Syringe Auxiliary Push Device Market: Enhancing Precision and Safety in Medication Delivery

Health |

2025-12-17 19:41:49

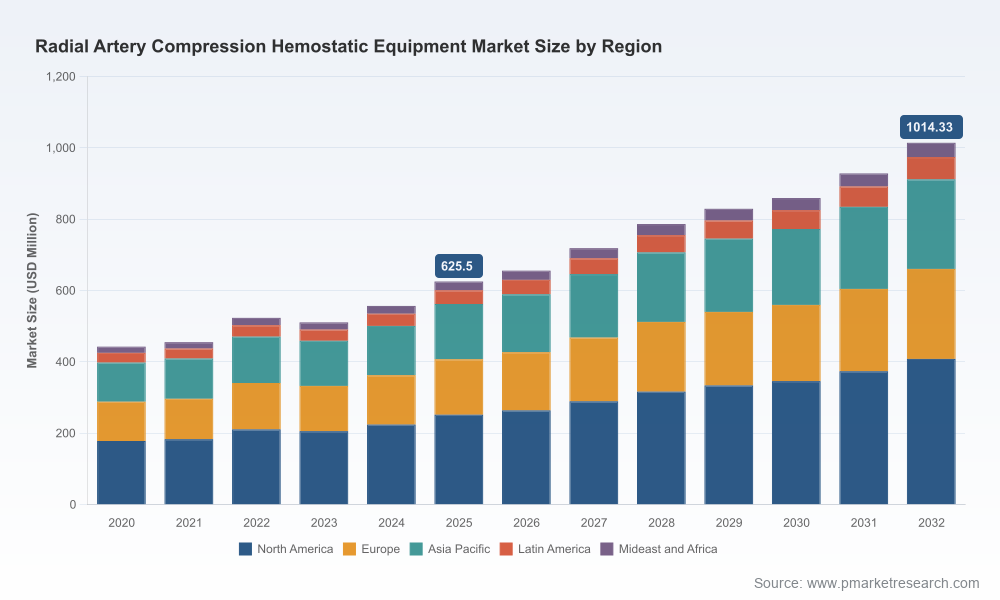

As interventional cardiology and vascular access practices continue their steady march toward radial-first protocols, the market for radial artery compression hemostatic equipment is entering a phase where disciplined strategy will determine winners and fast followers. PW Consulting’s new market study, anchored on a 2025 base year and a 2026–2032 forecast horizon, quantifies a clear growth runway: the global market expands at a compound annual growth rate (CAGR) of 7.15% and moves from an estimated USD 625.5 Million (base year 2025) toward just over USD 1.01 Billion by 2032. This briefing summarizes the report’s strategic value for boardrooms and corporate development teams planning decisions in 2026, without disclosing the proprietary segmentation detail that appears in the full report.

Radial Artery Compression Hemostatic Equipment Market

Clinical momentum toward transradial and distal radial access has created persistent demand for devices that balance reliable hemostasis with patient comfort and patent hemostasis protocols. Published clinical evidence and procedural guidelines increasingly emphasize preservation of radial artery patency to reduce long-term access complications, driving preference for devices that support controlled decompression strategies.

Radial Artery Compression Hemostatic Equipment Market

Regulatory predictability — radial compression devices are typically regulated as Class II devices and often cleared via the FDA 510(k) pathway — reduces time-to-market risk for iterative innovation. This regulatory backdrop encourages both incumbents and new entrants to invest in device evolution, adjunctive consumables, and procedural kits.

Radial Artery Compression Hemostatic Equipment Market

Market consolidation is meaningful: the sector exhibits high concentration at the top (CR3 ~65.4%; CR5 ~82.1%). For 2026 strategy this implies that scale-related advantages in distribution, hospital contracting, and clinical trial sponsorship remain a dominant competitive lever.

Proprietary market-sizing model calibrated across 2020–2025 historicals and forecasted to 2032, with sensitivity analyses that illuminate upside/downside scenarios under varying adoption curves for distal radial access and disposable hemostatic adjuncts.

Go-to-market playbooks segmented by commercial strategy (direct sales vs. distributor partnerships), procurement channel (capital vs. consumable), and end-user economics that reveal unit economics under different hospital contracting arrangements.

Clinical positioning dossiers that map each device archetype to evidence priorities (patent hemostasis metrics, RAO reduction, procedure time, patient-reported outcomes), enabling targeted clinical study design or real-world evidence (RWE) programs.

Regulatory and reimbursement roadmaps for key geographies, including decision trees for 510(k)-based pathways and dossier requirements for novel hemostatic adjuncts intended to support claims beyond predicate equivalence.

M&A and partnership screening matrices identifying capability gaps where bolt-on acquisitions could accelerate access to manufacturing scale, disposable components, or specialty distribution channels.

Pricing and margin benchmarking, with guidance on bundle pricing strategies (device + dressing/patch) that protect installed-base economics while capturing value from recurring consumables.

The market is anchored by a handful of well-capitalized players that control a majority share through a combination of product familiarity, clinical endorsement, and entrenched hospital logistics. Leading manufacturers have refined transparent, adjustable band systems that facilitate patent hemostasis protocols, while a growing set of challengers pursue differentiated ergonomics, distal-specific designs, or integrated hemostatic dressings.

Terumo Corporation — With an established TR Band franchise and a recent product initiative focused on distal access (notably a product launch in May 2026 addressing distal radial procedures), Terumo’s strategy emphasizes iterative innovation that preserves clinical familiarity while addressing procedural shifts. For rivals, Terumo’s approach signals that meaningful advances do not require revolutionary technology; well‑timed, clinically validated variants can sustain leadership.

Merit Medical Systems — Merit’s PreludeSYNC family illustrates a portfolio strategy that balances core mechanical compression systems with variants optimized for ease-of-use and site visibility. Merit’s model underscores the commercial value of a multi-tier product architecture that serves both standard and specialty radial workflows.

TZ Medical, Teleflex, Abbott — These firms compete on focused mechanical features (adjustability, targeted pressure application, wrist support) and distribution reach. Their presence reinforces the importance of hospital contracting, clinician training programs, and supply chain resilience.

Smaller and regional players (including several based in China and niche U.S. innovators) often pursue aggressive price points or design novelties (rotary designs, integrated hemostatic dressings). These entrants can pressure margins in cost-sensitive markets and create localized pockets of competition where purchasing is highly price-driven.

Prioritize clinical differentiation through outcome-focused evidence. With patent hemostasis and reduced RAO increasingly front-of-mind for institutional purchasers, invest in prospective RWE or targeted randomized studies that link your device to demonstrable reductions in access complications or workflow time savings. Even modest, well‑designed studies can shift purchasing behavior in high-volume cath labs.

Build product line architectures that capture recurring value. The core device sale is often a one-time or infrequent purchase; durable growth follows from consumables, dressing systems, or service contracts. Design bundles and subscription-like models that package hemostatic dressing consumables with device training and analytics.

Defend and expand channel partnerships. Given the high concentration among top players, mid‑sized competitors should lock in preferred vendor status through clinician education, consignment stocking, and fast-response logistics. For new entrants, pursue niche clinical champions (distal radial adopters, ambulatory centers) to establish proof points before broader roll-out.

Plan M&A or JV activity with explicit capability targets. Companies seeking rapid scale should evaluate acquisitions that deliver manufacturing scale, clinical trial infrastructure, or access to high-volume distributor networks. The market’s CR3/CR5 profile implies that consolidation can materially shift competitive dynamics in a relatively short period.

Leverage regulatory clarity to accelerate incremental innovations. The predictable 510(k) pathway enables modular product improvements — make regulatory strategy a front-line companion to product design so that incremental variants (e.g., distal-specific configurations, integrated dressings) can be launched with minimal cycle time.

Key market risks include pricing pressure from low-cost suppliers, slower-than-expected adoption of distal radial approaches in certain markets, and potential reimbursement shifts that deprioritize device selection criteria. PW Consulting’s scenario analysis shows that even under conservative adoption assumptions the market maintains positive growth; however, companies that fail to secure clinical endorsement or distribution footholds risk margin erosion.

Mitigant: Emphasize total cost of care narratives — reductions in RAO, shorter compression times, and improved throughput are persuasive in procurement discussions and can offset unit price sensitivity.

Mitigant: Localize commercialization — in price-competitive markets, hybrid models that combine lower-cost manufactured components with local assembly or distribution partnerships preserve margin while enabling competitive pricing.

Commercial planning: Use the report’s go‑to‑market scenarios to size addressable opportunities by procurement channel and craft tailored launch plans for distal-specific devices or consumable bundles.

Clinical strategy: Employ the evidence-mapping tools to prioritize which clinical endpoints to fund for registries and investigator-initiated studies that most influence hospital formulary committees.

M&A diligence: Leverage the market model and concentration metrics to set valuation ranges and identify acquisition targets that close capability gaps or accelerate geographic expansion.

Regulatory and quality planning: Adopt the report’s regulatory roadmap to sequence filings and post-market surveillance commitments to maintain competitive speed without regulatory surprise.

The radial artery compression hemostatic equipment market is not a winner-take-all arena, but it rewards focused scale, clinically credible innovation, and commercial discipline. With a projected CAGR of 7.15% and a clear path to market size that comfortably exceeds the USD 1 billion threshold by 2032, the market offers attractive returns for firms that invest in evidence generation, smart bundling of recurring consumables, and channel lock‑in. PW Consulting’s full report delivers the granular models, playbooks, and M&A screens necessary to convert these macro opportunities into executable 2026 strategies — including the tactical sequencing and budget forecasts that senior executives need to present to boards and investors.

For companies seeking the detailed regional and subsegment breakdowns, vendor share evolution, and the full set of financial model outputs necessary for transaction diligence or product launch planning, the complete PW Consulting Radial Artery Compression Hemostatic Equipment Market report provides the proprietary data and executable templates required to act with confidence in 2026.

For detailed analysis of this topic, please visit the official page:Radial Artery Compression Hemostatic Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com