Reciprocating Compressor for Oil & Gas Market — Strategic Outlook 2026: PW Consulting Reveals Tactical Intelligence for Executive Decision-Making

PW Consulting today publishes an executive briefing drawn from its forthcoming market research report, Reciprocating Compressor For Oil & Gas Market (Base Year: 2025; Forecast: 2026–2032). This release is crafted for C-suite leaders, project sponsors, and asset managers who need actionable, risk-calibrated guidance for capital allocation, procurement strategy, and technology adoption in 2026. The briefing highlights the report’s strategic value, key industry dynamics, and competitive implications — while intentionally reserving detailed segment-level figures to drive direct engagement with the full report.

Reciprocating Compressor For Oil Gas Market

Why this report matters for 2026 decisions

Reciprocating compressors remain a foundational technology across upstream, midstream and downstream oil & gas value chains. As operators balance legacy asset optimization with new energy requirements, the market’s trajectory is now governed by a mix of steady demand and structural shifts — from tighter emissions rules to emerging hydrogen service opportunities. Our report synthesizes market sizing, trend analysis, supply-chain stress points, and vendor benchmarking to convert these macro signals into practical steps for near-term decision-makers.

Reciprocating Compressor For Oil Gas Market

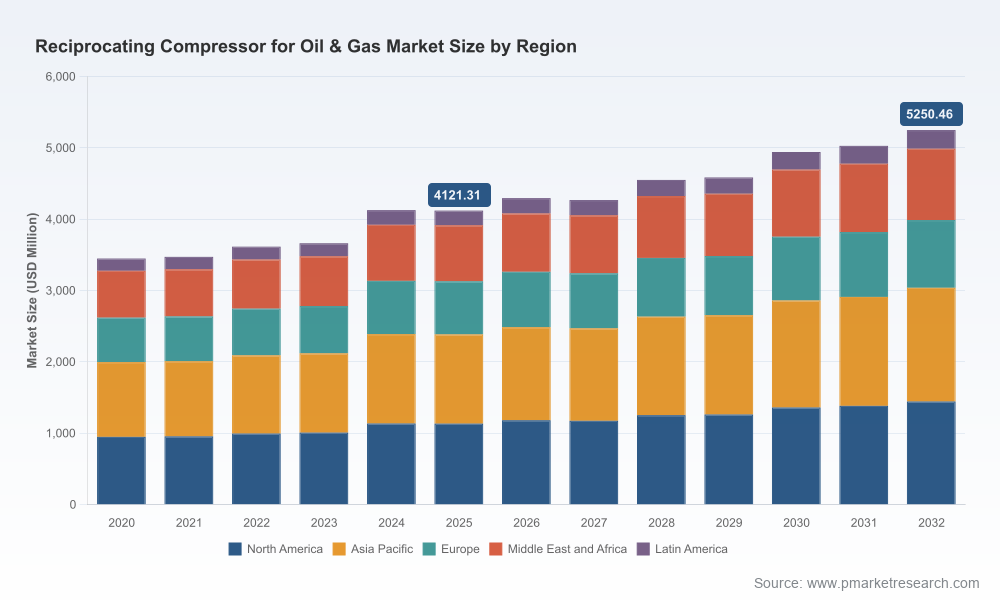

- Quantified market trajectory: The global market reached a material scale in 2025 and, under our baseline scenario, is projected to grow at a compound annual growth rate (CAGR) of 3.52% over the 2026–2032 forecast window. By 2032 the market is expected to be substantially larger than in 2025, reflecting continued demand for conventional gas compression while incremental growth is driven by new-service requirements (e.g., hydrogen-capable systems and CO2-ready designs).

- Action-oriented frameworks: The report is structured to support capital planning cycles in 2026 — offering procurement decision trees, risk matrices for OEM selection, and retrofit vs. greenfield guidance specific to reciprocating compression.

- Regulatory and materials sensitivity analysis: We provide scenario-based cost modeling that ties changes in raw-material prices and evolving emissions standards to project economics, enabling CFOs and project leads to stress-test investment cases.

Core findings — the strategic implications

Three themes should define executive priorities in 2026:

Reciprocating Compressor For Oil Gas Market

- Stability with a shifting envelope: Overall market growth is moderate but stable. Procurement cycles should anticipate predictable replacement and capacity expansion activity while preparing for episodic capital demands tied to decarbonization projects and gas quality handling requirements.

- Decarbonization is a design driver: Demand is increasingly skewed toward compressors that can accept alternative gases (hydrogen blends, CO2) and that meet stricter fugitive emission limits. Engineering teams must reconcile legacy fleet constraints with modular designs and materials compatibility — an area where first-mover advantages in retrofit kits and valve technology will matter.

- Supply-chain and cost transparency is non-negotiable: Steel price stabilization in mid-2025 (in the low–mid $800s per short ton range in the U.S.) has reduced near-term input volatility, yet fabrication lead-times and alloy availability remain risk vectors for 2026 delivery schedules. Contracting strategies that combine fixed-price elements with indexed-material clauses will reduce margin leakage for both OEMs and buyers.

Report contents — what you will find inside

PW Consulting’s full report is designed as a playbook, not a narrative. Key deliverables include:

- Market sizing and forecast model with transparent methodology and assumptions for 2020–2032 (base year 2025).

- Demand-driver matrices across upstream, midstream and downstream use cases, paired with purchase-logic templates for CAPEX decision-making.

- Supplier capability maps and an OEM selection toolkit that scores vendors on reliability, service footprint, emission performance, and retrofit offerings.

- Regulatory impact assessment, including practical compliance pathways for New Source Performance Standards that affect reciprocating compressor rod packing and leak detection/repair regimes.

- Cost-sensitivity and scenario analysis integrating raw-material price paths (steel), fabrication lead-time variability, and operational fuel/gas quality changes.

- Case studies and checklists for hydrogen-readiness, valve modernization (including electronic control pockets), and lifecycle service contracts.

Competitive landscape — what to watch in 2026

The market remains moderately consolidated: the top three incumbents account for roughly a third of industry revenues, and the top five for about half. This concentration profile produces a dynamic where large OEMs set technical standards while specialty players compete on customization, service excellence, and niche applications.

Key firms profiled in the report include (representative selection):

- Ariel Corporation — A global leader in separable reciprocating gas compressors, with product breadth across high- and medium-speed platforms. Ariel’s investments in smart compression and hydrogen-capable models indicate a dual strategy of defending traditional markets while pursuing energy-transition opportunities.

- Baker Hughes — A fullstream supplier that emphasizes modular API 618-compliant machines for high-pressure services. Its engineering focus on low pulsation and maintainability positions it well for operators prioritizing reliability in demanding environments.

- Burckhardt Compression AG — Known for customized and modular systems across gas transport, storage and emerging hydrogen applications. Burckhardt’s service-centric model makes it a go-to for complex retrofits and fleet modernization projects.

- Siemens Energy (Dresser-Rand) — With dedicated reciprocating compressor facilities, the company prioritizes capacity control technologies and advanced valve systems, which are critical for performance optimization in process industries.

- Ingersoll Rand, Howden, Atlas Copco, MAN Energy Solutions, Neuman & Esser, and Borsig — Each of these players brings differentiated strengths — from oil-free compression and offshore systems to specialized engineering for hydrogen and process gases — creating a supplier ecosystem where technical fit and service coverage drive procurement choices.

Recent industry activity underscores these dynamics: new service centers and strategic exhibitions in 2025–2026 signal both market maintenance demand and a shift toward hydrogen and low-emission applications. These deployments frequently come with vendor-specific retrofit packages and service partnerships that materially affect total lifecycle cost of ownership.

Regulatory and technical dynamics shaping procurement

Executives must plan around two intersecting forces:

- Compliance-driven upgrades: Standards such as the ISO framework for reciprocating compressors and region-specific emission rules (for example, U.S. NSPS provisions for rod packing and monitoring cadence) are accelerating replacement cycles for non-compliant equipment. The report provides a prioritized upgrade roadmap tied to typical asset classes and operational profiles.

- Technology-enabled value capture: Innovations such as electronic variable clearance pockets, advanced valve materials, and monitoring-enabled predictive maintenance are delivering measurable uptime and efficiency gains. Our benchmarking shows that technology adoption choice materially changes operational expenditure profiles over a compressor’s service life.

How to use the report in your 2026 planning cycle

We designed the report as an input to four common executive workflows in 2026:

- CAPEX prioritization: Use scenario outputs to rank projects by net present value sensitivity to steel cost and lead-time risk, and to evaluate retrofit versus new-build for hydrogen readiness.

- Vendor strategy: Apply our OEM scoring model to shorten RFQ cycles and to structure service-level agreements that align supplier incentives with uptime and emissions goals.

- Supply-chain hedging: Adopt contract language templates and material-indexing options provided in the report to mitigate input-cost exposure while preserving schedule certainty.

- Regulatory compliance planning: Map your fleet to the compliant roadmap and budget for prioritized packings, seals, and monitoring upgrades to avoid enforcement or shutdown risk.

Executive recommendations — immediate actions for 2026

- Conduct a rapid fleet-screen using our 30‑point checklist to identify units at risk of non-compliance or near-term economic obsolescence.

- Shortlist vendors using the report’s capability maps and run a two-stage procurement with technical proof-of-concept for hydrogen or CO2 service before committing to long-lead procurements.

- Negotiate fixed-price fabrication bands with indexed materials clauses to protect project economics in the event of steel-price reversals or alloy scarcity.

- Invest in retrofit pilots for valve modernization and electronic-clearance controls on high-utilization assets to demonstrate measurable operating-cost reductions within 12–18 months.

Next steps and how to access full intelligence

This briefing is a strategic distillation intended to accelerate decision-making in 2026. The full PW Consulting report contains the detailed segment models, vendor scorecards, contract clause templates, and downloadable scenario models referenced here. To obtain the complete report and access our interactive forecasting toolsets, please visit the report landing page on PW Consulting’s website where you can order the full analysis and arrange advisory support.

For procurement leads, asset managers, and corporate strategists, PW Consulting offers tailored briefings and implementation workshops that translate the report’s findings into procurement documents and retrofit roadmaps — contact us to schedule a 90-minute executive workshop and receive a customized fleet-screening addendum.

PW Consulting remains committed to delivering concise, decision-ready analysis that balances transparency and proprietary depth. This briefing showcases the frameworks and strategic conclusions our clients will use to navigate the modest growth environment and structural transitions shaping the reciprocating compressor market through 2032.

For detailed analysis of this topic, please visit the official page:Reciprocating Compressor For Oil Gas Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com