How Are AI-Driven Threat Detection Technologies Transforming the Proactive Security Monitoring Market?

Networking |

2026-03-12 06:08:51

PW Consulting is pleased to present an executive preview of our flagship Soldier Combat System Market report, designed to inform and accelerate strategic decisions in 2026 for prime contractors, mid‑tier suppliers, investors, and defence procurement authorities. The report consolidates five years of historical observation (2020–2025) with a forward view across the 2026–2032 forecast window, projecting a steady compound annual growth rate (CAGR) of 6.45%. In aggregate terms, the market expanded from approximately USD 10,650 Million in 2020 to USD 14,522.92 Million in 2025, and our base modelling anticipates continued growth through 2032, with the market reaching an estimated USD 22,495.06 Million by the end of the forecast horizon.

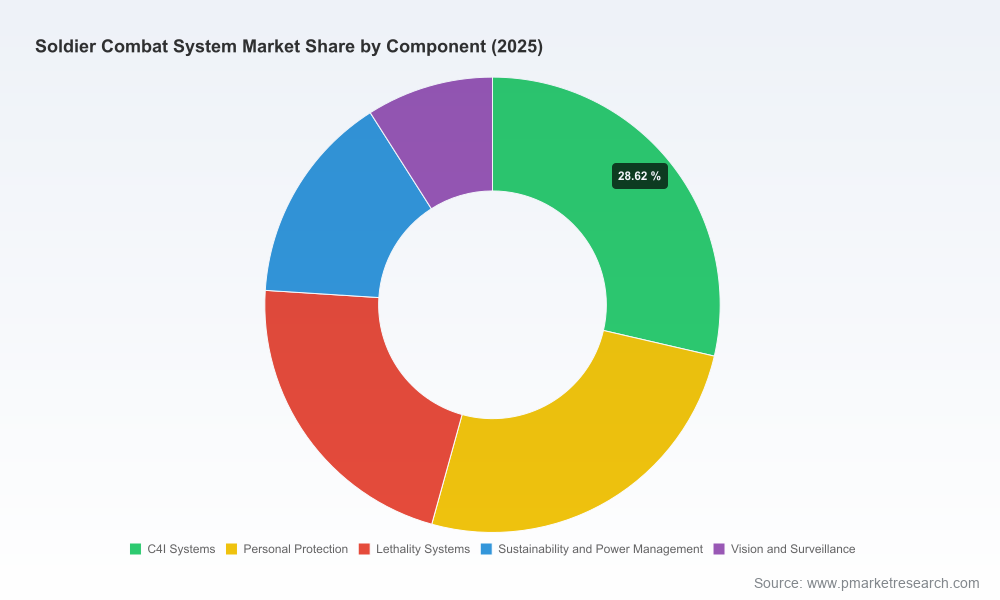

Soldier Combat System Market

Timing and scale: With procurement cycles lengthening and capability refresh requirements accelerating, the 2026 calendar is a pivotal inflection point for suppliers to secure mid‑term programme positions and for customers to lock in interoperable architectures that will deliver value over multiple upgrade waves.

Soldier Combat System Market

Risk‑constrained investment: The report provides a practical framework to evaluate technology bets (e.g., power and data management, multispectral sensors, C4I middleware) against regulatory and export risk, enabling boardroom‑level decisions that balance growth potential and compliance exposure.

Soldier Combat System Market

Competitive posture: Our analysis identifies where scale and systems‑integration capabilities matter most, and where specialist suppliers can win by supplying modular subsystems — information that is directly actionable for M&A, JV, and partnership strategies in 2026.

Executive dashboards that translate macro forecasts into decision‑ready artefacts: procurement timelines, program prioritisation matrices, and a go‑to‑market playbook keyed to capability clusters.

Vendor benchmarking that goes beyond feature lists — scoring suppliers on systems integration experience, open‑architecture delivery, sustainment footprint, and export‑compliance posture.

Supply‑chain and industrial base mapping, highlighting single‑source risks, critical component concentration, and lead‑time sensitivities for power systems, optronics, and advanced textiles.

Operational case studies and field trial templates that help programme managers convert lab prototypes into deployable kits while controlling soldier load and lifecycle costs.

Actionable modelling tools: scenario‑driven revenue build templates, procurement spend corridors, and a decision tree for buy vs. build vs. partner choices calibrated to 2026 budget cycles.

The market’s mid‑single‑digit CAGR masks significant structural shifts. Demand remains anchored in integrated C4I and situational awareness capabilities, while survivability, lethality augmentation, and sustainable power distribution are the primary engineering focal points for the next programme wave. Modularity and open‑architecture principles are no longer optional: programmes that embed standards engineering for power/data distribution and vehicle interoperability gain both procurement and sustainment advantages.

Industry concentration metrics indicate a market where a handful of systems integrators retain material share but where specialist suppliers exert disproportionate influence over capability roadmaps. Our concentration analysis (CR3 ~38.5%; CR5 ~54.2%) points to a moderately consolidated prime layer with an active and contestable second tier — fertile ground for targeted partnerships and bolt‑on acquisitions in 2026.

Primes with systems‑integration heritage: Companies such as Rheinmetall, BAE Systems, Thales, Safran, General Dynamics, and L3Harris remain central because they can deliver end‑to‑end integration across C4I, communications, and platform connectivity. Rheinmetall’s recent framework award for a major infantry digitization programme — a multi‑year contract announced in early 2025 — underscores the strategic value of platform incumbency and proven open‑architecture implementations.

Specialists and sensor houses: Firms like Elbit Systems and Saab continue to push differentiated capability sets (multispectral sensors, camouflage systems and lightweight optronics) that influence prime design choices. Elbit’s contract win in 2026 to develop next‑generation head‑borne mission command hardware highlights supplier relevance at the sensor/host interface.

Protection and apparel innovators: NP Aerospace and others are converting protection expertise into integrated solutions (armour, apparel, e‑textiles) that address soldier burden and modularity — teaming arrangements announced in 2025 show this trend is accelerating.

New‑economy entrants and suppliers: Expect a steady inflow of firms focused on power management, energy harvesting, AI‑enabled sensor fusing, and life‑sign monitoring — areas that prime integrators will either develop internally or source through partnerships.

Export control regimes (notably ITAR and national munitions/dual‑use frameworks) materially affect programme structuring, supplier selection, and go‑to‑market timelines. Early licensing strategies, export control engineering, and technical data compartmentalisation should be treated as programme design constraints rather than downstream compliance tasks. Concurrently, NATO and allied interoperability expectations are driving adoption of open architectures for C4I and power/data interfaces — programmes that achieve both regulatory robustness and standards compliance will shorten delivery timelines and expand export optionality.

Our field interviews and lab‑to‑field assessments consistently flag a handful of recurring integration challenges that derail schedules: power and thermal management for dismounted suites; reliable, low‑latency data distribution for sensor fusion; ruggedised human‑machine interfaces that preserve soldier ergonomics; and sustainment logistics for complex sensor suites. These are not hypothetical engineering risks—they are the most common causes of cost growth and late fielding. Solutions that demonstrably reduce soldier burden while maintaining modular upgrade paths command premium procurement attention in 2026.

Prioritise modular open‑architecture bets: Allocate R&D and bid resources to interfaces and middleware that enable plug‑and‑play subsystems; this lowers integration cost and expands addressable markets.

De‑risk export early: Embed export control and technical data strategies into programme planning. Regulatory lead times can exceed hardware lead times; plan licensing workstreams in parallel with development.

Invest in power and sustainment: Treat battery systems, smart textiles and hub architectures as strategic enablers. Small improvements in power density and management deliver outsized operational value.

Make partnerships conditional: Use proof‑point milestones and limited‑run field trials to qualify partners, preserving optionality for future capability waves.

Target selective consolidation: For investors and corporates, the CR3/CR5 profile indicates room for value‑accretive M&A among specialists with scalable IP in sensors, lightweight protection, or power subsystems.

Operationalise sustainment thinking: Build spare‑parts and training models into initial contract pricing to avoid downstream cost escalation and fleet dilution.

Large framework awards and head‑borne system contracts announced in late 2024–2026 have realigned supplier prioritisation and cleared pathways for integration work in allied programmes. Notable examples include a multi‑year framework linked to a major European infantry digitisation effort and a 2026 US Army award focused on next‑generation head‑borne mission command.

Teaming agreements between protection specialists and apparel integrators illustrate an accelerating trend: delivering integrated kits at scale (including several thousand unit commitments in selected programmes) is now a commercially viable strategy for tier‑two suppliers.

The full report provides the granular instruments that procurement teams and corporate strategists need: detailed segmentation by component and platform, regional programme timing, vendor scorecards, supply‑chain heatmaps, total‑cost‑of‑ownership models, and scenario‑level demand curves. It also includes executable playbooks for procurement engagement, partner selection, and capability road‑maps tailored to 2026 budget cycles. In keeping with our “preview” approach, we have highlighted strategic signposts here while reserving the granular segment‑level tables and unit economics for the full report.

For organisations preparing 2026 bids, investment committees evaluating defence tech targets, or programme offices planning capability modernisation, the PW Consulting Soldier Combat System Market report is designed to shorten the path from insight to action. Our research team remains available for briefings, bespoke scenario modelling, and tailored supplier assessments to support critical decisions in 2026.

To access the full report and supporting data tools, visit the PW Consulting report page or contact our research desk for a briefing and licensing options.

For detailed analysis of this topic, please visit the official page:Soldier Combat System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com