PW Consulting: Vacuum Atmosphere Furnace Market Set to Expand at a 7.85% CAGR in 2026–2032, Driving Sector Momentum

Other |

2026-07-02 15:28:48

PW Consulting today releases an executive briefing highlighting the strategic implications of our new Laser Line Dielectric Mirror Market report (base year 2025, forecast 2026–2032). This briefing synthesizes the report’s high-conviction findings to support leadership teams making capital, sourcing, product, and M&A decisions in 2026. It showcases the actionable analysis and scenario work contained in the full study while intentionally withholding granular segment and regional line-item figures to preserve the report’s role as the primary source for market-specific purchase decisions.

Laser Line Dielectric Mirror Market

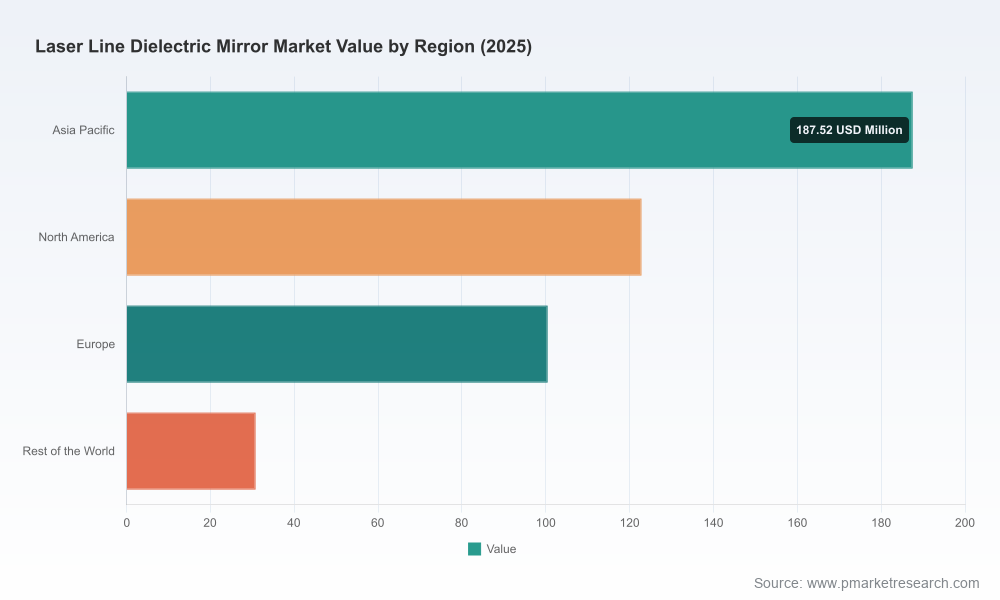

Market momentum: The laser line dielectric mirror market is a mid-sized but steadily expanding component of the broader photonics supply chain. Our model shows that the market grew consistently through the early 2020s and reached a substantive $USD Million level in 2025; under our central-case assumptions it continues to expand through the forecast window at a compound annual growth rate of 6.25%.

Laser Line Dielectric Mirror Market

Strategic leverage: These mirrors are critical in high-value end markets — from industrial laser material processing and ultrafast scientific systems to medical instrumentation and defense platforms. Small improvements in mirror performance (damage threshold, group delay dispersion, multi-wavelength stability) translate into outsized value for system integrators, creating attractive margin and differentiation opportunities for capable suppliers.

Laser Line Dielectric Mirror Market

Supply chain sensitivity: Coating and substrate inputs, manufacturing methods (ion beam sputtering, e-beam, IBS), and lead times materially affect customer selection and procurement strategies. Recent regulatory developments and raw-material constraints have raised the strategic importance of sourcing resilience.

Our historical tracking (2020–2025) documents a steady recovery and expansion from the pandemic period into a structurally larger market by 2025. Under our baseline forecast, the market extends through 2032 with consistent mid-single-digit CAGR growth (6.25%), driven by rising demand in laser material processing and incremental adoption in medical and research systems. The report provides year-by-year market sizing in USD Million for 2026–2032 and alternative scenarios for slower and faster adoption pathways, enabling CFOs and corporate strategists to stress-test capital allocation plans and revenue targets.

Proprietary market model: A transparent, auditable model with historical time series (2020–2025), detailed forecasting logic for 2026–2032, and sensitivity knobs to re-run scenarios under different macro, supply, and technology assumptions.

Commercial playbook: Go-to-market and pricing strategies for suppliers and OEMs, including channel structuring, inventory buffering tactics, and service-level architectures that reduce lead-time premium without eroding margins.

Supplier scorecards: Comparative capability matrices across manufacturing technologies (IBS, e‑beam, sputtering), coating performance (LIDT, reflectivity, GDD), quality systems, and lead-time commitments — designed for use in SRM and sourcing negotiations.

Supply chain, risk, and mitigation mapping: Identification of critical upstream dependencies (substrates, rare coating materials, specialized deposition equipment), scenario-based disruption impact analysis, and actionable mitigation playbooks (dual sourcing, inventory strategies, localized manufacturing).

Technology deep dives: Technical notes on substrate choices (fused silica, Zerodur), dielectric stack architectures for single- and multi-line mirrors, and trade-offs between narrowband HR performance and broadband/ultrafast designs, with recommended test protocols for LIDT and spectral stability.

M&A and partnership roadmap: Valuation heuristics, integration checklist, and a short-list of acquisition targets for strategic buyers seeking to accelerate capability in high-power or ultrafast mirror technology.

The market is moderately concentrated: the top three players account for a meaningful but non-dominant share of industry revenues, and the top five expand that share to just under half the market. That structure creates room for regional specialists and technology-focused challengers to win on performance, speed, and cost. Below we profile the competitive archetypes that matter to buyers and strategists.

Established system suppliers with breadth — Companies such as Thorlabs (Newton, NJ, USA) and Newport Corporation (Irvine, CA, USA) combine broad product catalogs with strong distribution and engineering support. Their advantage lies in predictable supply, extensive testing capabilities, and the ability to bundle optics into sub-systems for OEM customers.

Optical specialists with deep coating capability — Firms including Edmund Optics (Barrington, NJ, USA), Layertec (Mellingen, Germany), and OPTOMAN (Vilnius, Lithuania) compete on coating precision, low group delay dispersion variants for ultrafast lasers, and custom spectral designs. These providers are often preferred where performance tolerances are tight.

High-damage-threshold and high-reflectivity niche players — Manufacturers such as Alien Photonics (Vilnius, Lithuania), Perkins Precision Developments (Longmont, CO, USA), and Alluxa (product developments in 2025) target the highest LIDT and ultra-high reflectivity needs, particularly for high-energy and defense applications.

Cost and scale-oriented producers — Asian manufacturers (examples include Shanghai Optics and Hangzhou Shalom EO) balance competitive pricing with increasingly sophisticated coating capabilities. Their strategic advantage lies in high-volume production and speed-to-market for standard product lines and custom OEM runs.

Regional enablers and component specialists — Companies such as LASER COMPONENTS (Germany), CVI Laser Optics (IDEX), and Wavelength Opto-Electronic (Singapore) are important to system integrators seeking regional supply continuity and application-specific engineering support.

Recent supplier moves illustrate these dynamics: Layertec’s 2026 catalog expansion signals continued investment in large reference assemblies and precision coatings; OPTOMAN’s trade-show engagement highlights competitive focus on repeatability in IBS coatings; and supplier awards to firms like LASEROPTIK underscore the premium placed on short lead times and high LIDT performance.

Regulatory and trade risk: Export controls introduced in 2025–2026 affecting critical materials and production equipment have already elevated material costs and extended lead times for some suppliers. Companies should assume ongoing geopolitical tailwinds toward regionalization and increased scrutiny of supply chains.

Raw material constraints: Key substrates and coating materials (e.g., fused silica, specialist layers) remain concentrated among a small set of suppliers. Substrate selection and coating stack thickness decisions (typical HR coatings for 1064 nm are multiple microns in thickness) materially affect production geometry, throughput, and yield.

Technology substitution pressure: Advances in deposition methods and new multilayer designs are compressing lifecycle time for product differentiation. Suppliers that do not invest in next-generation deposition and metrology will face price pressure and margin erosion on commodity lines.

Customer procurement sophistication: OEMs and system integrators increasingly demand supplier transparency on LIDT testing, batch traceability, and sustainability practices — creating selection criteria that go beyond price and nominal spectral specs.

Sourcing strategy: Build multi-tiered supplier relationships that separate strategic, capability-critical components (e.g., high-LIDT coatings, large-format substrates) from commodity items. Implement contractual guardrails for capacity and lead-time assurances tied to penalties or option capacity.

R&D and product roadmap: Prioritize investments in coating technologies that demonstrably raise damage threshold and reduce group delay dispersion for ultrafast applications. Where feasible, co-invest in qualification testbeds with key customers to lock in early adopter deployments.

M&A and partnerships: Use acquisitions to rapidly augment in-house coating capabilities, metrology, or regional manufacturing footprint. The market’s concentration profile means bolt-on deals can be earnings-accretive if integration risk is managed.

Risk management: Establish a clear mitigation plan for material export restrictions, including alternate material formulations, qualifying secondary substrate suppliers, and geographic diversification of critical coating capacity.

This report is structured as an operational tool for leadership teams — not a descriptive summary. It combines a rigorously documented market model, supplier scoring, and executable commercial playbooks that procurement, product, and corporate development teams can apply directly to 2026 planning cycles. Importantly, the report’s appendices include testing protocols, an audited supplier capability database, and a deal-ready M&A checklist.

To preserve the commercial integrity and competitive advantage of our analysis — and to align with the “trailer” principle — we have withheld granular regional shares and application-specific line-item figures in this briefing. Subscribers to the full report receive the complete breakdowns, model files, and vendor scorecards needed to operationalize the insights for procurement tenders, product roadmaps, and M&A diligence.

For companies making supply, product, or M&A decisions in 2026, the immediate priorities are clear: stress-test 2026 budgets against a mid-single-digit growth baseline, secure conditional capacity for critical coating and substrate inputs, and prioritize technology investments that increase mirror LIDT and ultrafast performance. PW Consulting’s full report provides the models, supplier analytics, and actionable playbooks to implement these steps with measurable KPIs.

Contact PW Consulting to request the full Laser Line Dielectric Mirror Market report and the accompanying model files, supplier scorecards, and scenario workshops tailored for executive planning sessions.

For detailed analysis of this topic, please visit the official page:Laser Line Dielectric Mirror Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com