PW Consulting: Strategic Brief — Used and Refurbished Medical Devices Market (2026 Outlook)

Executive Summary

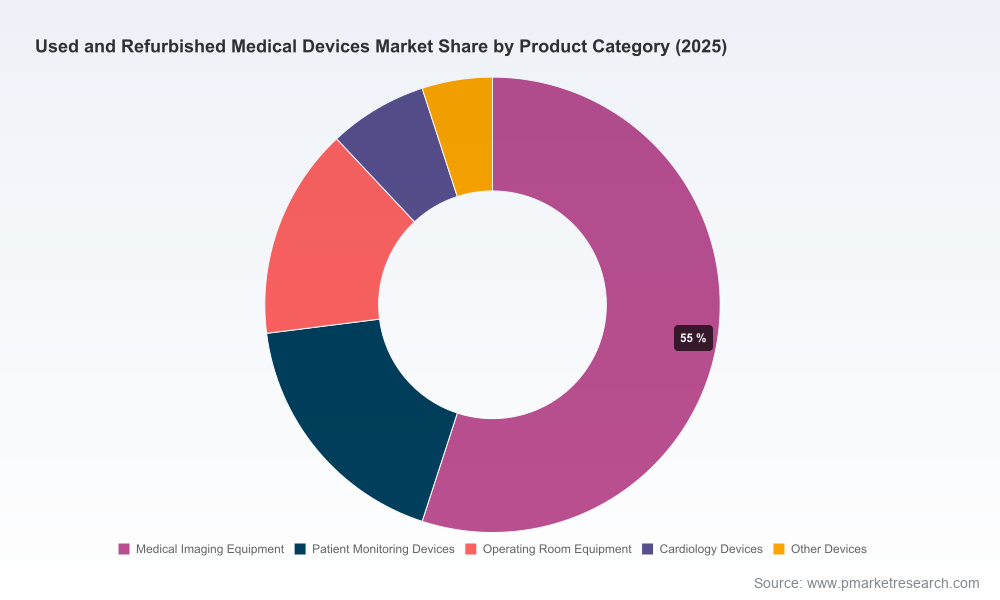

PW Consulting’s new market research brief on the Used and Refurbished Medical Devices Market synthesizes seven years of historical context (2020–2025) and a robust seven‑year forecast horizon (2026–2032) to equip senior leaders with the evidence and scenario thinking required for 2026 strategic decisions. Using USD as the reporting currency and Million as the revenue unit, the market is valued at an estimated USD 17,250 Million in the report’s base year of 2025 and is projected to grow to approximately USD 36,267.9 Million by 2032 — a compound annual growth rate (CAGR) of 11.2% over the forecast period. The market shows moderate concentration with the top three players controlling roughly 38.5% and the top five about 52.3% of the market, signaling both established OEM and independent-refurbisher influence and room for challengers.

Used And Refurbished Medical Devices Market

Why This Brief Matters for 2026 Decision-Makers

- Actionable timing for capital planning: The high‑teens CAGR trajectory through 2032 means procurement and CapEx plans drafted in 2026 will have to account for a maturing secondary market that can materially displace or complement new‑equipment budgets.

- Regulatory inflection: Recent regulatory clarifications and the emergence of Quality Management System Regulation (QMSR) create new compliance thresholds that directly affect sourcing, refurbishment workflows, and liability exposure. Procurement, legal, and clinical engineering teams must align now to avoid retrofitting compliance frameworks later.

- Commercial leverage and service economics: As refurbished offerings approach OEM performance and warranty profiles, commercial models — from pure asset resale to integrated as‑a‑service and managed equipment programs — will determine which players scale sustainably.

- ESG and reimbursement dynamics: Sustainability benefits and value‑based care incentives are increasingly linked to procurement choices; organizations that quantify lifecycle emissions and total cost of ownership (TCO) will have a competitive edge in payer and system negotiations.

What the Report Contains (Practical, Non‑Proprietary Highlights)

PW Consulting’s full report is structured to serve both the strategist and the practitioner. Highlights include:

Used And Refurbished Medical Devices Market

- Market sizing and trajectory: historical analysis (2020–2025) and seven‑year forecasts (2026–2032) expressed in USD Million, including scenario variants tied to regulatory and macroeconomic stressors.

- Market structure and concentration dynamics: measures of competitive intensity, entry barriers, and vertical integration pressures that explain why the market is neither fully commoditized nor exclusively OEM‑controlled.

- Operational playbooks: step‑by‑step checklists for integrating refurbished devices into hospital fleets, including procurement requirements, acceptance testing, service‑level templates, and warranty structuring.

- Commercial modules: negotiated pricing frameworks, lifecycle services, and bundling tactics that protect margins while preserving clinical confidence.

- Regulatory and quality compliance guide: an applied interpretation of recent FDA guidance and the QMSR, with decision trees for distinguishing servicing vs. remanufacturing, and a risk matrix for when OEM involvement is required.

- Scenario modeling assets: modular forecasting models that allow executives to test the impact of procurement shifts, reimbursement changes, and regulatory tightening on revenue and EBITDA.

- Competitive profiles: strategic positioning and capability assessments for leading providers in the refurbished space, with implications for partnerships, M&A targets, and white‑label opportunities.

Competitive Landscape — What We Learned

The competitive set combines legacy OEMs expanding certified refurbished programs and specialized independent refurbishers. Key archetypes include:

Used And Refurbished Medical Devices Market

- OEM‑led certified programs: Major global players are packaging refurbished systems under branded, warranty‑backed programs that emphasize OEM‑comparable performance, certified processes, and sustainability narratives. These programs seek to protect brand integrity while capturing price‑sensitive demand.

- Independent multi‑vendor specialists: Independent refurbishers offer multi‑vendor, often lower‑cost solutions with deep spare‑parts networks and flexible service contracts — attractive to system integrators and regional hospital networks.

- Service‑oriented aggregators: Firms combining rental, refurbishment, and biomedical services are winning share by offering on‑demand capacity without the need for large capital outlays.

Representative names analyzed in the report include established OEM programs and high‑competency independents. Each is profiled with respect to value proposition, refurbishment process rigor, warranty and service models, go‑to‑market approaches, and partnership appetites. These profiles serve as starting points for alliance mapping, procurement negotiations, and M&A screening.

Regulatory and Operational Headwinds — What to Watch in 2026

- QMSR and FDA enforcement dynamics: With the QMSR effective in early 2026 and the 2024 FDA guidance clarifying remanufacturing vs. servicing, organizations must reassess where refurbishment activities sit on the compliance spectrum. Remanufacturing that materially changes device performance will increasingly be treated as manufacturing — with full regulatory obligations.

- Premarket and postmarket obligations: In jurisdictions where remanufacturing triggers premarket requirements, refurbished systems may require clearance comparable to new devices. This affects time‑to‑market for higher‑risk categories and raises the bar for documentation and traceability.

- Procurement and contracting implications: Hospitals must update acceptance criteria, contracting templates, and vendor audits to reflect new compliance expectations, otherwise they risk operational disruptions and potential regulatory citations.

Market Drivers and Strategic Opportunities

The brief synthesizes market drivers that have practical, decision‑grade implications for 2026:

- Tight hospital CapEx and the need for capacity: Health systems under capital pressure are increasingly turning to refurbished equipment to expand diagnostic and therapeutic capacity while trimming up‑front spend. Typical procurement programs can deliver significant immediate cost savings versus new purchases where the clinical need, throughput, and service profile align.

- Sustainability as a procurement lever: Certified refurbished systems can deliver measurable lifecycle emissions reductions. Quantifying these savings allows procurement teams to align with system‑level ESG targets and to differentiate bids in public tenders.

- Service economics and lifecycle revenue: There is a growing avenue for capturing aftermarket revenue through managed services, spare parts, and upgrade packages — often with higher margins than initial hardware sales.

- Consolidation and bolt‑on M&A: Independent refurbishers and regional service firms are attractive bolt‑on targets for both OEMs and private equity sponsors seeking to scale distribution and service footprints quickly.

Risks, Uncertainties, and Mitigations

- Regulatory reclassification risk: Should regulators tighten the definition of remanufacturing, some refurbishment models may require retroactive compliance efforts. Mitigation: adopt ISO 13485 aligned QMS elements now and maintain robust device history records.

- Perception and clinician acceptance: Clinical stakeholders may be skeptical of refurbished systems for high‑acuity use. Mitigation: emphasize standardized testing protocols, OEM‑equivalent warranties, and pilot deployments with KPI measurement.

- Supply chain and parts availability: Aging device platforms face parts scarcity. Mitigation: establish long‑term parts agreements, prioritize upgrades compatible with common modules, and evaluate third‑party parts strategies within regulatory constraints.

How Executives Should Use This Brief in 2026

For CEOs, CFOs, CMOs, and heads of procurement and clinical engineering, this PW Consulting brief is designed to be directly operationalized:

- Use scenario models to stress‑test capital plans and determine the optimal ratio of new vs. refurbished purchases for your asset mix.

- Deploy the regulatory compliance checklist to audit refurbishment vendors and to determine when OEM involvement is necessary to avoid remanufacturing exposure.

- Apply the supplier assessment templates in vendor RFPs to standardize quality, service, and sustainability metrics across bids.

- Use the competitive profiles and M&A screening criteria to identify strategic partners, acquisition targets, or white‑label opportunities aligned with your growth and margin objectives.

Recent Developments and What They Mean

- FDA QMSR effective 2026: elevates quality expectations for refurbishment processes and makes ISO 13485 alignment a practical advantage for suppliers.

- FDA guidance (2024): clarifies the servicing vs. remanufacturing distinction — a crucial interpretive tool for legal and operational teams evaluating refurbishment scope.

- Sector M&A activity in 2026: recent acquisitions in regional refurbisher networks underscore continued consolidation — a trend that accelerates scale advantages for service and parts logistics.

Next Steps — Where to Find the Full Analysis

This briefing is a strategic preview designed to surface decision‑critical insights while preserving the detailed segment forecasts, vendor benchmarking matrices, and downloadable modeling templates available only in the full PW Consulting report. The full report contains granular, region‑and‑product level forecasts, procurement checklists, and editable Excel models you can use in boardroom discussions and budget cycles. To access the complete analysis, strategic toolkits, and vendor playbooks, please visit our report page or contact PW Consulting’s industry desk directly.

About PW Consulting

PW Consulting is a strategy advisory firm specializing in healthcare market intelligence, commercial due diligence, and operational playbooks for medical technology and health systems. Our industry teams combine regulatory, clinical, and commercial expertise to deliver pragmatic insights that translate into measurable action.

For detailed analysis of this topic, please visit the official page:Used And Refurbished Medical Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com