Medical Aesthetic Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-08 10:07:09

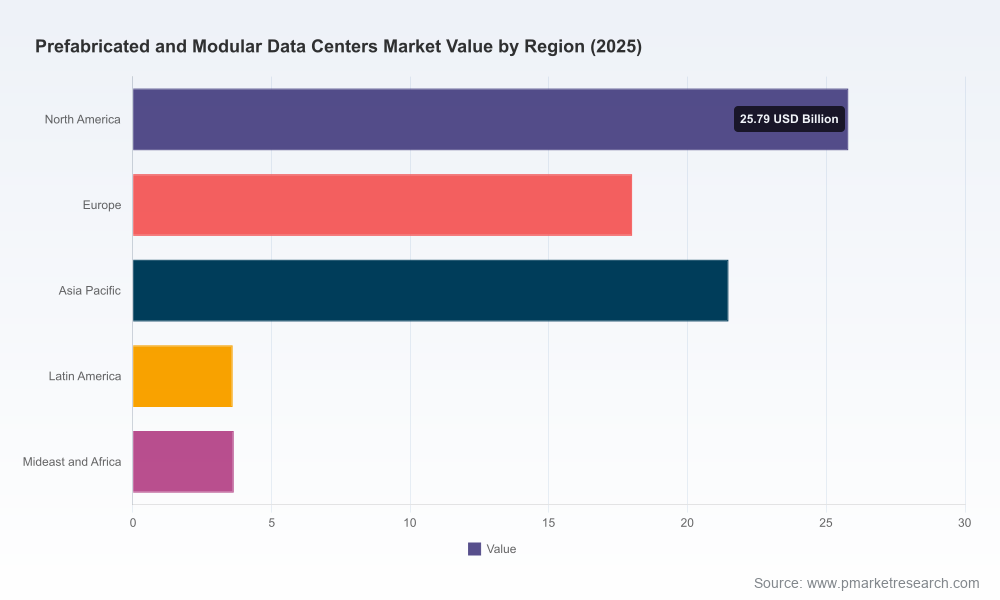

PW Consulting’s latest market study on Prefabricated and Modular Data Centers (base year 2025) arrives at a pivotal moment for infrastructure leaders and C-suite executives. The market that generated roughly USD 72.5 Billion in 2025 is on a clear, rapid growth trajectory — our modeling shows a sustained compound annual growth rate of 16.45% into the next decade, with the industry scaling materially by 2032. For organizations that must balance latency, sustainability, capital discipline, and regulatory risk, the choices made in 2026 will materially shape total cost of ownership (TCO), speed-to-market, and long-term flexibility.

Prefabricated And Modular Data Centers Market

Acceleration of AI and high-density computing: Persistent demand for high-performance workloads is driving a structural shift toward factory-integrated podules and liquid-cooled architectures. Suppliers and operators are rapidly aligning product roadmaps around dense, power-intensive deployments — a change that favors modularization as a risk-mitigation and speed-to-scale mechanism.

Prefabricated And Modular Data Centers Market

Regulatory and energy-price pressure: In 2026, more than two dozen U.S. states are moving to ensure data centers finance their incremental grid impacts and disclose energy usages and costs. Major hyperscalers have committed to ratepayer protection frameworks. Meanwhile, residential electricity prices rose sharply in 2025, and utilities requested multibillion-dollar infrastructure cost recoveries that have already influenced project economics for large facilities. Those conditions increase the value of modular approaches that optimize power density, on-site resiliency, and phased deployment.

Prefabricated And Modular Data Centers Market

Factory-built advantage: Controlled-factory construction continues to unlock predictable schedules and quality assurance. The growing availability of standardized modular platforms shortens lead times for capacity additions and reduces exposure to on-site labor volatility — a decisive advantage when rapid capacity delivery is tied to business continuity or revenue milestones.

PW Consulting’s research goes beyond headline forecasts. The study is constructed as a decision support system for buyers, operators, and investors considering modularization in 2026 and beyond. Key deliverables inside the full report include:

Scenario-based demand models and TCO frameworks calibrated to 2026 energy and construction dynamics — enabling sensitivity analysis for utility cost escalation, labor constraints, and capex deferral strategies.

Vendor scorecards and procurement playbooks that align technical fit (e.g., liquid cooling readiness, busway power distribution, redundancy topology) with commercial terms and factory integration capabilities.

Deployment playbooks for edge, telco, colocation, and hyperscale use cases — including phased build strategies that minimize stranded capacity while enabling rapid ramping for burst workloads.

Risk matrices covering regulatory exposure, grid interconnection timing, and raw-material/energy price shocks, with mitigation pathways and contractual structures that preserve optionality.

Implementation checklists for mechanical-electrical integration, liquid-cooling adoption, and commissioning to reduce time-to-first-workload and accelerate predictable performance validation.

The modular data center market is expanding quickly but is not highly concentrated. Our concentration analysis shows that the top three players collectively account for a significant minority of market revenue, and the top five remain under half of total market sales. This fragmentation underscores two realities: first, technical diversity and differentiated go-to-market models are still decisive; second, there is room for consolidation and partnership strategies that can rapidly scale factory capacity and solution portfolios.

For procurement teams and strategic investors, this means that competitive benchmarking should prioritize specific technical capabilities, manufacturing footprint, and integration competencies rather than assuming incumbent dominance. Vendor selection in 2026 will be as much about roadmap alignment and factory capacity assurance as it will be about price per kW.

We profile and evaluate leading suppliers that are shaping modular and prefabricated solutions today. Representative players span multinational platform providers, power-specialist OEMs, and specialized factory-build vendors:

Schneider Electric — A global systems integrator delivering modular EcoStruxure solutions and pod-based architectures optimized for high-density AI workloads, including integrated liquid-cooling and high-power distribution busways. Recent alliances underscore its push into AI-specialized modular systems.

Vertiv — A supplier focusing on scalable factory-integrated prefabricated systems, with product launches oriented to overhead infrastructure and liquid cooling for AI and HPC environments. Vertiv’s partnerships and OneCore portfolio demonstrate a platform approach for multi-megawatt modularization.

Huawei — Offering a broad FusionModule family for edge, telco, and scalable deployments, designed for quick roll-out and vertical integration with telco operators and cloud providers.

Eaton — Power-focused modular solutions emphasizing UPS, resilience, and integrated power management for edge and AI applications.

Specialists (BMarko Structures, CenCore, CDM, PodTech, TAS, Delta Electronics) — Niche and mid-market players that deliver custom containerized and pod solutions, often with TEMPEST-compliant, defense-grade, or highly configurable factory-built offerings that appeal to colocation, edge, and specialized enterprise needs.

Recent product activity — including new modular overhead infrastructure systems and pod launches — confirms that suppliers are racing to bundle power, cooling, and containment into factory-integrated products tailored for AI-scale density. Strategic partnerships between systems integrators and compute OEMs are accelerating time-to-deploy and lowering integration risk.

Policy and utility-regulatory dynamics are shifting procurement calculus. Several U.S. states have advanced legislation in 2026 requiring data centers to internalize incremental energy infrastructure costs and report consumption to protect ratepayers. In parallel, large cloud providers’ ratepayer protection pledges have altered intergovernmental expectations and utility negotiation dynamics.

Operationally, this results in three priority considerations for executives:

Grid Interconnection & Project Timing — Expect longer, more conditional interconnection timelines in some jurisdictions and potential cost-shifting requirements that can erode projected margins for large builds. Modular approaches that enable phased energization reduce upfront exposure.

Energy Resilience & On-site Options — With residential electricity prices and utility requests for infrastructure recovery rising, integrating onsite generation, storage, and energy management into modular designs becomes a strategic lever to control operating expense volatility.

Contracting & Rate Structures — Negotiating milestone-aligned tariffs and conditional infrastructure funding clauses will be necessary. That requires closer collaboration between real-estate, legal, and energy procurement functions when buying modular systems.

Adopt phased modularization: Prioritize pod-based or module-first architectures to match capacity expansion with demand, limit stranded capital, and preserve future redesign options for liquid cooling and higher power densities.

Condition vendor selection on factory capacity and supply-chain resilience: Evaluate suppliers’ manufacturing footprints, floor-to-factory logistics, and their demonstrated ability to hit compressed delivery timelines.

Integrate energy strategy into early design: Model combined scenarios for utility tariffs, on-site DER (distributed energy resources), and storage; use modularity to test and scale energy configurations with lower financial risk.

Standardize interfaces and commissioning procedures: Specify mechanical and electrical interface standards and acceptance tests in contracts to reduce heterogeneity across deployments and lower lifecycle OPEX.

Leverage partnerships over acquisitions for speed: For organizations seeking rapid capacity, partnering with established modular suppliers or co-developing factory lines can be faster and less capital-intensive than greenfield construction.

Our full report is designed to be an executable briefing for 2026 decision-makers: it blends a market sizing and forecast framework with procurement templates, vendor scorecards, deployment playbooks, and scenario-based TCO tools that are ready to be adapted to your portfolio and regulatory environment. We intentionally balance transparency with discretion: the report demonstrates methodology, assumptions, and sensitivity levers while preserving proprietary sub-segmentation and revenue-level tables for subscribers and licensed users.

With the modular market expanding from a sizable 2025 base and growing at a double-digit CAGR, organizations have a narrow window in 2026 to reframe how they source, finance, and operate compute capacity. The modularization wave is not simply about faster builds — it represents a chance to realign capital intensity, decouple deployment schedules from utility-pace, and adopt energy-smart designs that mitigate regulatory and rate pressures.

For strategy teams, procurement leads, and infrastructure investors, PW Consulting’s study provides the decision-ready insights required to act with confidence in 2026. For a full set of datasets, vendor scorecards, and our scenario TCO models — including the detailed breakdowns and validated supplier comparisons that we intentionally reserve for the report itself — please visit our official publication page to access the complete research package.

For detailed analysis of this topic, please visit the official page:Prefabricated And Modular Data Centers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com