Photoresist Photosensitizer Market 2026: Strategic Imperatives from PW Consulting’s Latest Analysis

As semiconductor and advanced-display supply chains enter an inflection point, photosensitizers — the small-molecule workhorses embedded in photoresists — are attracting renewed strategic attention. PW Consulting’s new market study on Photoresist Photosensitizers (base year 2025; forecast 2026–2032) synthesizes seven years of market trajectory and seven-year forecasts to equip executive teams with decision-grade intelligence as they plan 2026 investments, procurement strategies, and technology roadmaps.

Photoresist Photosensitizer Market

Market snapshot: growth with structural concentration

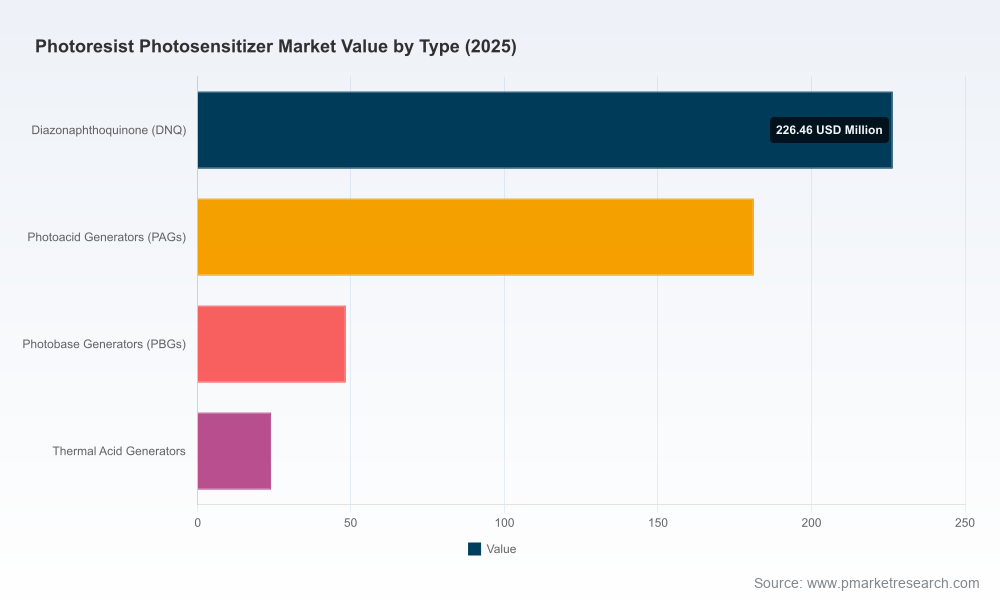

Our model shows the global photoresist photosensitizer market reached an estimated USD 480.0 Million in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 8.01% through 2032. This growth is not evenly distributed: demand dynamics are being reshaped by node migration in logic and memory fabs, accelerating uptake of EUV- and immersion-capable chemistries, and the expanding footprint of advanced packaging and heterogeneous integration. At the same time, the market remains concentrated: the top three suppliers control a clear majority of global supply, and the top five approach near-total dominance — a structural reality that should be treated as a fundamental constraint in sourcing and M&A planning.

Photoresist Photosensitizer Market

Why this report matters for 2026 decisions

- Capital allocation: With foundry and memory capex plans pushing advanced node capacity through 2027, procurement teams need to align photosensitizer offtake and supply agreements with multi-year fab ramp schedules. The report translates market growth into pragmatic volume and lead-time scenarios for 2026 planning cycles.

- Technology choices: As fabs adopt sub-5nm processes and EUV becomes more broadly standard, photosensitizer selection drives pattern fidelity and defect density. Our analysis maps the technology-performance trade-offs of leading photosensitizer chemistries and quantifies the relative importance of purity thresholds and impurity control for yield optimization at advanced nodes.

- Supply chain and regulatory risk management: Heightened scrutiny on persistent fluorinated compounds (PFAS) and ongoing export-control dynamics mean procurement and compliance teams must revisit supplier resilience, substitution pathways, and wastewater-treatment requirements. The report provides scenario-based templates to stress-test supplier continuity against regulatory shocks and trade disruptions.

What the report contains — operationally focused and decision-ready

PW Consulting’s study is designed for boardrooms and procurement war-rooms. Highlights include:

Photoresist Photosensitizer Market

- Market model and topline forecast (2020–2032) with sensitivity bands tied to fab-capex trajectories — enabling planners to test upside/downside scenarios for 2026 commitments.

- Technology-performance matrix that compares photosensitizer classes on parameters that matter to fabs: quantum yield, diffusion, acid-generation efficiency, thermal stability, and impurity risk.

- Supplier scorecards that assess manufacturing footprint, production capacity, quality systems, and geopolitical exposure — calibrated for tactical supplier selection and dual-sourcing strategies.

- Regulatory impact mapping and wastewater-treatment playbook, translating PFAS risk into compliance timelines and capital needs for effluent control.

- Sourcing and procurement playbooks: contract templates, lead-time modeling, inventory strategies, and hedge recommendations for 12–36 month cycles.

- M&A and partnership shortlists: high-probability targets and capability gaps, with financial proxies and integration risk checklists for 2026 deal pipelines.

- Executive dashboards and slide-ready artifacts for investor and board communication — all exportable to client templates.

To preserve commercial value for clients and prospective subscribers, detailed regional and application-level splits and line-item revenue tables are intentionally withheld from this public summary. The full report contains complete segmentation, unit-volume forecasts, and supplier-by-product matrices.

Competitive landscape: what the incumbents are doing

The market is led by long-established photoresist manufacturers and specialty-chemical players whose scale, IP, and fabs-aligned customer relationships form high barriers to entry. Key players profiled in our analysis include Tokyo Ohka Kogyo (TOK), JSR Corporation, FUJIFILM (including FUJIFILM Electronic Materials and Wako), Shin-Etsu Chemical, DuPont, Toyo Gosei, Merck (EMD Electronics), and a mix of regional specialty suppliers and entrants.

- Tokyo Ohka Kogyo (TOK): TOK’s recent capacity expansion for EUV-compatible resists signals a strategic doubling-down on next-node supply. Their integrated approach—formulating resists where photosensitizers are a proprietary lever—gives them a distinct advantage in co-optimizing chemistry for yield at advanced nodes.

- JSR Corporation: With the January 2026 launch of high-resolution EUV resists targeted at sub-5nm, JSR continues to push photosensitizer innovation. Expect aggressive technology licensing and close co-development with foundry partners.

- FUJIFILM Group (Electronic Materials & Wako): FUJIFILM’s portfolio depth across ArF, KrF, and immersion chemistries, combined with high-purity photosensitizer supply, positions it as a preferred partner for customers seeking end-to-end performance guarantees.

- Shin-Etsu and Merck: These players compete on scale, quality systems, and broad product breadth. Their recent product introductions for ArF immersion and other advanced use-cases underscore a push to defend share in DRAM and logic segments.

- DuPont and Toyo Gosei: Focused on differentiated chemistries and raw-material supply, these firms are pivotal to shorter lead-time sourcing and formulation tuning for advanced packaging applications.

- Specialty and regional suppliers: A cohort of smaller vendors—including European and Chinese producers—fill critical niches for research-grade, customized, or lower-capacity needs. Their role in local supply chains and research collaboration deserves attention from regional fabs and IDMs seeking supply diversity.

Our competitive scoring incorporates capacity, technical depth, IP position, regulatory exposure, and recent corporate actions. For 2026, the data suggest consolidation pressure will persist, and strategic partnerships (co-development, toll-manufacturing) will be primary mechanisms for newcomers to scale without replicating the incumbents’ capital investments.

Industry dynamics and risk vectors

- Regulatory scrutiny on PFAS: Peer-reviewed studies and regulatory signals indicate rising restrictions; reported PFOS concentrations in photoresist wastewater have triggered scrutiny in multiple jurisdictions. Firms should budget for wastewater upgrades and consider PFAS-free product roadmaps.

- Geopolitics and export controls: High-end KrF/ArF resists and associated photosensitizers remain clustered among a few Japanese suppliers, and existing export controls underscore supply-chain fragility. Strategic buyers should map geo-exposure and build contingency contracts.

- Raw-material quality constraints: Photosensitizers account for a meaningful share of photoresist raw-material volume globally, with production exceeding hundreds of thousands of kilograms per year and impurity thresholds for advanced nodes held below parts-per-million levels. This tight quality bar elevates the value of suppliers with proven ultra-high-purity manufacturing.

- EUV adoption and PAG demand: Adoption of EUV-tailored photoacid generators has accelerated, with a notable share of advanced fabs moving to specialized PAG systems. This trend creates asymmetric demand for tailored photosensitizers and creates margin opportunities for firms that can deliver node-specific solutions.

Strategic imperatives for executives in 2026

- Re-align procurement to fab timelines: Shift from annual buy-sheets to multi-year offtake arrangements that mirror fab ramps, with embedded SLAs for purity and batch-release testing.

- Invest in regulatory-proof roadmaps: Prioritize product migration plans away from at-risk chemistries and quantify capex for wastewater remediation as part of total cost of ownership (TCO) calculations.

- Pursue co-development and dual-sourcing: Use technical partnerships to de-risk node-specific photosensitizer supply while maintaining redundancy across geographically diverse suppliers.

- Embed chemistry risk in M&A and JV screens: For investors and corporate development teams, supplier concentration and PFAS exposure should be hard filters in target screening frameworks.

- Operationalize purity metrics: Integrate impurity thresholds and analytics (trace-level monitoring) into incoming-inspection protocols and supplier scorecards.

How to use the PW Consulting report

This study functions as both a strategic briefing and an implementation toolkit. Licensing the full report gives access to the complete dataset, segmentation granularity, supplier-by-product matrices, and downloadable assets for board presentations. For firms prioritizing speed to market, our consulting practice offers tailored workshops that convert report insights into executable sourcing strategies, joint-development roadmaps, or regulatory-compliance programs over a 6–12 week engagement.

To preserve the competitive utility of our analysis we have withheld detailed regional and application-specific revenue tables from this open summary. For the full dataset, supplier scorecards, and executable playbooks needed to make confident 2026 decisions, please contact PW Consulting to request the complete Photoresist Photosensitizer Market report and associated advisory services.

For detailed analysis of this topic, please visit the official page:Photoresist Photosensitizer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com