Platinum‑Rhenium Catalysts Market — Strategic Outlook for 2026

PW Consulting today releases a focused industry brief accompanying our upcoming Platinum Rhenium Catalysts Market report, designed to equip C‑suite leaders, strategy teams, and procurement heads with the strategic perspective required for decisive action in 2026. The market reached an estimated USD 520.0 Million in 2025 and, under our base forecast, is projected to expand at a compound annual growth rate (CAGR) of approximately 4.1% through the 2026–2032 horizon, reaching roughly USD 689 Million by 2032. These headline metrics frame a market that is mature, structurally concentrated, and increasingly sensitive to raw material dynamics and regulatory attention.

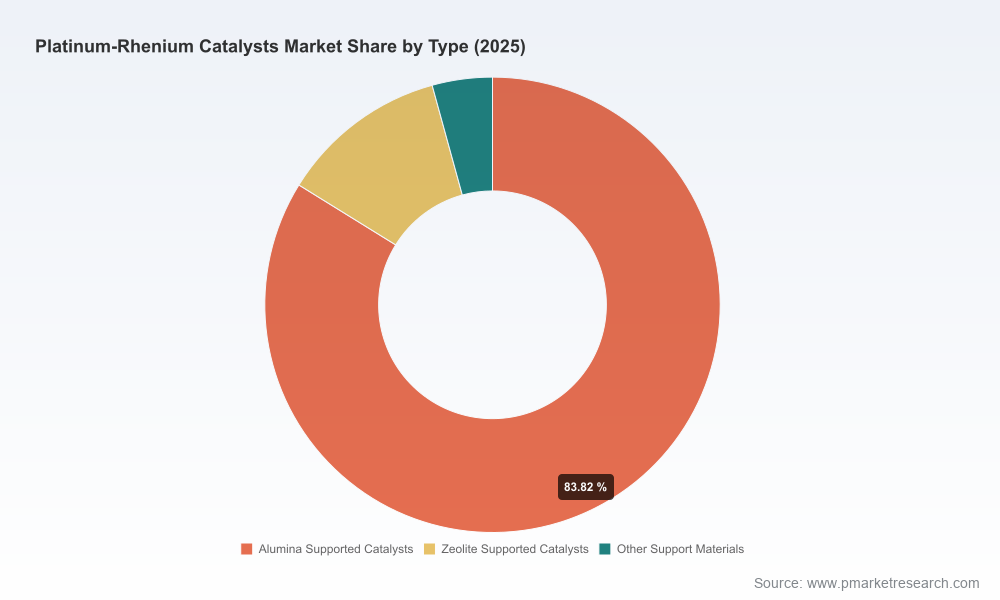

Platinum Rhenium Catalysts Market

Why this matters to executives in 2026

- Price volatility in rhenium feedstocks and concentrated supply chains are changing the economics of platinum‑rhenium systems — decisions taken this year on supply contracts, recycling, and technology investments will materially affect margin and continuity through the next planning cycle.

- Market concentration among a small set of incumbent catalyst producers creates both dependency risks and strategic partnership opportunities; competitive moves by any of the major players can rapidly alter access to patented formulations and closed‑loop recycling networks.

- Regulatory classification of rhenium as a critical mineral, together with growing sustainability mandates, is accelerating the commercial value of recycling and material‑efficient catalyst technologies.

Drivers, headwinds and the near‑term shock factors

Demand fundamentals remain driven by downstream refinery and petrochemical optimization programs that prioritize yield and octane management, as well as specialty chemical syntheses that rely on platinum‑group activity. However, the supply‑side story is dominated by raw material dynamics. In 2025, catalytic‑grade ammonium perrhenate averaged materially higher prices versus the prior year, and rhenium metal pellet pricing experienced an even larger uptick. These sharp moves — alongside modest increases in primary production reported from key jurisdictions — have created an acute focus on feedstock availability and cost pass‑through.

Platinum Rhenium Catalysts Market

Concurrently, industry practice around spent catalyst management is evolving into tighter closed‑loop networks where producers, refiners and recyclers co‑manage flows. This transition reduces net primary demand but raises strategic stakes around control of return streams, proprietary reprocessing techniques, and value capture in recovery. Finally, regulatory recognition of rhenium as a critical mineral has implications for trade policy, stockpiling, and incentive structures that will inform capital allocation choices in 2026.

Platinum Rhenium Catalysts Market

Competitive landscape — who matters and why

The market is meaningfully concentrated: the top three global players account for a majority share of commercial supply, while the top five control nearly four in five dollars of the market. This concentration shapes negotiating leverage, technology access, and the geographic footprint of supply chains.

- Johnson Matthey (London) — A longstanding leader in precious‑metal catalysis, JM combines manufacturing scale with recycling and licensing capabilities. Its breadth across refinery‑scale reforming catalysts and aftermarket services gives it a high degree of influence on commercialization of new formulations.

- BASF (Ludwigshafen) — As a global catalyst business with deep integration into refinery and chemical process licensing, BASF’s platinum‑rhenium offerings play in both semi‑regenerative and cyclic reforming segments. Their ability to bundle catalyst supply with process engineering is a differentiator for large refiner customers.

- Umicore (Hoboken) — Competing on high‑performance formulations and a strong recycling footprint, Umicore’s precious metals chemistry capabilities allow it to propose end‑to‑end metal management solutions that reduce net raw‑material exposure for clients.

- Heraeus Precious Metals (Hanau) — A specialist in supported Pt/Re systems and recycling logistics, Heraeus has recently signaled strategic collaboration beyond traditional customers; notably, a mid‑2025 strategic partnership with an automotive OEM underscores cross‑industry interest in platinum‑group metal solutions.

- Clariant (Muttenz) — Focused on niche catalyst chemistries and tailored service models, Clariant competes on formulation agility and process integration for petrochemical customers.

- AVANT (Shandong) and Vineeth Precious Catalysts (Mumbai) — Regional manufacturers and reprocessors that provide scale and localized service models, increasingly relevant for cost‑sensitive markets and for customers pursuing supplier diversification.

For incumbents, the strategic playbook ranges from defending aftermarket relationships to integrating recycling innovations. For new entrants or downstream buyers, the game is access: access to secure feedstock, access to recycling capacity, and access to proprietary catalyst know‑how.

What the PW Consulting report delivers — practical modules

We designed the full report to be a transaction‑ready, operational tool rather than a purely descriptive market study. Key deliverables include:

- Transparent market sizing and forecast model (historical 2020–2025 and forward projections to 2032) with scenario toggles for raw material price shocks and substitution pathways.

- Supply‑chain heat maps showing points of concentration, recycling flows, and choke points for rhenium and platinum supply.

- Price‑sensitivity and margin models that link APR/rhenium price scenarios to catalyst BOM cost and recommended commercial pass‑through strategies.

- Competitive benchmarking of technology, services (manufacturing, licensing, recycling), and commercial terms across the major producers and selected regional suppliers.

- Deal pipeline assessment and M&A target screening, with valuation ranges and integration risk scorecards for asset acquisition, joint ventures, or strategic partnerships.

- Operational playbooks for procurement and catalyst lifecycle optimization — including tender templates, contract clauses for material price escalation, and approaches to secure return‑stream control.

- Primary research appendices summarizing interviews with refinery engineering leads, catalyst procurement officers, and recycler operators.

To preserve proprietary value and to respect commercial sensitivity, the report presents granular segmentation and regional splits in interactive tables behind a gated data workbook — a deliberate choice to ensure clients who require the full depth receive it through a controlled engagement.

Strategic recommendations for 2026 decision cycles

- Embed raw‑material scenario planning into your 2026 budgeting process. Run stress tests that incorporate short‑term spikes similar to those observed in 2025 for APR and rhenium pellets, and quantify the impact on product margins and operating cash flow.

- Prioritize partnership models that secure recycled rhenium flows: invest in or contract with recyclers, negotiate long‑term take‑back agreements, or explore tolling arrangements with smelters to reduce exposure to spot market volatility.

- For refiners and large end‑users, consider multi‑supplier sourcing and technical lock‑ins (e.g., licensing agreements or exclusive reprocessing) to balance cost and continuity risks while preserving access to high‑performance formulations.

- For catalyst producers, accelerate differentiation through support‑material innovation, lifecycle services, and digital monitoring to extend cycle life and improve yield — these levers reduce net metal intensity and buffer price swings.

- Assess targeted M&A or minority investments in regional reprocessors and specialty formulators to capture upside from recycling arbitrage and localized service demand.

- Engage with policymakers and industry consortia where classification as a critical mineral creates options for strategic stockpiling, incentives, or priority access programs.

How PW Consulting can support your 2026 response

Our advisory work combines front‑line industry contacts, proprietary pricing models, and transaction experience across commodities, chemicals, and catalysts. We offer modular engagements that range from a focused procurement playbook and scenario modeling to full due diligence and negotiation support for strategic partnerships or bolt‑on acquisitions. For clients needing rapid insight, we provide an executive briefing pack derived from the full report, plus a live model that can be re‑run with client‑specific inputs.

PW Consulting’s Platinum Rhenium Catalysts Market report is intentionally structured as both a strategic primer and a transaction‑grade toolkit. The preview above highlights the principal forces that will shape 2026 decisions: elevated raw‑material volatility, concentrated supply, regulatory attention, and the pivot to closed‑loop recycling. For executives weighing capital allocation, procurement commitments, or partnership structures this year, timely access to the report’s segmented forecasts, supplier scorecards, and price‑sensitivity matrices will be decisive.

To access the full report, including detailed regional and application segmentation, interactive financial models, and the confidential data workbook, please visit our report page or contact PW Consulting’s Industrial Materials practice for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Platinum Rhenium Catalysts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com