Tissue Heart Valves Market Growth Analysis and Future Expansion Outlook

Health |

2026-04-10 12:21:09

As OEMs recalibrate platforms, materials and supplier networks for the next wave of vehicle programs, the global automotive interior and exterior trim market is entering a phase where tactical decisions in 2026 will materially affect cost, compliance and product differentiation through the early 2030s. PW Consulting’s latest market study, anchored on a 2025 base year and a detailed 2026–2032 forecast, shows the market continuing to expand — growing at an expected compound annual growth rate (CAGR) of 4.7% across the forecast window and projecting meaningful upside by 2032. This briefing highlights the strategic value of the full report for executives who must balance immediate supply-side pressures with multi-year product and sourcing investments.

Automotive Interior Exterior Trim Market

Timing: 2026 is a pivotal year for program sourcing and supplier selection cycles. Decisions taken this year — from material lock-ins to supplier qualification and sustainability roadmaps — will influence cost structures and vehicle specifications through platform lifecycles that stretch into the early 2030s.

Automotive Interior Exterior Trim Market

Scale and trajectory: The market has moved from the low‑to‑mid‑$30 billion range in the early 2020s to an approximate mid‑$40 billion size by 2025, and our model anticipates continued growth toward the low‑$60 billion range by 2032 under the central case. That growth underpins both organic capacity expansion and active consolidation opportunities.

Automotive Interior Exterior Trim Market

Concentration & competition: Market concentration is meaningful but not prohibitive — the top three and top five suppliers capture a notable share of industry revenue, leaving space for nimble specialists and regional champions to win program positions. The market structure creates differentiated strategic paths for tier‑one integrators, component specialists and modular suppliers.

Materials cost volatility: Plastic resin markets remain a primary cost lever. Recent upward pressure on polypropylene (PP) in early 2026 and sustained resin price volatility have sharpened margins for trim manufacturers. For purchasers and suppliers alike, exposure to volatile feedstock costs requires new contracting disciplines (indexation, collars, strategic inventories) and a proactive materials substitution agenda.

Regulatory and circularity mandates: Revised regional ELV rules and recycled content targets are changing material specification pathways. The regulatory trajectory forces manufacturers to validate recycled-content supply chains and to demonstrate compliance without compromising durability, aesthetics or cycle time.

Product and experience differentiation: Interiors are a key battleground in the transition to EVs and shared mobility. Demand for integrated cockpit modules, advanced surfaces, and perceived quality enhancements continues, even as cost pressures mount. Trim suppliers that can package tactile quality with weight and cost optimization will be advantaged.

Supply-chain resilience: Recent industry moves and raw-material shocks underscore the need for geographically diversified manufacturing and second-source strategies, especially for programs with concentrated platform builds or aggressive ramp profiles.

The competitive set combines global integrators, seat and systems specialists, and premium luxury suppliers. Notable players profiled in our report include Magna International Inc. (Aurora, Canada), Grupo Antolin (Burgos, Spain), Yanfeng Automotive Interiors (Shanghai, China), Toyota Boshoku Corporation (Kariya, Japan), Lear Corporation (Southfield, Michigan, USA), Adient plc (Dublin, Ireland), Toyoda Gosei Co., Ltd. (Kiyosu, Japan), Continental AG (Hanover, Germany), DRÄXLMAIER Group (Vilsbiburg, Germany) and IAC Group (Luxembourg).

Strategic patterns: Large integrators emphasize modularization and sustainable materials to secure long-term OEM partnerships. Seat specialists continue to expand surface and integrated trim capabilities to capture greater value per seat assembly.

Recent signals: Award recognitions and financial performance updates from leading suppliers confirm pressure on performance and the premium placed on delivery and innovation. The announced transaction separating certain interiors businesses into standalone entities signals renewed investor interest and creates new strategic alternatives for OEM sourcing.

Implication for OEMs and suppliers: Program teams should intensify supplier due diligence on sustainability credentials, capacity flexibility and materials innovation. For suppliers, pursuing differentiated surface technologies, validated recycled‑content supply chains and demonstrable cost control will be key to winning new business in 2026 RFQs.

Market sizing and forecast model: A transparent, auditable model with historical series (2020–2025 base analysis), our 2026–2032 central forecast, and upside/downside scenarios for macro and materials risk factors.

Supply‑chain risk matrix: Granular assessment of feedstock exposure, supplier concentration risks, logistics chokepoints and contract levers to mitigate input volatility.

Competitive & capability maps: Side‑by‑side profiles of leading suppliers covering product scope, global footprint, sustainability positioning and recent strategic moves.

Materials and innovation playbook: Practical guidance on accelerated qualification of recycled polymers and alternative substrates, cost vs. performance tradeoffs, and co‑development approaches for OEMs and tier suppliers.

Commercial decision tools: Procurement templates for indexation clauses, hedging scenarios and cost‑pass mechanisms; M&A screening criteria and a prioritized list of capability gaps that can be filled by acquisition or JV.

Program strategy roadmaps: Actionable checklists for program managers — supplier selection criteria tied to ramp profiles, quality KPIs and sustainability requirements that reflect upcoming regulatory thresholds.

1. Institutionalize materials cost governance — create cross‑functional “feedstock war‑rooms” that combine procurement, engineering and finance to manage PP and resin exposure. Implement contract mechanisms (indexation, collars, supplier cost audits) and maintain a rolling 12–24 month sensitivity model linked to program pricing.

2. Accelerate recycled-content qualification — move beyond pilot projects to validated production pipelines. Prioritize components and assemblies where recycled content can be scaled without program risk and include recyclability specifications in early design reviews.

3. Reassess supplier portfolios through a capability lens — weigh the benefits of long-term partnerships with modular integrators against tactical second-sourcing to reduce single-point risks. Use our supplier scorecards to quantify fit-for-program metrics.

4. Target bolt-on M&A and JV for capability gaps — the mid‑tier and specialist supplier landscape contains assets that can accelerate time‑to‑market for smart surfaces, lightweight structures and integrated modules. Our screening criteria identify high‑priority targets and valuation sensitivities.

5. Embed sustainability as a cost‑management lever — view regulatory compliance and recycled‑content adoption not only as a compliance cost but as a component of long-term supplier differentiation and potential premium pricing for “green” trim options.

6. Strengthen program execution metrics — add tighter ramp KPIs tied to material yield, scrap rates and rework costs. Contractual incentives that reward on‑time, on‑quality delivery reduce supplier cost risk and protect launch timelines.

This executive summary is designed to surface the core strategic levers that should guide procurement, product and corporate development decisions in 2026. For teams preparing RFQs, negotiating supplier contracts or evaluating M&A targets, the full PW Consulting Automotive Interior & Exterior Trim Market Report provides the underlying data models, supplier scorecards and scenario stress tests you need to convert insight into action.

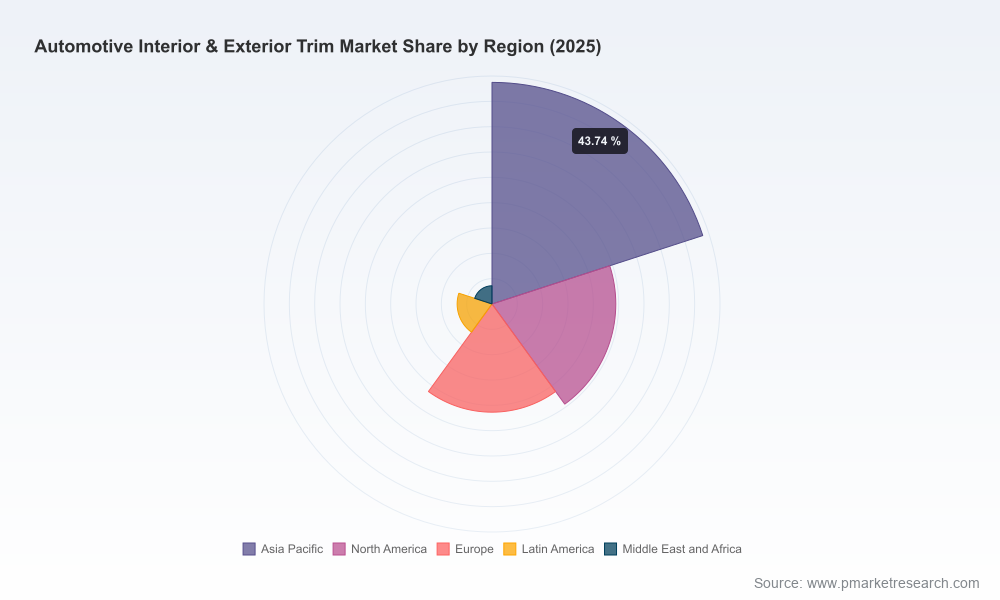

We intentionally reserve granular sub‑segment tables and region‑level allocations for the full report to ensure that decisionmakers access the complete dataset and models directly. That material includes detailed sensitivity analyses, supplier financials and configurable spreadsheets for program‑level cost modeling.

The coming 18–24 months will separate organizations that treat trim as a static commodity from those that leverage it as a strategic lever for quality, brand differentiation and margin protection. With market expansion continuing and material/regulatory pressures intensifying, 2026 decisions will echo across product lifecycles and balance sheets through 2032. PW Consulting’s report is built to help senior leaders convert uncertainty into prioritized, executable plans — from sourcing and supplier strategy to materials innovation and portfolio optimization.

Contact PW Consulting to access the full study, underlying models and tailored advisory support to implement the recommendations outlined here.

For detailed analysis of this topic, please visit the official page:Automotive Interior Exterior Trim Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com