PW Consulting Releases Strategic Brief: Casting and Splinting Market — A 2026 Playbook for Competitive Advantage

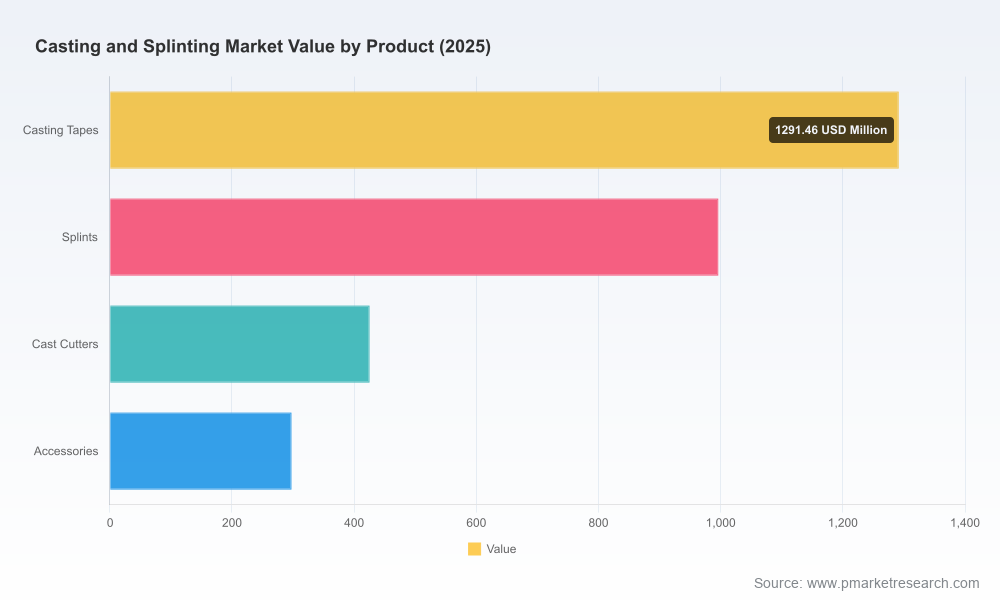

PW Consulting today publishes an executive-level industry insight to accompany our full Casting and Splinting Market report (base year 2025, forecast 2026–2032). The global market, measured at approximately USD 3,010 million in 2025, enters 2026 at an inflection point; our forecast shows a return to sustained expansion with a compound annual growth rate (CAGR) of 6.18% across the 2026–2032 horizon, taking the market toward a multi-billion-dollar opportunity by 2032. This briefing outlines why the findings matter for leadership teams making capital allocation, product, and commercial decisions in 2026 — while reserving the granular segmentation tables and proprietary scenario matrices for the full report.

Casting And Splinting Market

Why this research matters for 2026 decision-makers

- Actionable foresight: The market’s projected mid-single-digit CAGR masks materially different risk–reward profiles across product types, materials and channels; understanding those profiles is essential for prioritizing R&D and commercialization spend in 2026.

- Regulatory and reimbursement timing: With device innovation accelerating (bio-based resins, thermoplastics, 3D-printed custom splints), early-stage regulatory strategy and HCPCS coding preparedness are determinative for product launch windows and revenue recognition.

- Competitive positioning: Moderate market concentration means moves by a handful of incumbents materially change market dynamics; targeted partnerships, distribution plays, and selective M&A can meaningfully accelerate share gains.

- Procurement levers: Hospitals and clinic systems are optimizing for strength-to-weight, turnaround time and total cost of care — procurement sourcing strategies developed now will shape unit economics through the next contract cycle.

High-level findings — a calibrated look (teaser)

Our cross-validated analysis identifies four concurrent forces that will govern performance in 2026 and beyond: material innovation, care-site migration, regulatory/reimbursement complexity, and selective consolidation. The combination of faster-setting composite materials, the uptake of thermoplastics and 3D-printing for personalized splints, and patient-centred comfort improvements are driving buyers toward differentiated SKUs. At the same time, outpatient and ambulatory care settings continue to absorb case volume, shifting purchasing patterns and inventory strategies.

Casting And Splinting Market

From a market structure standpoint, the sector is not fragmented chaos nor tight oligopoly; the top three suppliers account for a significant minority of supply, and the top five further extend reach — a competitive environment that rewards scale but leaves room for focused challengers and technology-first entrants. For executives, this means a dual strategy: defend core institutional accounts through supply reliability and value-based contracting, while deploying nimble, product-led plays into specialized and ambulatory channels.

Casting And Splinting Market

Competitive landscape — who’s shaping the market and why it matters

The competitive map includes multinational incumbents with deep distribution and channel relationships, alongside specialised manufacturers and material innovators. Key players profiled in the report include established industrial players and orthopedics specialists; our company dossiers synthesize strategic posture, capability gaps, and near-term initiatives that will influence 2026 positioning.

- 3M Company — continuing to leverage formulation and materials science to extend product differentiation; recent launches emphasize comfort and sustainability, keeping 3M at the innovation vanguard.

- Zimmer Biomet — expanding into personalized care with additive manufacturing capabilities for custom splints, signaling an ambition to own higher-margin, bespoke solutions for complex cases.

- DJO Global (Enovis) — focused on rehabilitation-aligned splints and bracing that bridge acute immobilization and longer-term recovery products, suited to bundled care pathways.

- BSN Medical (Essity) — product modularity and rapid-curing systems target emergency and sports medicine settings where speed-to-fit and ventilation are competitive differentials.

- Stryker, Smith & Nephew, B. Braun and select regional manufacturers — collectively maintain comprehensive portfolios and channel depth, with varying emphasis on hospital procurement, outpatient clinics, and distributors.

- Regional players and specialty suppliers — continue to exploit local relationships and unique material competencies to serve niche clinical workflows.

Recent market actions illustrate strategic intent: global manufacturers introduced new semi-rigid and breathable casting tapes and modular fast-curing splint systems in 2024–2025, partnerships expanded distribution coverage late in 2025, and early 2026 brought proof-of-concept commercialization of 3D-printed custom splints. These moves accelerate product substitution and create first-mover advantages for companies that pair technical innovation with reimbursement readiness.

Regulatory, reimbursement and supply-chain dynamics

- Reimbursement: Proper coding and documentation are critical for realization of reimbursement value. Casting and splinting supplies are routinely referenced under HCPCS Q4001–Q4051 categories; differentiation by material, age bands and anatomic location has practical implications for clinical documentation and reimbursement capture.

- Regulation: Novel materials and design methods follow medical device clearance pathways; FDA 510(k) considerations remain central to time-to-market planning for new materials or device formats in orthopaedic immobilization.

- Raw materials & procurement: Material cost and availability — especially for fiberglass and specialized resins — influence hospital-level preference for certain product classes. The report maps supplier concentration, key inputs, and contingency options for procurement teams.

What the full report contains — operationally useful modules

The PW Consulting report is designed as a strategic toolset rather than a static dataset. Core deliverables include:

- Executive summary with near-term implications for 2026 budgets and go-to-market plans.

- Historical market-sizing (2020–2025) and a detailed forecast (2026–2032) with scenario sensitivity (base, conservative, and accelerated cases).

- Product and material taxonomy, including clinical use-cases, procurement drivers and price-pressure vectors.

- Regulatory and reimbursement playbooks — step-by-step actions to align product launches with coding and clearance timelines.

- Comprehensive competitive intelligence dossiers (strategic intent, capability map, M&A appetite, pricing posture).

- Channel and distribution analysis with negotiation levers for hospital systems, group purchasing organizations, and outpatient networks.

- Innovation radar on 3D printing, bio-based resins, and thermo-responsive materials with commercialization readiness assessments.

- Supply-chain stress tests and sourcing alternatives to mitigate raw material volatility.

- Commercial templates: procurement scorecards, RFP language, and integration blueprints for partnerships and acquisitions.

How executives should use this intelligence in 2026

Below are practical, near-term uses for leadership teams planning in 2026:

- R&D and product roadmap: Reallocate budget toward material science and personalization capabilities where higher margin expansion and defensibility exist.

- Commercial deployment: Segment field forces between institutional accounts (scale, reliability) and ambulatory/sports medicine channels (product-led trials, partner co-marketing).

- Regulatory & reimbursement readiness: Initiate HCPCS crosswalks and 510(k) pre-submission strategies to avoid launch delays and to maximize reimbursement realization.

- M&A and partnership screening: Use the report’s M&A scorecard to identify tuck-in targets that add distribution, specialized materials, or localized manufacturing capacity.

- Procurement negotiation: Equip sourcing teams with alternative-material playbooks and total-cost-of-care arguments to capture better contract terms.

Market concentration and competitive implications

The market exhibits measurable consolidation: the top three and five players control a meaningful share of the market’s commercial flows. This level of concentration creates predictable competitive dynamics — price competition in commoditized product lines, while innovation pockets become battlegrounds for value capture. Our strategic recommendations prioritize defending core revenue streams through supply assurance, while investing selectively in differentiated products that command premium pricing and improved reimbursement pathways.

Next steps — how to act on these insights

For teams preparing 2026 plans, the full PW Consulting report provides the granular segmentation, regional matrices, pricing curves, and M&A target lists that underpin confident execution. The briefing you are reading is designed as an operational preview; the complete dataset and proprietary scenario models are available through our report portal for clients and partners.

Contact PW Consulting to schedule a tailored briefing with our industry lead and receive an executive package customized to your strategic questions. The full report contains the detailed segment-level tables, regional breakdowns, and proprietary forecasts that enable transaction-level decision-making — intentionally withheld from this preview to preserve the competitive advantage available to report subscribers.

About PW Consulting

PW Consulting provides senior-level strategy and market intelligence to medical device manufacturers, distributors and health-system executives. Our research blends proprietary modeling, primary interviews across the care continuum, and rigorous scenario analysis to translate industry change into practical choices and measurable outcomes.

For detailed analysis of this topic, please visit the official page:Casting And Splinting Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com