Why Chrome Hearts Is the Ultimate Luxury Streetwear Brand

Shopping |

2026-06-16 07:12:43

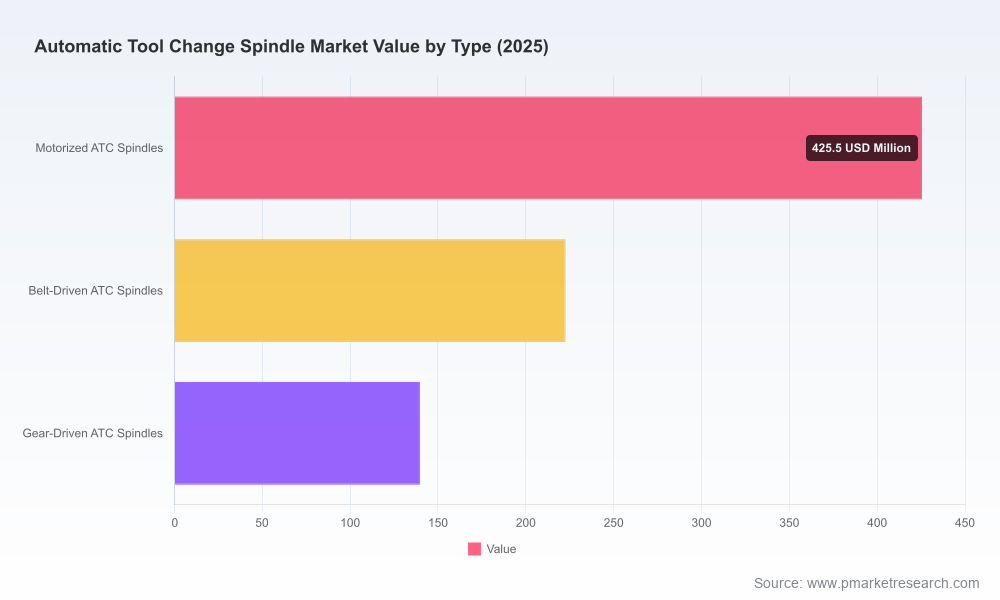

PW Consulting’s latest market study on Automatic Tool Change (ATC) spindles synthesizes the commercial, technological, and operational signals that will shape supplier selection, capital allocation, and factory transformation decisions in 2026. The report frames a market that has expanded steadily—from a market size of USD 595.4 Million in 2020 to USD 787.8 Million in 2025—and that is expected to grow to approximately USD 1,130.8 Million by 2032. Our forecast period (2026–2032) assumes a compound annual growth rate (CAGR) of 5.31%, a pace that underscores sustained, pragmatic adoption rather than speculative hype. This briefing highlights why that macro trajectory matters to C‑suite and plant leaders and what practical levers the full report equips you with to convert insight into measurable advantage.

Automatic Tool Change Spindle Market

Capital allocation discipline: With moderate, predictable market growth, procurement teams must prioritize investments that shorten payback and enable phased rollouts rather than all‑in platform bets. The report provides TCO and NPV templates tailored to ATC spindle procurements.

Automatic Tool Change Spindle Market

Supply‑chain preparedness: The study surfaces where supply pressures and input cost volatility will have the biggest impact on lead times and margins—critical for procurement and finance teams forecasting 2026 spend.

Automatic Tool Change Spindle Market

Operational readiness: For operations and engineering leaders, the report moves beyond vendor brochures to provide integration checklists, automation compatibility matrices, and practical retrofit pathways suited for incremental modernization and lights‑out ambitions.

Risk‑calibrated scenarios: Rather than a single forecast, we present scenario planning that stresses suppliers, materials, and adoption curves—enabling contingency budgeting and staged rollouts in 2026.

Automation as a labor substitute and productivity lever: Skilled labor shortages in CNC machining continue to push adoption of ATC spindles and complementary robotics. Firms pursuing lights‑out operations will prioritize reliability, serviceability, and digital diagnostics when specifying spindles.

Input‑cost pressure and component constraints: Precision bearings remain a strategic input—an adjacent market that was valued in the tens of billions in 2025 and is projected to grow further in 2026. Recent raw‑material and component cost increases—estimated to have driven production cost rises on the order of the high‑teens percentage for some manufacturers—favor operators that can secure long‑term supply agreements or invest in higher‑availability designs.

Technology differentiation: The field is evolving along multiple technical vectors—high‑speed air‑bearing spindles, motorized electrospindles, modular designs for power density, and retrofit mounts that reduce integration complexity. Each technology tradeoff (speed vs. torque, cooling approach, tool‑holding standard, maintenance model) materially affects application economics.

Concentration and competitive dynamics: The market exhibits moderate consolidation. The top three suppliers account for a significant single‑digit to low‑mid double‑digit share (CR3 ~31.45%), and the top five reach a larger slice (CR5 ~42.8%). This structure creates an environment where both established OEMs and nimble specialists can win—depending on execution of distribution, service, and vertical specialization.

GMN USA (subsidiary of GMN Germany, https://gmnusa.com) — strong position in high‑speed CNC spindles with ATC systems and broad service capabilities. Strategic implication: prioritizes customers needing high RPM performance and OEM‑grade lifecycle support; worth engaging on long‑term service contracts and technical co‑development.

Celera Motion (Novanta) (https://www.celeramotion.com) — leader in precision air‑bearing spindles with ultra‑high‑speed units. Strategic implication: appeals to manufacturers of composites and non‑ferrous parts where surface finish and micro‑precision matter; evaluate for niche, high‑value use cases.

Teknomotor (https://www.teknomotor.com) — European player focused on electrospindles for wood and aluminum machining, with quick tool‑change support. Strategic implication: strong candidate for woodworking and aluminum fabrication segments seeking integrated electrospindle solutions.

Jingjiangcity Jianken High‑Speed Electricmotor Co., Ltd. (https://www.jian-ken.com) — producer of pneumatic ATC spindle motors with competitive pricing and air‑cooled architectures. Strategic implication: interesting for volume‑sensitive projects and aftermarket retrofits where capex discipline is primary.

CNC Depot (https://www.cncdepot.net) — US manufacturer with a focus on the domestic small‑to‑mid power spindle market for routing and milling. Strategic implication: proximity, lead‑time and retrofit support make them attractive to North American integrators.

SPINOGY (https://www.spinogy.de) — German firm with modular, high‑frequency motor spindles supporting automatic changes. Strategic implication: design modularity accelerates customization and maintenance windows in advanced production cells.

Air Turbine Tools (https://www.airturbinetools.com) — specializes in high‑speed finishing spindles with retrofit mounts. Strategic implication: a practical option for finishing lines and detail work where ease of retrofit reduces conversion cost.

PwnCNC (https://pwncnc.com) and RapidChange ATC (https://rapidchangeatc.com) — smaller, system‑centric players focused on hobbyist to professional and affordable ATC systems. Strategic implication: valuable for pilot projects, proof‑of‑concepts, and cost‑sensitive upgrades before enterprise rollouts.

Recent vendor activity underscores the market’s practical orientation: GMN USA published updated guidance on selection and maintenance of ATC spindles in January 2026, while ecosystem contributors released integration overviews in late 2025—signals that suppliers are moving from product marketing toward enabling operational adoption. Executives should read these publications as supplier playbooks that can shorten internal learning curves, but the report cautions buyers to verify claims with field trials and standardized acceptance tests.

Clear, audit‑grade market sizing and growth context (2020–2025 historical analysis and 2026–2032 forecast), including sensitivity to input costs and adoption rates to inform 2026 budget cycles.

Decision frameworks and procurement scorecards: standardized criteria to evaluate suppliers across reliability, service footprint, spare parts economics, upgrade path, and digital interfaces.

Integration playbooks and retrofit checklists: step‑by‑step guidance for mechanical, electrical and control integration with common CNC platforms and robotic cells—minimizing downtime during deployment.

Financial tools: TCO models, break‑even and payback calculators, and capex vs. opex comparators customized to ATC spindle configurations and utilization profiles.

Risk and mitigation matrices: supplier concentration risk, raw material exposure, and labor dependencies, with prioritized mitigation actions for each risk vector.

Case studies and vendor negotiation playbooks: anonymized program examples that show procurement strategies that reduced total cost by optimizing maintenance contracts, buyback terms, and spare‑parts pooling.

90 days — De‑risk: run supplier pre‑qualification using our procurement scorecard, secure critical long‑lead components where appropriate, and scope a pilot line that validates integration assumptions.

180 days — Scale: convert validated pilots into phased rollouts targeting high ROI cells, lock in service level agreements with key suppliers, and implement predictive maintenance sensors on pilot spindles.

365 days — Embed: shift to capacity planning that incorporates ATC spindle uptimes, update workforce plans to prioritize automation supervision skills, and complete supplier consolidation or strategic partnerships as indicated by the supplier performance dashboards in our report.

Executive takeaway: the ATC spindle market presents a low‑to‑medium growth environment where durable competitive advantage arises from execution—supplier selection, integration speed, and maintenance strategy—not from speculative technology bets. Our analysis shows a market large enough to support specialized vendors and scale players alike; the winning companies in 2026 will be those that translate product capability into predictable, measurable factory throughput improvements while managing component risk and lifecycle costs.

The full PW Consulting report contains the segmented dataset, granular vendor rankings, downloadable tools (scorecards, TCO models, integration checklists) and the appendices that rigorously document our assumptions and scenario methodology. To access the full intelligence—required for procurement approvals, capex committees and detailed supplier negotiations—please visit the report page or contact your PW Consulting account representative to request the authorized dataset and executive briefing materials.

For detailed analysis of this topic, please visit the official page:Automatic Tool Change Spindle Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com