Military Tactics Simulator Market: Strategic Intelligence for 2026 Decision-Making

As PW Consulting’s lead industry analyst, I present an executive briefing drawn from our forthcoming Military Tactics Simulator Market report — a strategic “trailer” that highlights the intelligence firms, procurement authorities, and technology investors must have on their radar for 2026. The global market for military tactics simulators has reached a strategic inflection point: in 2025 it stood at approximately USD 16.15 billion, and under our baseline projection it is set to expand to roughly USD 26.65 billion by 2032, representing a compounded annual growth rate of 7.42%. These macro dynamics underpin a set of operational, procurement, and technology choices that will determine competitive positioning through the end of the decade.

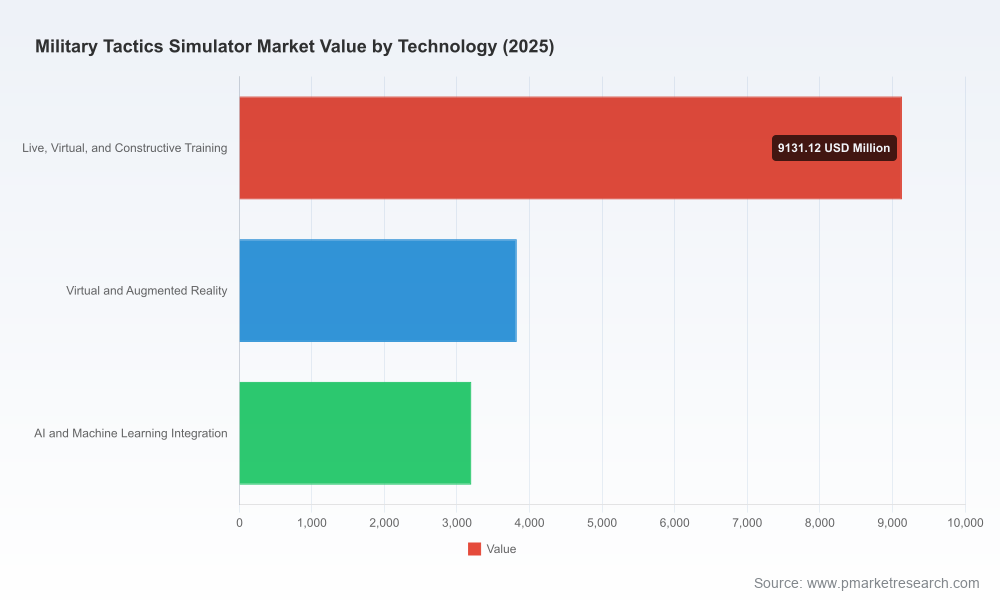

Military Tactics Simulator Market

Why 2026 Is a Pivotal Year

- Budget cycles across major defense customers are aligning to fund multi-year modernization programs that emphasize Live-Virtual-Constructive (LVC) integrations, VR/AR-enabled training, and AI-augmented tactical decision aids.

- Standards and regulatory updates — from coalition interoperability frameworks to national VV&A policy — are moving from concept to enforcement, compressing the window in which systems must prove compliance.

- Supply-side constraints around advanced compute, high-fidelity terrain modeling, and haptics are creating short-term bottlenecks that will influence contract structure, delivery timelines, and pricing dynamics.

For any organization preparing procurement, R&D, or M&A strategies in 2026, the choice is between locking in legacy, monolithic solutions or adopting modular, standards-aligned architectures that lower integration risk while increasing upgrade velocity. Our report is designed to make that trade-off explicit and actionable.

Military Tactics Simulator Market

What the Report Delivers (Operationally Focused)

PW Consulting’s report is built around decision-ready deliverables rather than academic description. Key operational components include:

Military Tactics Simulator Market

- Market-sizing and growth scenarios calibrated to procurement cycles — with downside, baseline, and accelerated-adoption cases to stress-test investment assumptions.

- Vendor benchmarking and capability maps that score vendors across integration readiness, LVC maturity, VV&A support, sustainment cost, and cyber-hardening.

- Procurement playbooks and RFP templates tailored to modular simulation architectures, including clauses to manage compute supply risk and intellectual property for software components.

- Technical deep-dives into VR/AR, AI/ML integration, and high-fidelity constructive simulations — each with hands-on checklists for testbeds, minimum viable fidelity, and performance measurement.

- Interoperability and standards playbook aligned to NATO and DoD frameworks (including HLA/C2SIM and VV&A guidance) that converts compliance into procurement requirements and acceptance criteria.

- Pilot and PoC blueprints with evaluation metrics for fidelity, training throughput, mission-rehearsal effectiveness, and lifecycle cost modeling.

- M&A and partnership playbooks focusing on bolt-on software, terrain data capabilities, and access to classified benchmarking environments.

The report emphasizes actionable material: templates, measurable KPIs, and scenario-based decision trees that enable program managers and C-suite leaders to move from strategy to execution quickly.

Competitive Landscape: Strategic Implications

The market exhibits a moderate level of concentration (CR3 around 42% and CR5 approximately 58%), indicating a field where leading primes hold influence but credible specialist and software-only firms continue to capture niche opportunities. Below are strategic assessments of core industry players you should monitor closely.

- CAE Inc. — CAE’s strengths are in comprehensive LVC ecosystems and integrated training solutions. Expect continued emphasis on end-to-end program offers that bundle simulation hardware, scenario libraries, and sustainment contracts. For buyers, CAE typically reduces program risk but can increase vendor lock-in unless modular exit clauses are negotiated.

- Rheinmetall AG — With a strong foothold in land-systems simulation and XR driver training, Rheinmetall is positioning for combined-arms modernization efforts. Their approach favors platform-specific fidelity and vehicle-in-the-loop capabilities, making them a logical partner for force-modernization projects focused on armored and mechanized units.

- Thales Group — Thales brings integrated command-and-control simulation strength. Their value proposition is in coupling tactical scenario simulation with C2 interoperability — attractive to customers pursuing whole-of-force training and doctrine validation.

- Lockheed Martin — Lockheed’s immersive suites and mission rehearsal tools are optimized for integration with broader systems of record. Their advantage is program-scale delivery and classified-environment credentials, but competition exists from more agile software-centric suppliers.

- BAE Systems — BAE’s tactical engagement and combined-arms simulation capabilities, including solutions designed for networked exercises, make them a primary contender for coalition training procurements.

- L3Harris Technologies — L3Harris offers maritime and ground system simulators with a focus on crew synchronization. Expect continued competition on turnkey training ranges and systems that emphasize human-machine teaming.

- Saab AB — Saab’s AR-focused simulators and emphasis on joint operations position them well for nations upgrading infantry and squad-level training with augmented systems that bridge live and virtual.

- Bohemia Interactive Simulations — As a software-native provider of VBS4, Bohemia remains a go-to for high-fidelity tactical scenario software. Their modular, extensible architecture is attractive to customers seeking rapid updates and lower integration costs.

- FAAC Incorporated — FAAC’s niche in vehicle crew and route-clearance simulators provides opportunities in specialized treaties and countermine mission sets where fidelity in vehicle dynamics and sensor simulation matter.

- HAVELSAN Inc. — HAVELSAN’s capabilities in tactical warfare simulation and command training are notable in markets pursuing localized sovereign development and regional interoperability.

- Cubic Corporation — Cubic’s LVC and tactical engagement systems are well-suited to force-on-force training and combined-arms exercises. Their business model favors scalable solutions across training ranges and institutional training centers.

Strategic takeaway: primes and software incumbents are converging. Buyers should evaluate a blend of prime-led systems for scale and software-specialists for agility. For vendors, differentiation will come from standards compliance, AI-enabled instructor tools, and data-driven training outcomes.

Regulatory & Standards Dynamics That Will Shape Contracts

- NATO interoperability frameworks and standards that specify High Level Architecture and simulation exchange formats are moving from recommendation to contractual requirement. Programs that do not demonstrate compliance risk non-qualification in multinational exercises.

- Updated DoD VV&A guidance tightens expectations around model verification and lifecycle accreditation; suppliers must show end-to-end traceability and documented validation regimes.

- C2SIM standards are increasingly referenced in procurement language to ensure simulations can exchange operational intent and orders with command systems without bespoke middleware.

These regulatory movements create two practical effects for 2026: (1) increased upfront engineering and test effort (and cost) to demonstrate compliance; (2) a premium for vendors with repeatable VV&A processes and demonstrable interoperability credentials.

Technology Enablers and Supply Constraints

Adoption of VR/AR, LVC, and AI/ML is accelerating, but high-fidelity simulation demands advanced computational hardware and richly detailed 3D terrain models. Our market analysis highlights potential supply bottlenecks in specialized GPUs, real-time terrain generation pipelines, and haptic subsystems. Organizations should expect longer lead times for turnkey systems unless procurement strategies account for component-level sourcing or cloud-/edge-compute alternatives.

Recommendations for 2026 Decision-Makers

- Make interoperability and VV&A non-negotiable procurement criteria. Require demonstrable compliance with relevant coalition standards as part of acceptance testing.

- Favor modular, service-oriented architectures over monolithic systems. Include migration and data-portability clauses to reduce vendor lock-in risk.

- Design pilots to stress-test supply-chain assumptions — particularly compute, terrain content, and haptics — before committing to full deployments.

- Embed performance-based logistics and sustainment metrics into contracts to shift risk to vendors while preserving upgrade pathways.

- Prioritize partnerships with software-native providers for rapid scenario updates and with primes for platform-level integration where scale and security are required.

- Measure training ROI using mission-aligned KPIs: mission-rehearsal fidelity, trainee throughput, time-to-validity (VV&A cycle time), and total cost of ownership over a 7–10 year horizon.

How PW Consulting Can Support Your 2026 Agenda

Our full report supplies the data, templates, and scenario tools needed to operationalize the recommendations above. It contains supplier scorecards, procurement clause banks, a VV&A playbook, and PoC evaluation templates designed to be plug-and-play with defense acquisition processes. This briefing intentionally omits deep segmentation tables and transactional-level pricing details to direct you to the primary report where the full datasets, region- and platform-level breakdowns, and downloadable tools are available.

Contact PW Consulting to schedule a briefing or request an excerpted dataset tailored to your program office, investor diligence team, or defense R&D portfolio. For leaders facing 2026 procurement windows, the choices made now — around standards, modularity, and supplier mixes — will determine operational readiness and budget effectiveness for years to come.

For detailed analysis of this topic, please visit the official page:Military Tactics Simulator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com