Steel Rebar Market: Size, Share, and Growth Forecast 2025 –2032

Gardening |

2026-06-17 09:05:48

PW Consulting’s latest Gan Wafers Market study (base year 2025; historical window 2020–2025; forecast 2026–2032) delivers the decision-grade intelligence executives and investors need to shape strategies in 2026 and beyond. Our independent model shows an accelerated expansion trajectory: the market has more than doubled in five years to 2025 and — under our central case — is set to grow at a compounded annual growth rate (CAGR) of 18.5% through 2032. That pace implies a multi‑billion‑dollar market opportunity by the end of the forecast, driven by penetration across power electronics, RF and emerging optoelectronics use cases.

Gan Wafers Market

Technology scaling is converging with commercial demand. Recent milestones in wafer scale-up and new substrate approaches are reducing entry barriers for high-volume device manufacture, but they also raise timing and capital deployment questions for both incumbents and challengers.

Gan Wafers Market

Supply‑side volatility has moved from a commodity issue to a strategic vulnerability. Trade and raw‑material dynamics — notably policy actions affecting gallium flows and step changes in average unit costs — are already forcing procurement redesigns and upstream hedging strategies. The US net dependence on imports through 2025, and recent policy movements in major producing markets, create a structural emphasis on supplier diversification and vertical resilience.

Gan Wafers Market

Competitive positioning is in flux. A measured level of concentration at the top of the value chain has left room for regional champions and specialized technology players to capture differentiated value if they can execute on capacity scaling, quality, and ecosystem partnerships.

This report was written for executives who must make binding choices in 2026: where to allocate CapEx, which technology bets to place, which partners to prioritize, and how to hedge supply and regulatory risk. Key deliverables include:

Robust market sizing and forecasts (2020–2032) with transparent methodology and scenario variants that stress-test outcomes under alternative demand and supply assumptions.

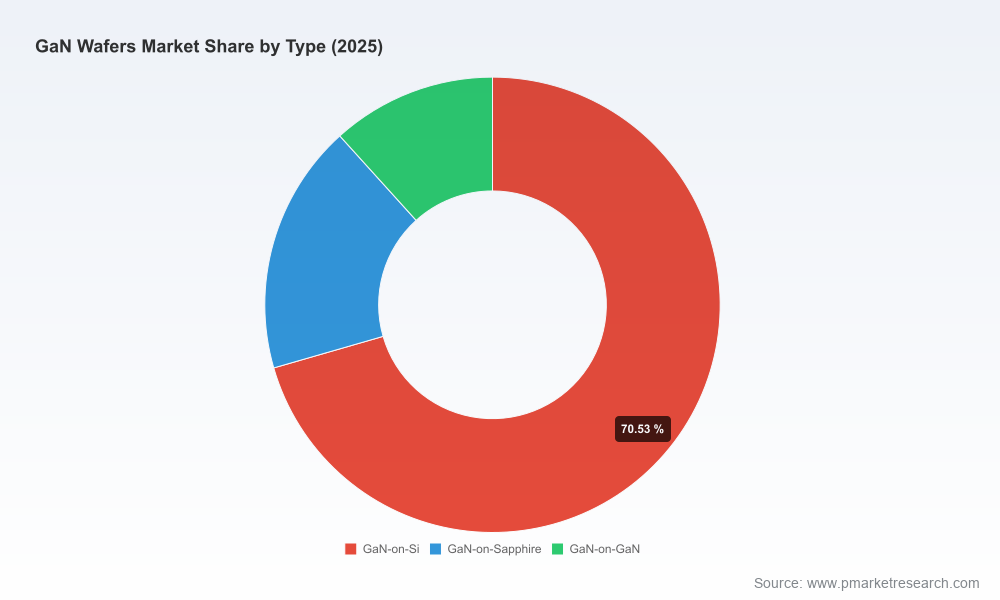

Supply-side mapping and capacity model that ties manufacturing modalities (bulk GaN, epi on silicon, sapphire, SiC, and engineered substrates) to realistic ramp timelines and cost curves.

Technology roadmaps highlighting the maturation path for critical processes (HVPE, MOCVD epitaxy, liquid‑phase growth, 300mm scaling) and their implications for yield, unit costs and device performance.

Risk-adjusted investment playbooks for device OEMs, substrate suppliers, foundries and wafer fabs, with suggested staging of CapEx and thresholds for committing to full-scale production.

Go-to-market and partner strategies, including an actionable M&A target framework and due-diligence checklist tailored to wafer- and epi‑foundry transactions.

Procurement and inventory strategies informed by raw material volatility scenarios and regulatory stress tests — practical templates for hedging gallium exposure and securing long‑lead items.

The ecosystem contains a mix of vertically integrated substrate manufacturers, epi‑wafer specialists, and service‑oriented foundries. Our analysis profiles each major participant, contrasts their strategic advantages, and maps logical near‑term moves. Highlights include:

Eta Research Ltd. (Shanghai) — a bulk GaN producer using an in‑house HVPE process. Its self‑developed capability in free‑standing wafers and portfolio of doping variants positions it as a cost‑competitive supplier for laser diode, RF and power sectors seeking alternative substrate sources.

Sanan Optoelectronics / Sanan Semiconductor — notable for large-scale GaN‑on‑Si epi capabilities and foundry services. Their capacity expansions reflect a strategy to serve both commodity power device demand and higher‑value optical segments via scale and integrated service offerings.

Sumitomo Electric Industries — focused on GaN substrate innovation and larger diameter GaN‑on‑GaN wafers targeting high‑performance power applications. Recent work on polycrystalline diamond integrations signals a push into differentiated, performance‑driven product segments.

NGK Insulators — leveraging liquid‑phase crystal growth for ultra‑low dislocation density GaN wafers aimed at RF and optical customers demanding high crystallinity and reliability.

IQE plc — a leading epitaxial wafer supplier across SiC, Si, GaN and engineered substrates, now accelerating partnerships to co‑develop device platforms (e.g., power platforms for automotive and data center stacks).

Wolfspeed (formerly Cree) — a stronghold in GaN‑on‑SiC and device production for RF power, with deep market channels into telecom and defense segments.

Recent industry moves underscore the dynamic landscape: Infineon ramping toward scalable 300mm GaN samples, Sumitomo’s GaN‑HEMT on diamond substrate work, and IQE’s strategic collaborations with wafer fabs to deliver 650V platforms for automotive and data center customers. These developments crystallize two competing strategic models: integrated scale‑up by established materials/device leaders, and modular ecosystem plays where specialized wafer suppliers and foundries form value‑chain coalitions.

Our concentration analysis shows a market where the three largest firms capture a meaningful share but not a dominant monopoly position, and the five‑player concentration rises materially — a structure that creates both cooperation opportunities (e.g., shared supply initiatives) and competitive tension (competing non‑price differentiators such as yield, service, and IP). These dynamics shape realistic M&A, JV and procurement scenarios for 2026.

Raw material geopolitics and price shocks. Policy decisions affecting gallium exports, shifts in global production concentration, and unit cost changes can change supplier economics and trigger urgent re‑routing or long‑term supplier contracts.

Scaling execution risk. Delays or yield shortfalls in 300mm migration or in new substrate forms materially change competitive advantage and capital recovery profiles.

Demand adoption variability. End‑market adoption rates for GaN in power supplies, EVs, data center power architectures and RF infrastructure will determine the pace of commercial absorption and capex amortization.

Regulatory and trade developments. Export controls, tariff regimes, and national procurement policies will influence supply chain siting decisions and strategic inventory posture.

Prioritize investment staging: use our scenario outputs to phase CapEx commitments — pilot, pre‑commercial, and full‑scale — while tying payment and performance milestones to yield improvements and price curves.

Design procurement and supplier diversification playbooks: stress‑test suppliers against gallium and other upstream constraints and simulate outcomes under short‑term export restrictions and price shocks.

Craft targeted partnerships: match device roadmaps to wafer suppliers whose technology and capacity timing best align with product launch windows, and lock in JDA or foundry arrangements where appropriate.

Build an M&A shortlist: leverage our proprietary screening to identify targets that fill technical, capacity or market access gaps — and use our valuation heuristics to price in execution and integration risk.

This briefing is a curated preview of the full PW Consulting Gan Wafers Market Study. The complete report contains the granular segmented datasets, interactive models, supplier scorecards, technology adoption curves and the full set of scenario outputs that senior teams rely on to commit capital and resources. To preserve competitive confidentiality and to provide clients with actionable exclusivity, the detailed regional, type, and application segment tables and modelled revenue splits are available via our report portal.

For teams preparing 2026 strategic plans, this study is designed to convert macro momentum into executable actions: select partners, sequence investments, and protect margins against raw material and policy shocks. PW Consulting remains available to translate the report’s outputs into bespoke roadmaps, due diligence support, and board‑level decision packages.

For detailed analysis of this topic, please visit the official page:Gan Wafers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com