnetic Clamping Technology provides a focused, decision-ready intelligence package for executives preparing budgets, product roadmaps, procurement strategies, and M&A activity in 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the report quantifies the market’s size and trajectory (market value at USD 585.5 Million in the 2025 base year, projected to approach roughly USD 907 Million by 2032 at a 6.45% compound annual growth rate) while delivering the practical tools that senior leaders need to convert that macro view into executable plans.

Magnetic Clamping Technology Market

Convergence of automation and precision machining: Magnetic clamping systems increasingly serve as an enabler for fast tool change, deformation-free workholding, and five-sided machining access — capabilities that directly accelerate cycle-time reduction and reduce scrap in modern CNC environments.

Magnetic Clamping Technology Market

Material and cost volatility: High-performance magnets rely on neodymium-rich rare earth inputs. In 2026 neodymium oxide traded well above historical norms (market sources reported prices in excess of USD 112,000 per tonne), introducing procurement and margin pressures that ripple across OEMs and component manufacturers.

Magnetic Clamping Technology Market

Standards and safety governance: New and clarified regulations such as ISO 23582-1:2023 establish essential safety and integration requirements for magnetic clamping systems used on plastics and rubber machines. Compliance will be a gating factor for both product acceptance and liability management.

Industry structure and consolidation signals: The market shows a moderate concentration profile (top-three players capture roughly 42% of reported market revenue and the top-five about 58%), which creates windows for targeted partnerships, niche specialization, and selective acquisition depending on strategic intent.

Robust market sizing and top-line outlook — independent projections through 2032, including sensitivity runs reflecting raw material and macroeconomic scenarios.

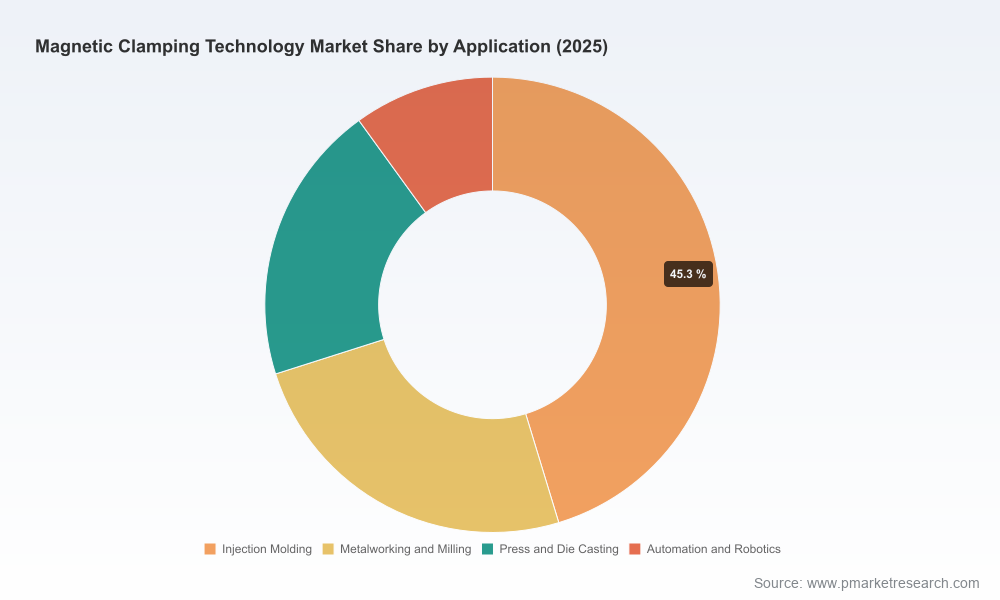

Demand-driver analysis — mapping use-cases (injection molding, metalworking, press/die applications, automation integrations) to technology choices and total cost of ownership (TCO) trade-offs.

Technology roadmaps and deployment playbooks — comparison of electro-permanent, permanent, and electromagnetic approaches, with guidance on selection by cycle-time, energy profile, maintenance cadence, and safety requirements.

Supply-chain heat map and input-cost sensitivity — forward-looking scenario modelling for rare-earth inputs, contract levers for alloy buyers, and recommended hedging/tactical sourcing approaches for 2026 procurement cycles.

Regulatory and compliance checklist — ISO 23582-1:2023 implications, cleanroom interface considerations for mold clamping, and integration checklists for safety managers.

Competitive benchmarking and capability matrix — feature/function, service footprint, certification profile, and product differentiators for major suppliers (executive-level summaries with supplier risk scores).

Go-to-market and commercialization playbooks — channel strategies, retrofit pathways, and OEM co-development models calibrated to reduce payback timelines.

M&A and partnership screening toolkit — target filters, valuation multiples observed in analogous electromechanical niches, and integration planning templates for bolt-on and platform deals.

Procurement leaders should rebase sourcing strategies around rare-earth cost volatility. Short-term fixed-price contracts may protect margins, but mid-term strategies should include dual-sourcing, strategic inventory, and engineering substitution where feasible.

Product leaders must prioritize electro-permanent and hybrid approaches where quick switching, low steady-state energy draw, and cleanroom compatibility are differentiators. Systems that draw power only during switching offer a compelling TCO profile for mold-clamping and high-throughput molding cells.

Manufacturing and operations teams should accelerate pilot deployments of magnetic workholding in cells aiming to reduce setup time and vibration; measurable KPIs should include set-up minutes per part, reject rate, and spindle load variance.

Investors and M&A teams should look for targets that combine proprietary electro-permanent IP, strong customization services, and access to vertical channels (e.g., molding machine OEMs or Tier-1 automotive suppliers) to capture integration value.

The market’s competitive topology is a blend of legacy mechanical specialists, magnetic-focused innovators, and regional manufacturers serving niche applications. Several players illustrate the variety of strategic approaches in 2026:

SCHUNK GmbH & Co. KG (Lauffen am Neckar, Germany) emphasizes high-precision MAGNOS permanent magnetic clamping for five-sided machining, focusing on uniform clamping forces to reduce vibration and enable near-zero deformation workholding — a classic product-led differentiation strategy aimed at high-value machining centers.

Stäubli International AG (Pfäffikon, Switzerland) has developed magnetic quick-change systems for injection molding that combine active safety, clamping-force feedback, and compatibility with small-tonnage presses — signaling a platform-plus-service approach tailored to the plastics industry.

AMF and Roemheld’s magnetic clamping offerings continue to integrate with zero-point systems and partner ecosystems, reflecting a move toward modular automation interoperability. AMF’s 2026 trade-show presence underscores market-facing commercialization and systems integration ambitions.

Mag-Autoblok Tecnomagnete’s recent hybrid chuck innovations and partnerships indicate activity in combining mechanical and magnetic clamping strengths — a useful hedging strategy where customers require both centering and magnetic holding capabilities.

Regional specialists and service-centric firms (examples include Earth-Chain, WALMAG, Eclipse Magnetics, and Braillon) continue to compete on customization, repair, and rental services — an attractive margin pool for firms that can deliver uptime and localized support.

These strategic postures align with the market’s concentration profile: leaders deploy global channel reach and product breadth while specialised players compete on local service and tailored engineering. Executives should interpret product releases and trade-show activity as real-time signals for where adoption momentum is building.

Raw material shocks: Accelerated price moves in neodymium or supply restrictions would compress margins and could delay new projects unless passed through price adjustments or mitigated by material substitution.

Regulatory tightening: Extensions to ISO or safety regimes adding validation or documentation requirements could lengthen time-to-market for new systems, particularly in plastics and medical-device applications.

Technology substitution: Alternative clamping paradigms (e.g., advanced vacuum fixturing with improved composite tooling) could disrupt segments where magnetic clamping currently holds advantages.

Consolidation dynamics: A wave of M&A concentrating more share in leading platforms would reshape buyer power and pricing; conversely, open ecosystems with standardized interfaces could democratize access and accelerate adoption.

Procurement: Run the report’s cost-sensitivity models against supplier bids to develop defensible hedging strategies for 12–36 month sourcing cycles.

R&D and product planning: Map product roadmaps to the technology and safety checklists in the report; prioritize features that shorten OEM qualification cycles and enable retrofitability.

Commercial strategy: Use the go-to-market playbooks to pilot value-based pricing in target verticals and quantify payback windows for end customers to accelerate adoption.

M&A & corporate development: Apply the screening toolkit to prioritize targets by IP defensibility, service footprint, and channel synergy in core geographies.

Operations: Implement the recommended KPI set for pilot cells to validate TCO claims and to produce internal case studies for wider rollouts.

This executive brief is a focused preview of the full PW Consulting study. The full report contains detailed scenario models, granular segmentation tables, supplier scorecards, and downloadable tools that allow teams to run tailored sensitivity analyses against their own assumptions. We deliberately limit the disclosure here to establish the strategic narrative and to protect the actionable microdata that drive confident 2026 decision-making. For organisations seeking to align procurement cycles, product development, or M&A pipelines to the magnetic clamping market’s trajectory, the full intelligence package is designed as a plug-and-play foundation.

To access the report’s full datasets, interactive models, and supplier benchmarking appendices, please visit PW Consulting’s market research portal or contact your PW Consulting advisor for a briefing tailored to your industry segment and strategic priorities.

For detailed analysis of this topic, please visit the official page:Magnetic Clamping Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com