Experts Predict: Inverters and Converters Will Drive the Power Electronics Market

Other |

2026-04-27 06:23:47

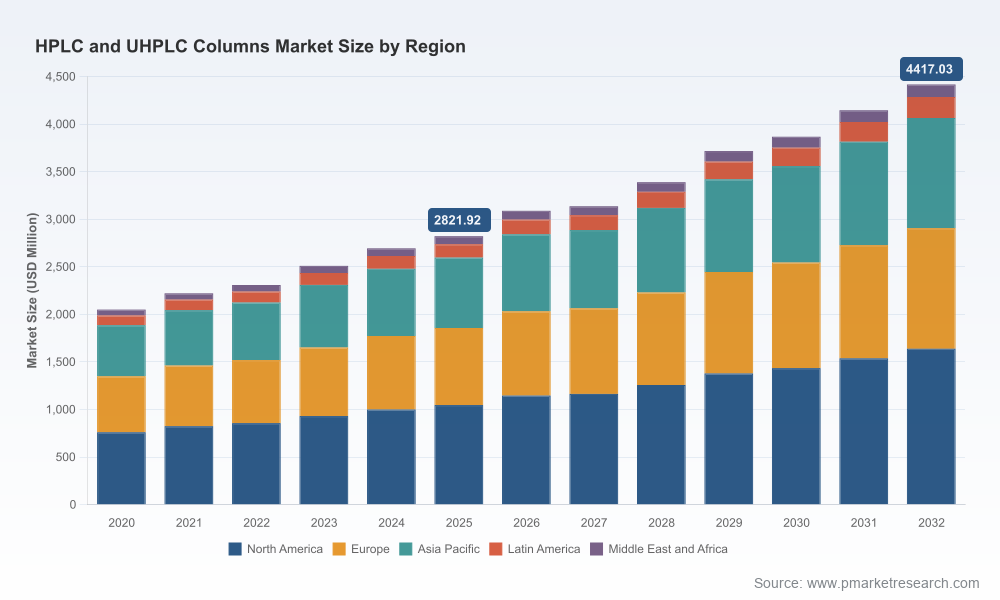

As companies prepare investment roadmaps and product strategies for 2026, the HPLC and UHPLC columns market presents a distinct blend of steady expansion and concentrated competitive dynamics. PW Consulting’s latest market study — with 2025 as the base year and a 2026–2032 forecast horizon — quantifies that momentum: a compound annual growth rate (CAGR) of 6.61% underpins a market that grew through the early 2020s and reached a multi‑billion USD level in 2025, with clear acceleration anticipated through the forecast window. For senior leaders in analytical labs, instrument manufacturers, reagent suppliers and private equity investors, these headline figures frame three strategic imperatives that will determine winners and laggards in 2026 and beyond.

Hplc And Uhplc Columns Market

Regulatory and technical thresholds are converging. Increasing regulatory expectations for sensitivity and resolution in pharmaceutical quality control are pushing laboratories toward advanced UHPLC columns with sub‑2 μm particles and hybrid chemistries. This trend is not transient: it reshapes capital equipment cycles, consumable sourcing strategies and method transfer priorities across QC and R&D functions.

Hplc And Uhplc Columns Market

Downstream bioprocess analytics and oligonucleotide therapeutics are driving demand for specialized stationary phases and high‑inertness hardware. Recent product introductions from major vendors specifically target these use cases, signaling supplier commitment to life‑science upgrades that will influence procurement decisions in 2026.

Hplc And Uhplc Columns Market

Raw material dynamics and supply chain resilience are rising on procurement scorecards. Analysts tracked a notable uptick in silica feedstock market dynamics in late 2025 — a reminder that substrate availability, price volatility and particle‑engineered differentiation can materially affect margin and lead‑time for column manufacturers.

PW Consulting’s model — rooted in historical performance from 2020–2025 and stress‑tested against macroeconomic scenarios and use‑case adoption curves — shows the market expanding from its 2025 baseline to materially higher levels by the end of the 2026–2032 forecast window. The 6.61% CAGR reflects a composite of recurring consumable demand, instrument retrofit cycles, method modernization in regulated labs, and growing uptake in environmental and food safety testing where analytical sensitivity is increasingly mandated.

For CFOs and heads of strategic planning, the implications are straightforward: predictable top‑line growth justifies targeted investments in manufacturing scale, differentiated chemistries and channel expansion, while also demanding tighter cost control on raw material exposures and logistics. The market’s moderate concentration — with the top three players commanding a meaningful share but not monopolizing the sector (CR3 ~42.5%, CR5 ~61.8%) — creates opportunity for mid‑market firms and focused innovators to capture specialty niches.

Integrated Scenario Modeling. We provide downside, baseline and upside scenarios that quantify the sensitivity of revenue pools to key variables: adoption of UHPLC in regulated QC, silica supply shocks, and evolving environmental method mandates.

Go‑to‑Market Playbooks. The report translates demand signals into practical commercial strategies — from channel mix optimization and service bundling to pricing strategies for premium chemistries and lifetime‑value management of high‑frequency consumables.

Technology Roadmaps. We map product feature priorities (inertness, pH range, particle morphology, column formats) to customer segments and validation pain points, enabling R&D prioritization that aligns with 2026 procurement cycles.

Supply Chain Risk Assessment. The study includes supplier matrices, lead‑time stress tests and mitigation tactics for raw material concentration — essential for operations and procurement teams building resilient sourcing strategies.

Competitive Positioning Tools. Benchmarked scorecards and capability heatmaps allow business leaders to identify white spaces for differentiation and potential M&A targets that accelerate scale or technology access.

The HPLC/UHPLC columns ecosystem is anchored by a mix of instrument incumbents, specialty chromatography firms and niche technical suppliers. In their own ways, leading companies are moving beyond simple column SKUs toward platform thinking: pairing stationary‑phase chemistry with instrumentation, software and lifecycle services that increase switching costs for end users.

Agilent Technologies (Santa Clara) continues to lean on broad product families and advanced chemistries aimed at small molecules, biotherapeutics and oligonucleotides. Its recent launches emphasize ultra‑inert surfaces tailored for sensitive bioanalytical workflows, underlining a go‑deep strategy in life‑science QC and R&D.

Waters Corporation (Milford) differentiates through integrated technologies — proprietary resin capabilities, hybrid surface chemistries and instrument‑column co‑development. Their MaxPeak and BioResolve introductions illustrate a focus on high‑throughput biopharma measurements and preparative upgrades.

Thermo Fisher Scientific leverages portfolio breadth to serve diverse end markets, while Shimadzu and Merck KGaA (MilliporeSigma) maintain strong positions through system compatibility, superficially porous particle innovations and applications in peptide and protein analysis.

Danaher’s Phenomenex, Tosoh, Biotage and a cadre of specialist suppliers (e.g., Restek, KNAUER, YMC) play to niche strengths — core‑shell technologies, chiral separations, size‑exclusion expertise and robustness for environmental and food testing. These players are the primary source of tactical innovation and application‑specific differentiation.

Regional and specialized vendors remain significant in customer segments that prioritize cost, local support or unique stationary phases; their agility is an asset where method equivalence and fast validation cycles are prioritized.

Product launches in 2025 targeted life‑science workflows (ultra‑inert columns and affinity columns optimized for protein titer measurements), signaling supplier prioritization of biopharma QC and method robustness.

Process‑scale column introductions reflect increased focus on downstream bioprocessing analytics and scale‑up interoperability between analytical and preparative chromatography.

Smaller entrants and component specialists continue to introduce high pH‑stable phases and hybrid particle architectures, increasing competitive pressure on incumbent commodity offerings.

Decision‑makers must balance three operational dynamics when planning for 2026:

Cost versus performance trade‑offs. Buyers in regulated industries will pay premiums for columns that reduce method variability and validation burden, while high‑volume, cost‑sensitive laboratories will prioritize ruggedness and throughput.

Validation and method transfer friction. Vendors that support method equivalency, provide robust validation packages and offer column‑instrument pairings will lower barriers to upgrade and lock in recurring consumable demand.

Supply chain and raw material exposure. Changes in silica feedstock markets and production capacity matter. PW Consulting’s analysis highlights material supply concentration and its potential to propagate lead‑time and price volatility — a critical factor for manufacturing and procurement leaders.

For manufacturers: invest selectively in differentiated chemistries and in‑house capabilities that raise switching costs (e.g., proprietary resins, validated method kits). Pair R&D roadmaps with channel enablement and lab services to accelerate adoption.

For distributors and OEMs: prioritize portfolio curation that balances high‑margin specialty products with rugged mainstream offerings. Offer bundled validation and training services to capture the validation‑heavy life‑science customer base.

For laboratory operators: assess total cost of ownership beyond list price — consider column lifespan, method transfer time and vendor support. Where regulatory pressure is increasing, moving to advanced UHPLC chemistries may reduce downstream risk and rework.

For investors: the market’s mid‑range concentration combined with steady CAGR creates diversified opportunities — from bolt‑on acquisitions that add niche chemistries to platform plays that consolidate regional specialists with strong service footprints.

In line with our “trailer” approach to this public release, PW Consulting intentionally showcases market directionality, strategic implications and supplier dynamics while withholding the full tabular segmentation outputs and granular regional or application‑level dollar breakdowns that underpin our forecast. The deep segmentation matrices, scenario model inputs, price sensitivity analyses and supplier scorecards are included in the full report and interactive dashboard — critical tools for operationalizing a 2026 strategy.

Executives and strategy teams should treat these findings as the foundation for three immediate actions:

Initiate a portfolio stress test against our scenario models to prioritize capex and R&D spend.

Engage procurement to assess supply‑risk mitigation (contracting, dual‑sourcing, vertical integration where feasible).

Schedule vendor and service partner audits focused on validation support and end‑user training capabilities to accelerate method adoption.

For organizations that require the full economic model, granular segmentation, supplier scorecards and download‑ready validation templates, PW Consulting’s comprehensive Hplc And Uhplc Columns Market report provides the complete dataset and practical playbooks to convert the 2026 opportunity into measurable outcomes. Access to the full resource includes interactive forecasting tools, supplier comparators and risk‑adjusted scenario outputs designed for board‑level decision making.

For detailed analysis of this topic, please visit the official page:Hplc And Uhplc Columns Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com