Throttle Position Sensors (TPS) Market Set for Strong Growth, Reaching USD 4.73 Billion by 2034

Film |

2026-06-12 10:19:33

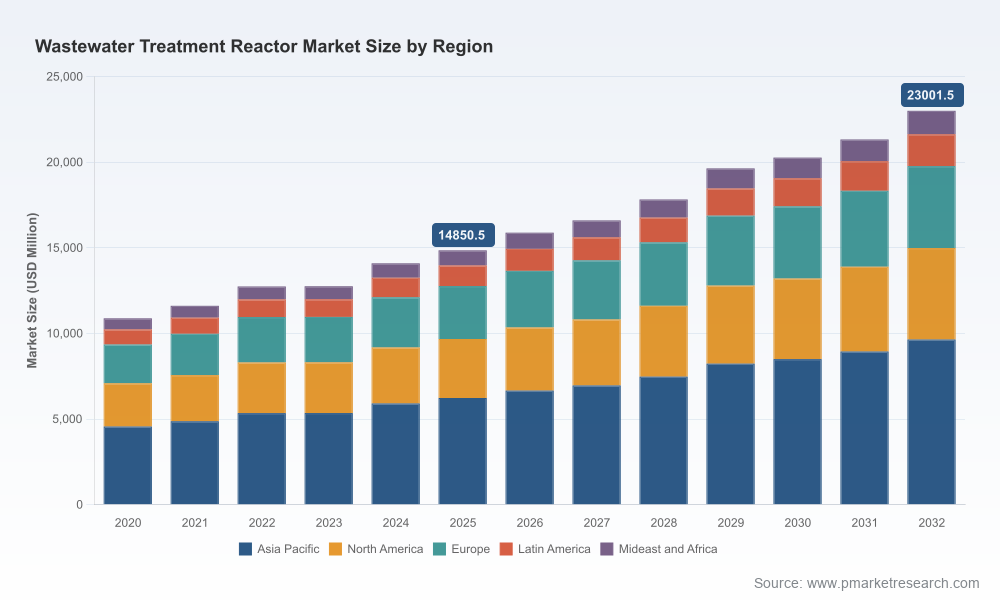

PW Consulting’s latest Wastewater Treatment Reactor Market report (base year 2025; forecast 2026–2032) is crafted as a practical decision-support playbook for utilities, industrial end‑users, technology vendors, investors, and policy teams planning capital allocation or technology roadmaps in 2026. The global market for wastewater treatment reactors crossed a notable size threshold in 2025 and is projected to grow at a steady 6.45% CAGR through 2032, driven by regulatory tightening, water reuse mandates and the accelerating commercialization of membrane and advanced biological systems. Our analysis combines rigorous market sizing, primary interviews, vendor benchmarking and scenario modelling so stakeholders can convert macro trends into executable actions — while we intentionally preserve the granular segment tables behind a single-source paywall to protect clients’ competitive advantage.

Wastewater Treatment Reactor Market

Regulatory acceleration: Heightened limits on nutrient discharge and increasing scrutiny of emerging contaminants such as PFAS are reshaping procurement specifications for municipal and industrial plants. Expect regulators to prescribe tighter performance thresholds and monitoring regimes that favor advanced biological reactors (e.g., MBR, SBR) integrated with oxidation and membrane polishing stages.

Wastewater Treatment Reactor Market

Policy-driven reuse and ZLD: Jurisdictions are moving from “encourage reuse” to enforceable reuse targets and zero‑liquid discharge (ZLD) frameworks. That structural shift is raising the strategic priority of membrane-enabled reactor designs and hybrid chemico-biological trains in industrial projects where water scarcity or regulatory compliance is non-negotiable.

Wastewater Treatment Reactor Market

Input-cost volatility: Chemical dosing remains a material line‑item for biological operations. Since 2022 acrylamide pricing has exhibited quarter-to-quarter volatility, and biodegradable membrane alternatives command significant price premiums. These cost realities are forcing operators to re-evaluate TCO, favoring capital investments that lower ongoing chemical and sludge management expenses.

Consolidation and capability-build: The competitive landscape is active — acquisitions and targeted facility launches in 2024–2025 have signaled vendor moves to secure modular packaged plants, PFAS remediation capability and decentralized solutions. Our report documents recent strategic moves and maps which acquirers have strengthened which capabilities.

This report is organized to support pragmatic 12–36 month decision cycles. Key deliverables include:

Robust market sizing and growth scenarios: Historical reconstruction (2020–2025) and a forward projection through 2032, including base, upside, and downside cases that reflect regulatory upticks and material-price shocks. These scenarios equip CFOs and investment committees to stress-test CAPEX plans.

Technology deep dives: Comparative assessments of biological reactor types and membrane integrations, with techno-economic break‑downs on lifecycle OPEX drivers (energy, membranes, chemicals, sludge handling) and switching costs to greener membrane alternatives.

Vendor benchmarking and capability matrices: A structured scorecard covering engineering depth, aftermarket networks, modular packaged solutions, intellectual property and recent corporate developments — designed to shorten vendor selection cycles and reduce procurement risk.

Operational playbooks: Real-world retrofit and greenfield decision trees, procurement templates, O&M optimization checklists, and performance KPIs tailored for municipal vs industrial operators.

M&A and partnership roadmap: Identification of consolidation targets, joint‑venture archetypes and integration risks for strategic acquirers. The section highlights where bolt‑on assets (membrane suppliers, advanced oxidation units, PFAS polishing systems) deliver asymmetric value.

Case studies and investment-ready models: Multi‑phase project examples that illustrate funding structures, off‑taker contracts, and lifecycle modelling suitable for private-equity, infrastructure funds and utilities.

The wastewater treatment reactor sector remains fragmented, with the top three players accounting for under one‑fifth of market revenue and the top five failing to command a dominant share. This market concentration profile leaves room for both scale‑driven consolidation and niche specialists to capture value through technology differentiation. In our vendor review we profile market leaders and strategic challengers, including (not exhaustive):

Veolia Water Technologies (Saint‑Maurice, France) — Deep membrane and packaged-reactor expertise; notable for ultrafiltration platforms and integrated treatment lines for municipal and industrial clients.

SUEZ (La Défense, France) — Broad portfolio across membranes, ion-exchange and advanced oxidation; strong systems integration capability for complex industrial effluents.

Xylem Inc. (Rye Brook, NY, USA) — Differentiates on hydraulic equipment and energy‑efficient pumping/mixing systems synergistic with reactor performance improvements.

Evoqua Water Technologies (Pittsburgh, PA, USA) — Focused on packaged solutions and membrane-enabled reactor lines for industrial clients.

Aquatech, Ovivo, Smith & Loveless, Kubota and others — A mix of niche industrial specialists and global system integrators offering solutions from zero-liquid discharge to operator‑friendly packaged MBR systems.

Our procurement scorecards compare these suppliers across project delivery speed, total installed cost, aftermarket density, and technology roadmaps — tools we recommend buyers use to accelerate vendor short‑listing in 2026.

Facility & capability launches: Large-scale PFAS treatment installations and membrane-polishing facilities launched in 2025 are changing performance baselines for remediation contracts and municipal procurement specifications.

Strategic acquisitions: Transactions announced in 2024–2025 indicate acquirers are prioritizing packaged reactor systems, decentralized solutions and membranes as key capability bets.

Utility capital programs: A wave of U.S. municipal upgrades for biological reactors and nutrient removal scheduled into 2026 creates near-term deal flow opportunities for modular suppliers and EPCs with rapid deployment credentials.

Input-price shocks: Chemical and membrane price volatility materially alters operating economics; sensitivity analysis in the report quantifies breakpoints where greener (but costlier) membranes become net‑beneficial.

Regulatory timing: Uncertainty in permit issuance and evolving PFAS thresholds can delay project paybacks. Scenario pathways in the report recommend staging investments to align with likely regulatory trajectories.

Technology obsolescence: Rapid adoption of hybrid treatments (membrane + advanced oxidation) increases the risk of stranded assets for plants built to older specifications; our retrofit playbook addresses phased upgrades to manage this risk.

Based on our synthesis of market forecasts, vendor capabilities and regulatory dynamics, PW Consulting recommends the following priority actions for different stakeholders in 2026:

Utilities: Prioritize modular, membrane-capable upgrades for plants with reuse or nutrient-removal mandates. Use staged contracting to preserve price optionality for membranes and chemicals as markets evolve.

Industrial operators: Design for ZLD or partial reuse from day one if your sector has high water intensity or tough effluent constituents; evaluate lifecycle comparisons that include sludge disposal and chemical costs, not just CAPEX.

Vendors & EPCs: Build pre-qualified supply bundles (membrane + advanced oxidation + automation) and strengthen aftermarket networks — faster O&M response and predictive service will be a decisive tender criterion in 2026.

Investors & acquirers: Target firms with modular packaged plants, PFAS/advanced oxidation patents, or strong cross‑sell positions into utility upgrade pipelines. Our M&A heatmap highlights where valuation arbitrage is most likely.

Clients consistently tell us they need intelligence that bridges strategy and execution. This report integrates high‑frequency market tracking with on‑the‑ground interviews (operators, engineers, procurement leads), a detailed vendor scorecard and project-level financial models suitable for board-level decision-making. We deliver not just the “what” but the “how” — next‑best moves, procurement templates and implementation milestones you can act on in 2026.

In keeping with PW Consulting’s “preview” principle, this public summary demonstrates the report’s analytic depth and immediate relevance for 2026 planning while withholding full granular segmentation tables, regional split figures and detailed revenue-by-technology cells that constitute the competitive intelligence core of the study. These detailed datasets and vendor-level scorecards are available through the full report and are intended to be used under confidentiality terms so that subscribing organizations retain their strategic advantage when executing procurement or M&A strategies.

Shortlist opportunities: Use the report’s scenario filters to identify near-term procurement windows and vendor matches aligned to your risk tolerance.

De-risk projects: Apply our sensitivity templates to quantify the impact of membrane premium or chemical-price shocks on project IRR.

Accelerate sourcing: Leverage the vendor scorecards to compress vendor evaluation timelines from months to weeks for critical upgrades and emergency replacements.

Inform capital plans: Integrate our base and stress-case projections into 3–5 year CAPEX and lifecycle OPEX models.

For procurement teams, technology strategists and investors preparing actions in 2026, the full PW Consulting Wastewater Treatment Reactor Market report provides the proprietary segment detail, vendor matrices and financial models required to execute with confidence. Contact PW Consulting to obtain the complete dataset and bespoke advisory support tailored to your market and technical needs.

For detailed analysis of this topic, please visit the official page:Wastewater Treatment Reactor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com