M Cresol Market 2026: Strategic Imperatives from PW Consulting’s Forward-Looking Analysis

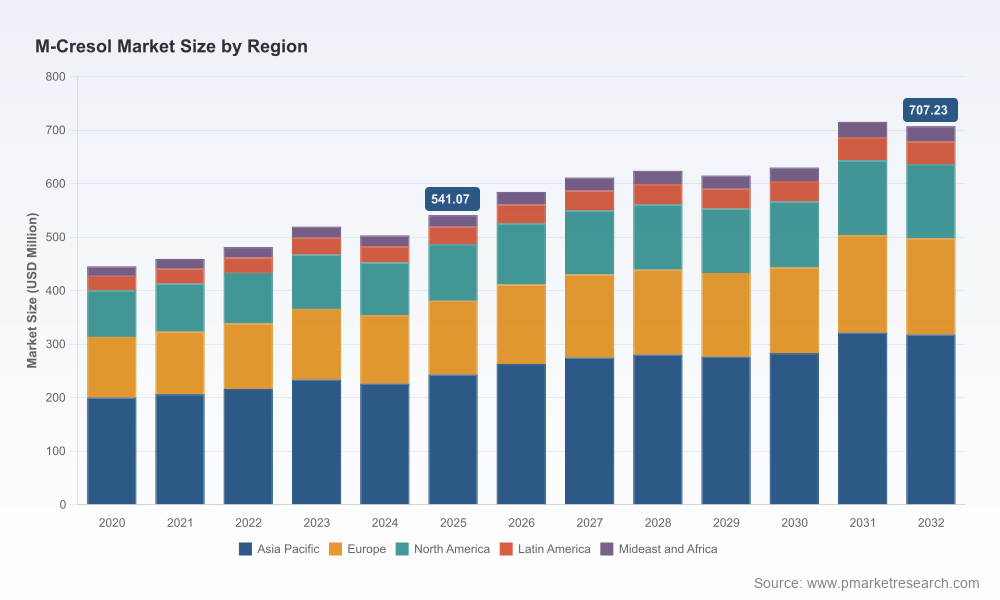

PW Consulting’s latest market study on M Cresol delivers an actionable intelligence package built to shape confident corporate decisions in 2026. Grounded in a calibrated historical series (2020–2025) and a seven‑year forecast window (2026–2032), the report synthesizes market sizing, cost dynamics, regulatory pressure points, and competitive strategy into a practical playbook for producers, buyers, and investors. The global M Cresol market reached USD 541.07 Million in the base year 2025 and is projected to grow at a compound annual growth rate (CAGR) of 3.9% through 2032—culminating in a market environment where selective premium positioning, feedstock management, and trade strategy will determine winners and losers.

M Cresol Market

Why this report matters for 2026 decision-making

2026 will be a year of consolidation and re‑pricing for phenolic intermediates. The convergence of feedstock volatility, targeted trade measures, and tightening environmental standards is reframing how midstream chemical companies make capital and sourcing choices. PW Consulting’s M Cresol market report was designed specifically to support three categories of strategic decisions in 2026:

M Cresol Market

- Capital allocation: Choose between brownfield debottlenecking, targeted capacity expansion for high‑purity grades, or investment in downstream integration to capture higher margins.

- Supply‑chain design: Rework sourcing and hedging strategies to manage benzene/toluene feedstock exposure and tariff impacts across procurement portfolios.

- Portfolio strategy: Identify premium product niches (high‑purity synthetic grades, pharma intermediates, specialty resins) where differentiation and tighter quality controls create defensible margins.

Report coverage — practical tools and deliverables

The study is built as a management toolkit, not an academic paper. It combines robust market statistics with tactical instruments that executives can deploy immediately:

M Cresol Market

- Validated market size curve (2020–2025) and a granular forecast to 2032, including revenue scenarios under three macroeconomic assumptions.

- Feedstock sensitivity models that quantify the impact of benzene and toluene price swings on plant‑level margins and break‑even prices.

- Tariff and trade‑policy impact matrices—showing how Section 301 measures and recent levies can alter landed costs and make local production competitive in targeted markets.

- Regulatory compliance checklists and CAPEX/OPEX benchmarks for emissions control and waste management for phenolic streams.

- Competitive landscaping with supplier scorecards, capability maps (high‑purity vs industrial grade), and M&A scoping templates based on concentration metrics.

- Go‑to‑market playbooks for sellers of high‑purity M Cresol (pricing, certification, and downstream partnerships) and for large consumers (sourcing, qualification, and dual‑sourcing templates).

Market dynamics: the levers that will shape 2026 outcomes

Our analysis isolates four primary dynamics that will govern near‑term outcomes:

- Feedstock economics: M Cresol production remains closely tied to aromatic feedstocks. Periodic declines in feedstock costs (for example, the softer naphtha pricing that helped ease production costs in late 2025) can rapidly restore margin, while regional spikes in toluene or benzene lift break‑even thresholds and pressure smaller producers.

- Trade policy and tariffs: Recent trade measures have materially changed the calculus on import dependence. Elevated duties on certain origins introduced in 2025 create a structural cost premium for some imported cresol streams, making onshore capacity and tariff‑aware sourcing strategies more attractive.

- Regulatory compliance: Environmental and safety regulations for phenolic compounds require continuous investment in emissions control and wastewater treatment. These are non‑optional overheads that favor larger producers with scale and capital access.

- Demand composition: Demand continues to bifurcate between high‑purity synthetic grades (serving pharmaceuticals, fine chemicals, and electronic applications) and broader industrial grades. Strategic differentiation—through quality, traceability, and co‑innovation with downstream customers—will drive margin expansion.

Competitive landscape: what concentration means for strategy

The M Cresol market demonstrates meaningful concentration among a limited number of global and regional players. PW Consulting’s competitive mapping shows a top‑three cluster that captures a substantial portion of industry volumes, and a top‑five group that accounts for the majority of tradable capacity. This concentration creates both risk and opportunity:

- For established producers with technical and purity advantages, consolidation dynamics enable disciplined pricing and targeted capacity utilization strategies.

- For midsized and regional players, selective vertical integration into downstream niches—combined with closer customer partnerships—can create defensible positions even in a concentrated environment.

- For buyers and traders, concentration increases counterparty risk but also creates clearer pathways for long‑term contracts and supplier development programs.

The report’s company profiles examine the strategic positioning of incumbent leaders and notable regional suppliers. Profiles include capability differentiators—such as LANXESS AG’s high‑purity offerings and Mitsui Chemicals’ intermediates capabilities—alongside exporters and synthetic route specialists from other regions. Each profile evaluates production technology, quality certifications, and strategic focus, offering readers a rapid due diligence starting point.

Strategic recommendations for 2026

From the analysis, PW Consulting derives targeted recommendations designed for leadership teams updating FY‑26 strategy:

- Hedge and diversify feedstock exposure: Implement layered hedging that covers both aromatic feedstock inputs and regional freight/tariff risk. Consider strategic offtake with integrated suppliers to stabilize margins.

- Prioritize high‑purity investments: Allocate incremental capital to upgrade purification and certification capabilities where downstream premiums exist—particularly for pharmaceutical and electronic end‑markets.

- Reassess trade footprints: Use tariff scenarios and landed cost models to decide between maintaining import channels, near‑shoring, or greenfield options. Incremental onshore capacity can be viable where duties materially inflate imported feedstock costs.

- Capitalize on consolidation opportunities: Given the market concentration, be prepared to evaluate M&A or JV targets that add technical capability or regional access—particularly assets that can be economically retrofitted for higher‑purity production.

- Embed regulatory resilience: Make environmental compliance and waste management an investment, not an afterthought. Early adoption of best‑in‑class pollution controls reduces future stranded‑asset risk and unlocks premium customer segments.

Risk scenarios and contingency planning

Our scenario work highlights three downside shocks that buyers and producers must model into 2026 plans: a sustained spike in aromatic feedstock prices, accelerated tariff escalation on key trade lanes, and tightening emissions standards that raise operating costs. For each shock, the report presents a set of mitigation pathways—ranging from short‑term sourcing swaps and temporary hedges to longer‑term capital interventions such as feedstock diversification into alternative synthetic routes.

What we intentionally withhold (and why)

PW Consulting follows a “trailer” publishing approach: this public brief demonstrates the analytical depth and practical orientation of the full study while withholding granular segment tables, regional/application split values, and plant‑level economics. These detailed datasets—including the full region and application breakdowns, supplier share by market, and model files—are available with the full report package for subscribers and purchasers. This editorial choice enables readers to validate high‑level conclusions here and then access the complete data set when making binding commercial decisions.

How to use the report in your 2026 planning cycle

Leaders should use the study to accelerate three planning activities in Q1–Q2 2026:

- Incorporate the feedstock sensitivity model into procurement and treasury stress tests.

- Run the tariff impact matrix against your current import profile and evaluate near‑term procurement shifts.

- Use supplier scorecards and the M&A screening templates to prioritize partnership and acquisition targets aligned with your strategic ambition (scale, quality, or downstream integration).

Final perspective

The M Cresol market is not a static commodity arena—its economics are being reshaped by feedstock cycles, policy levers, and quality‑driven end‑market growth. With a 2025 base of USD 541.07 Million and a projected 3.9% CAGR to 2032, 2026 represents a pivotal year to reset sourcing, invest in premium capabilities, and position for consolidation. PW Consulting’s report provides the decision‑grade tools and scenario playbooks to convert uncertainty into competitive advantage. For companies that act decisively in 2026—optimizing feedstock exposure, protecting margins through quality differentiation, and aligning regulatory investments—the market offers sustainable value creation through the decade.

Access the full report to retrieve the complete datasets, detailed segmentation tables, and executable templates that underpin these conclusions.

For detailed analysis of this topic, please visit the official page:M Cresol Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com