Anastomosis Devices Market Developments in Vascular Surgery Techniques

Other |

2026-03-12 07:50:17

PW Consulting’s latest market research on Clinical Disorder Treatment provides an essential strategic playbook for executives preparing decisions in 2026. Anchored on a detailed historical review (2020–2025) and a forward-looking forecast (2026–2032), the study synthesizes market-sizing, competitive positioning, regulatory inflection points, and practical go-to-market scenarios. Our analysis shows a durable, mid-single-digit growth trajectory — a compound annual growth rate of 6.18% — underscoring sustained commercial opportunity even as the sector undergoes structural change. This brief highlights the report’s strategic value while intentionally omitting the granular segment tables to encourage direct engagement with the full report for transaction-grade data.

Clinical Disorder Treatment Market

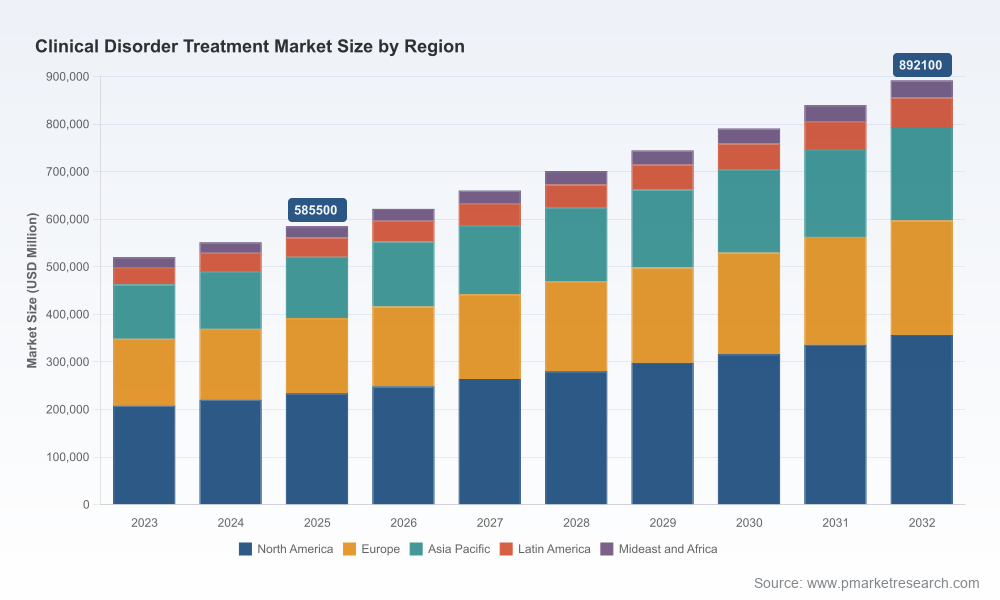

Clinical disorder treatment is in a period of steady expansion. The overall market base year is 2025, and the PW Consulting model projects consistent growth through the 2026–2032 forecast horizon. The market’s trajectory reflects the convergence of several tailwinds: rising prevalence and diagnosis rates, widening reimbursement for mental health services, the emergence of novel therapeutic classes, and the scaling of digital and hybrid care models. At the same time, the market remains only moderately consolidated, with a low concentration among the top three and top five participants — a structural feature that favors new entrants and differentiated specialty strategies.

Clinical Disorder Treatment Market

The market features a diverse set of competitors spanning global pharmaceutical companies, generics manufacturers, and dedicated behavioral health service operators. The sector’s three- and five-firm concentration ratios indicate an open competitive field: market share is distributed, and scale matters but does not dominate outcomes in many subspaces.

Clinical Disorder Treatment Market

Key company profiles analyzed in the report include market leaders with established CNS portfolios, major generics suppliers, and behavioral health networks. For each player we assess therapeutic anchors, pipeline proximity to market, commercial reach, and strategic levers including partnerships, M&A, and portfolio reshaping. Our evaluation highlights which capabilities are likely to win in 2026 and which require urgent investment.

2025–2026 has seen a meaningful acceleration in regulatory activity. Federal initiatives have opened prioritized pathways for certain novel modalities, with early approvals and trial accelerations that shorten traditional development timelines. Concurrently, key patent expirations in late 2026 create imminent generic pressure on several established treatments, shifting competitive calculus for incumbents and opening licensing opportunities for generics players. PW Consulting’s regulatory scenario simulations quantify the market-level impacts and provide recommended hedging strategies.

Insurance coverage is broadening for mental health services, and digital/hybrid care models are shifting patient pathways. Payers are increasingly receptive to value-based constructs for high-cost or high-utilization treatments, especially where robust outcomes and utilization management frameworks exist. For providers, integrating pharmacologic innovation with stepped-care digital therapeutics and community-based delivery can drive improved adherence and downstream cost-offsets. The report offers concrete contracting templates and operational metrics that providers and payers can use to align incentives.

To preserve the strategic integrity of client-level decisioning and to follow the “trailer” principle of this release, we have intentionally withheld our full segmented tables and transaction-grade numerical breakouts in this brief. The PW Consulting flagship report contains detailed regional, disorder-type, and service-setting splits, proprietary forecasting models, and downloadable datasets that underpin the scenarios summarized above. Access to those materials is available through our report portal and is recommended for teams preparing investments, portfolio re-prioritization, or complex negotiations in 2026.

PW Consulting’s Clinical Disorder Treatment Market report is designed as an operational tool for 2026 decision-making: it combines rigorous market economics, granular competitive intelligence, and executable playbooks. For companies and investors navigating an environment of regulatory acceleration, patent turnover, and evolving care models, this research converts ambiguity into prioritized action. Contact PW Consulting to secure the full report and the underlying datasets that power transaction-grade strategy.

For detailed analysis of this topic, please visit the official page:Clinical Disorder Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com