Special Airport Systems Market: Strategic Imperatives for 2026 — PW Consulting Special Report Preview

Key headlines

PW Consulting’s Special Airport Systems Market report (base year 2025) frames a decisive window for airport operators, system integrators, OEMs and investors. The market has exhibited steady expansion through the 2020–2025 historical period and is projected to grow at a compound annual growth rate (CAGR) of 6.5% across our 2026–2032 forecast horizon. By 2026 the market is forecast to surpass USD 13 billion, accelerating towards nearly USD 19.5 billion by 2032. Market concentration remains moderate: the top three vendors account for roughly a third of market revenues and the top five approach half of the ecosystem — conditions that favour both scale-driven incumbents and focused challengers with niche differentiation.

Special Airport Systems Market

Why this matters for 2026 decision-makers

- Budgeting and CapEx alignment: The 2026 fiscal year will be the first full planning cycle following major regulatory and standards updates that materially affect system specifications and lifecycle costs. Procurement timetables and multi-year funding commitments must be stress‑tested against updated compliance and throughput requirements.

- Technology transition management: Airports and integrators face synchronous upgrades across baggage, screening, airfield and passenger processing domains. Leaders who orchestrate staged, interoperable upgrades will minimize operational disruption while capturing efficiency gains.

- Competitive positioning and M&A: Moderate market concentration creates room for strategic acquisitions, carve-outs and partnerships. Buyers must evaluate target portfolios not just for installed base and revenue, but for software architectures, integration IP and compliance roadmaps.

Market trajectory — macro view (what the numbers conceal)

Our modelling, anchored on a 2025 base, synthesizes historical deployment patterns, procurement cycles, and policy shifts to project a structurally growing market. Growth is underpinned by two durable drivers: (1) passenger traffic recovery and capacity expansion pressures that keep demand for terminal and airfield systems on an upward path, and (2) regulatory and security modernisation that raises baseline requirements for new and retrofit projects.

Special Airport Systems Market

Importantly, the headline CAGR obscures material heterogeneity beneath the surface: replacement cycles, retrofit versus greenfield spend, and the share of software‑intensive solutions are evolving at different paces. The full report dissects these dynamics and maps three plausible demand scenarios with associated procurement lead times and OPEX/CapEx implications for 2026 planning.

Special Airport Systems Market

Practical contents of the PW Consulting report (what you get)

- Executive decision matrices: actionable frameworks that translate forecast trajectories into budget, procurement and vendor selection guidance suitable for CFOs and Head of Programs.

- Technology and implementation playbooks: stepwise blueprints for migrating to automated baggage handling, next‑gen security screening and digitised passenger processing with minimal operational disruption.

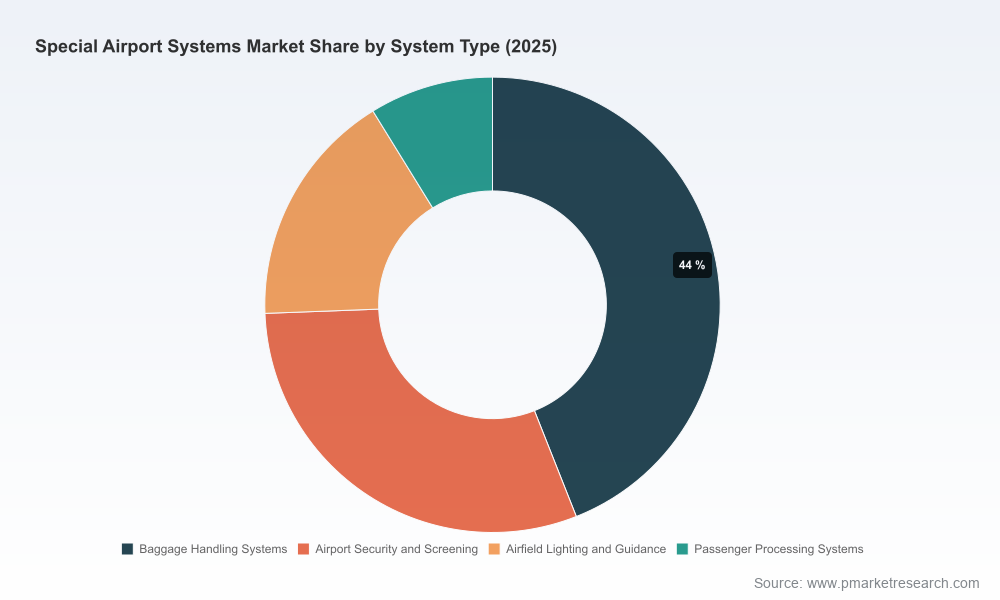

- Vendor evaluation toolkit: qualitative and quantitative scorecards for assessing systems, integration competency, support footprints and upgrade roadmaps (note: detailed segment-level shares and contract-by-contract financials are reserved for the full subscription).

- Risk register and compliance map: overlaying ICAO, IATA and national regulatory updates against project timelines to highlight gating items that must be resolved before contract award.

- CapEx optimisation templates: TCO models that reconcile lifecycle maintenance, software licence trajectories and retrofit premiums to help asset owners prioritise investments through 2032 horizons.

Competitive landscape — what incumbents and challengers signal for 2026

The competitive terrain features global systems integrators, specialised automation OEMs, and established defence/aerospace players adapting to civilian airport needs. Our strategic review covers leading names whose footprints and recent activity materially influence tender outcomes and customer expectations.

- Honeywell International Inc. — Positioned as a cross‑domain systems supplier, Honeywell’s strength is in combining security screening, building management and ground operations technologies into integrated service offers. For large airports seeking consolidated lifecycle contracts, Honeywell’s holistic approach remains compelling.

- Thales Group — Thales continues to leverage its air traffic management and security solutions pedigree. Its integrated approach to baggage and navigation systems makes it a logical partner for complex, multimodal upgrade programmes where systems interoperability is a priority.

- Vanderlande Industries & Daifuku — Specialists in high‑throughput automated baggage handling, these players remain central to terminals planning aggressive capacity upgrades. Their engineering depth and project track records shape tender expectations for automation performance and reliability.

- SITA & Amadeus — As the principal providers of passenger processing and airport IT, these firms define the standards for seamless passenger flows. Their platforms increasingly act as the integration layer tying together disparate physical systems into coherent operational dashboards.

- Leidos & RTX (Raytheon Technologies) — Firms with strong security and surveillance portfolios are influencing the security architecture choices of airports. Recent joint ventures and partnerships underscore a trend toward coalition strategies for delivering complex, security‑sensitive projects.

- Siemens, Indra Sistemas, Leonardo and ADB SAFEGATE — These vendors bring expertise across building automation, air traffic management, baggage systems and airfield lighting; their diverse capabilities make them frequent participants in consortium bids for large airport modernisations.

- Engineering and integrator specialists (IDOM, Deerns) — As airports outsource complex design and systems integration tasks, engineering firms that can knit together diverse systems with rigorous compliance credentials are in rising demand.

Notable recent moves — documented in our industry monitoring — include contract wins and strategic partnerships that reconfigure capability sets and bid consortiums. These developments, while not exhaustive here, are analysed in depth in the report to show how they change competitive dynamics for 2026 tenders.

Regulatory and programmatic catalysts shaping 2026 choices

- IATA standards updates: The 2026 editions of core handling manuals introduce near‑term changes to baggage handling and ground operations that materially affect system acceptance criteria and service level agreements.

- ICAO security evolution: Amendments to Annex 17 and the expansion of “One‑Stop Security” concepts create opportunities for integrated screening solutions but also impose new certification pathways for suppliers and airports.

- National safety deployments: Targeted national programmes — for example, planned runway safety technology rollouts — create pockets of accelerated demand and integration complexity that vendors must navigate.

For 2026 procurement teams, the intersection of these regulatory shifts with capital plans creates a narrow window to reprioritise scopes, update specifications and renegotiate delivery timelines.

Strategic recommendations — a pragmatic 9‑to‑18 month playbook

- Reframe procurement around interoperability and software lifecycle: Require open APIs, modular upgrade paths and vendor commitments to software maintenance to avoid costly rip‑and‑replace cycles.

- Adopt phased rollouts tied to operational milestones: Align physical upgrades with passenger flow targets to preserve revenue generation during works and reduce rework risk.

- Stress‑test vendor supply chains: Given ongoing geopolitical and component lead time risks, include supplier resilience clauses and multi‑source options in RFPs.

- Prioritise cybersecurity and data governance: As airport systems converge on shared IT platforms, mandate threat modelling and incident response capabilities as part of acceptance criteria.

- Explore partnerships and JV models: For complex, security‑sensitive programmes, consortium approaches that pair global vendors with local engineering partners often deliver better risk allocation and execution certainty.

- Plan for regulatory delta: Build contingency allowances for compliance-driven scope changes and allocate a governance cell to engage with regulators and testing authorities early in the design phase.

How PW Consulting’s report supports 2026 execution

Our Special Airport Systems Market report translates market-level forecasts and industry intelligence into execution-ready guidance. It contains vendor scorecards, procurement templates, project scheduling overlays and a scenario-based forecast that lets CFOs and programme directors model alternative trajectories. The document is intentionally prescriptive: it maps decision points to specific actions calendarised for 2026 budget cycles.

Next steps — essential actions for stakeholders

- Airports: Initiate immediate audits of existing contracts against the updated IATA/ICAO frameworks and begin vendor dialogues to lock in integration and software SLAs for 2026 rollouts.

- Vendors and integrators: Reassess product roadmaps for compliance and interoperability; accelerate partnerships to fill gaps in service delivery and systems integration capacity.

- Investors and M&A advisors: Prioritise targets with durable installed bases, upgradeable software stacks and demonstrated ability to win consortium bids for large modernisation programmes.

Conclusion

2026 will be a pivotal year in the evolution of special airport systems. The market is growing on a stable trajectory, regulatory and technological shifts are forcing re‑specification of solutions, and competitive dynamics favour both scaled incumbents and highly focused specialists. Our report is designed as a practical decision accelerator: it exposes the tactical levers that determine project success while preserving proprietary segment and contract-level detail for subscribers who require the full analytical depth.

Accessing the full intelligence

PW Consulting’s Special Airport Systems Market report includes comprehensive segment-level forecasts, detailed vendor benchmarking, and downloadable implementation toolkits. For organisations preparing budgets, tender strategies or M&A playbooks for 2026, the full report provides the data and templates necessary to convert market insight into operational advantage.

For detailed analysis of this topic, please visit the official page:Special Airport Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com