Organic Coconut Water Market Consumer Preferences and Purchase Behavior Analysis 2026–2034

Home |

2026-06-25 10:10:25

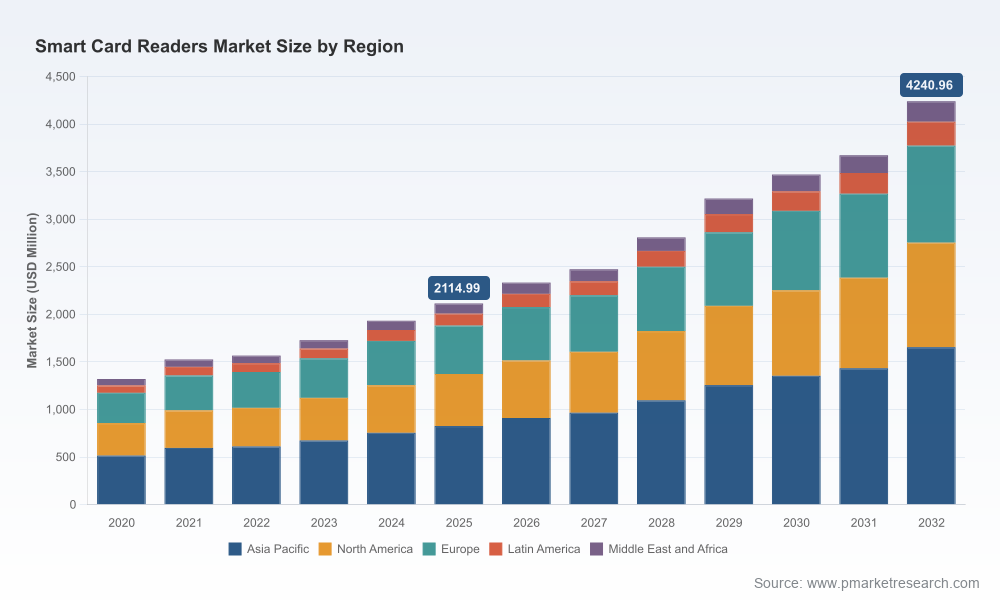

PW Consulting’s new Smart Card Readers Market report (base year 2025, historical 2020–2025, forecast 2026–2032) is designed as an executive-grade playbook for procurement, security architecture, and product strategy teams preparing for a decisive wave of deployments through 2026 and beyond. The market is expanding rapidly — growing from roughly USD 1.32 billion in 2020 to about USD 2.11 billion in 2025, and projected to continue on a double-digit trajectory (CAGR 10.45% for the 2026–2032 forecast window) to reach an expected market scale north of USD 4.24 billion by 2032. Market concentration is moderate: the top three vendors account for about 38% of revenue, and the top five eclipse roughly 52% — a structure that favors tiered vendor strategies and targeted partnerships.

Smart Card Readers Market

Timing matters. 2026 is the inflection year for several convergent forces: contactless use-cases accelerated by public health and convenience, widespread implementation of strong authentication standards (PKI, FIDO), and national eID programs moving from pilot to scale. Together these create both procurement urgency and opportunity for cost- and risk-optimized rollouts.

Smart Card Readers Market

Regulatory and standards pressure is rising. Compliance requirements such as FIPS 201 for government physical access, country-specific certifications (e.g., BIS for India), and extended NFC interoperability standards are changing vendor selection criteria and deployment checklists.

Smart Card Readers Market

Technology differentiation is now productized. Read-range improvements, NFC certification updates, embedded cryptographic modules, and multi-protocol readers are the new features that determine project success beyond baseline EMV or ISO compliance.

Market momentum: From 2020 to 2025 the sector recorded strong cumulative growth; the market enters 2026 with momentum and forecasted compound growth of 10.45% through 2032.

Scale opportunities: The market size in 2025 provides a robust base for enterprise and public-sector procurement programs; 2026 projections indicate sustained buyer demand for contactless, FIDO-ready, and government-compliant devices.

Vendor concentration: With ~38% CR3 and ~52% CR5, buyers can combine established global suppliers for scale with specialist vendors for niche requirements (payments, healthcare eID, IoT integration).

Executive brief and decision matrix: A one-page procurement decision matrix that aligns use-case priorities (authentication strength, interoperability, lifecycle cost, regulatory compliance) to procurement levers.

Market sizing and clear methodology: Transparent top-down and bottom-up approaches, assumptions and sensitivities used to arrive at the 2025 base and 2026–2032 forecast, plus downloadable model worksheets.

Technology & standards assessment: Comparative evaluation of contact vs contactless architectures, ISO/IEC 7816 and 14443 interoperability implications, EMV and NFC considerations, and FIDO/PKI adoption pathways.

Regulatory and certification matrix: Practical guidance on FIPS 201, country-level certifications (e.g., BIS), procurement language to enforce compliance, and risk controls for cross-border deployments.

Vendor benchmarking and procurement toolkit: Vendor scorecards, RFP templates, evaluation checklists, a short-listing methodology and sample negotiation playbooks to secure service-level and security commitments.

Deployment and integration playbooks: TCO and TTR (time-to-rollout) models, migration checklists (including cabling and interface upgrades), pilot KPI trackers, and recommended staging for scale rollouts.

Strategic scenarios: Three investment scenarios (consolidated, diversified, specialist-heavy) showing projected cost, time-to-value, and regulatory risk profiles to fit executive risk appetites.

The market is populated by a mix of global platform providers, specialized OEMs, and regional systems integrators. Our proprietary vendor framework assesses each supplier on four dimensions: security & cryptography, standards & certification footprint, integration ecosystem, and commercial flexibility (pricing, support, partner channels).

Advanced Card Systems Ltd. (ACS) — Hong Kong: Strong in multi-form-factor readers (USB, NFC, mobile) and rapid product updates for e-government and identity use-cases. Recent showcases at ID4Africa and certifications for government digital ID programs underscore its eID/government focus.

Identiv Inc. — United States: Noted for PIV/FIPS 201-capable uTrust series and physical/logical access integration. Well-suited for U.S. government and enterprise security programs where certified lists and FIPS compliance matter.

HID Global — United States: Enterprise-grade OMNIKEY portfolio with deep integration into access control and PKI ecosystems; a preferred option for organizations standardizing on a single vendor for both physical access hardware and identity lifecycle services.

Thales & IDEMIA — France: Positioned as high-security cryptography specialists with end-to-end identity and authentication platforms; attractive to governments and regulated verticals requiring stringent cryptographic assurance.

MagTek, Feitian, SpringCard, ID TECH, Castles, PAX and regional OEMs: These vendors cover payments, POS, and terminal-focused solutions. Their strengths are in transaction-level security and regional distribution, making them suitable for retail and transport projects where payment compliance and merchant networks are essential.

ASSA ABLOY and specialty access-product vendors: Best for physical access integrations, often bundled with door hardware and access management systems to simplify procurement for facilities teams.

Recent industry developments inform the competitive dynamics: ACS’s product demonstrations and government certifications in 2026 validate accelerating demand for certified eID readers. Meanwhile, standards evolution — notably the NFC Forum’s Certification Release enabling longer contactless read ranges — is shifting feature differentiation toward interoperability and user experience rather than raw hardware presence.

Procurement architecture: Combine a core platform supplier for scale and a set of specialists for high-assurance, payment, or localized regulatory needs. Use CR3/CR5 concentration insights to balance bargaining power and delivery risk.

Compliance-first specifications: Embed regulatory acceptance (FIPS 201, local certification) as pass/fail criteria in RFPs. Include firmware attestation, secure update pathways, and supply-chain provenance clauses.

Technical integration: Plan for infrastructure upgrades — many migrations require networked readers (TCP/IP) or RS-485 pathways and upgraded cabling (Category-5 or higher) to support two-way data flows and edge management.

Security lifecycle: Prioritize devices that support hardware-backed keys (PKI), FIDO authentication, and remote key management; require over-the-air firmware signing and rollback protections as contractual SLAs.

Operational pilots: Short pilots should validate read-range behavior, multi-protocol interoperability, usability across demographics, and backend PKI/FIDO integration rather than only device benchmarks.

Inventory & use-case mapping: Map current readers and endpoints to business-critical applications, compliance requirements, and end-user experience priorities.

Compliance gap analysis: Crosswalk existing inventory against FIPS 201 and local certifications; flag replacements and firmware remediation targets.

Vendor shortlisting and procurement playbook: Use our RFP templates to run two competitive pilots — one focused on government/compliance and one focused on high-volume contactless UX — and score vendors against the four-dimensional framework.

TCO and migration modeling: Run the report’s downloadable TCO model to evaluate capex/opex trade-offs, support windows, and software/firmware lifecycle costs.

Negotiate long-term support & update commitments: Secure firmware signing, vulnerability disclosure timelines, and spare-part assurances as part of contract negotiations.

This briefing is a “trailer” of the full PW Consulting Smart Card Readers Market report. The complete report contains the granular regional and end-use segmentation, vendor scorecards with feature-level matrices, downloadable Excel models, scenario sensitivity analyses, and a procurement-ready RFP kit. That level of detail is intentionally reserved for the full deliverable to provide the exact inputs your procurement, security, and engineering teams need to execute in 2026.

If your 2026 strategy depends on a reliable, standards-aligned, and cost-optimized rollout of smart card readers — whether for identity, payments, access control, or healthcare — this report converts market dynamics into an operational roadmap. PW Consulting’s analysis combines market-scale forecasts, regulatory intelligence, vendor differentiation, and practical playbooks so executive teams can make informed, defensible decisions before committing resources this fiscal year.

For detailed analysis of this topic, please visit the official page:Smart Card Readers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com